A major slowdown in global growth is expected to be caused by US President Trump’s impending “tariff wall”. The recession will start with a dollar liquidity crisis in China and end with a crash in the US, as funding pressures circulate through the global banking system.

Because China runs a large trade surplus with the US, Chinese banks have accumulated large amounts of Eurodollars, with trade being the main source of dollar funding.

The tariff wall appears to be targeting China, restricting the flow of Eurodollar deposits into the mainland and exacerbating dollar funding pressures abroad. The payments chain is essentially the supply chain in reverse.

Since the start of the trade war before the pandemic, China has managed to circumvent US tariffs through Mexico, ASEAN and other countries (entrepot trade), continuing to channel products to American consumers.

Imposing a blanket tariff “fortress” on all US imports is an attempt to make this tactic impossible. China, of course, is aware of this geopolitical vulnerability and has long been preparing for such an eventuality, developing multiple levers of pressure beyond retaliation and new trade routes.

Chinese banks can transfer Eurodollar deposits to their New York branches — keeping them within the US banking system — or place them in nostro accounts within major US banks. This appears to have been the prevailing practice until 2023.

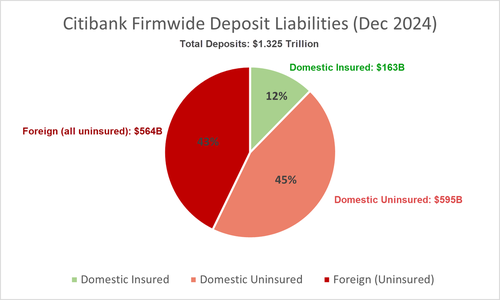

Since then, however, Chinese banks have been placing their deposits in nostro accounts in Hong Kong, i.e. outside the Fed system. Citibank has reported a huge amount of uninsured foreign deposits, much of which appears to come from Chinese claims. Notably, 79% of Citi’s domestic deposits are uninsured, which could trigger a solvency crisis if Chinese banks were forced to draw dollars immediately.

There are also serious risks in the event of a dollar shortage. If lending rates rise too high, Chinese banks and non-banks will be forced to liquidate dollar assets—stocks, government bonds, and credit—at fire prices. This will not only hurt the solvency of Chinese banks but also of American banks, while disrupting the stability of the global financial system.

The US sees an opportunity to inflict “asymmetric pain” on China, forcing its banks to adapt even more to the dollar system. However, it may overestimate its bargaining power. This sets the stage for another battle between the two Great Powers — and inevitably, there will be “blood.”

Recession? Crisis? Or just “detox”?

The word “recession” has become a key narrative. Tariffs are more likely to slow the economy than fuel inflation, creating recession risks that the market has not yet fully priced in. If a universal tariff wall had been imposed in 2021, it would likely have caused much greater inflationary pressure, because disposable and real incomes were higher, making consumers more willing to pay higher prices.

At this point in the business cycle, however, a tariff-induced price increase would likely force consumers to cut back on purchases and businesses to cut back on investment. Let’s leave the tariff debate aside altogether: fiscal expansion and immigration were two strong growth drivers under the Biden administration.

As these factors peak and stabilize, expectations for U.S. growth will be revised downward.

The slowdown in growth should come as no surprise. Upcoming labor market and GDP data will likely be weaker than in previous years, reflecting a “detoxification period.” That means lower stock prices and increased volatility. But does it also mean an “official” recession? Maybe.

The scale of undocumented immigration into the US can be controlled

When most people talk about a recession, they have a common denominator in mind: a stock market crash, which wipes out trillions of dollars with every 2% drop in the S&P 500. But a recession is not limited to that.

A true economic shock is characterized by more than one factor.

1. In a recession, there is no way to improve the deficit or make the fiscal path more sustainable. In modern America, even a rudimentary fiscal balance cannot be achieved. If returns on assets are not positive (stocks are not rising) or if businesses are not making profits (real GDP stagnates or declines), government tax revenues will fall, widening the budget deficit.

In a highly financialized economy, tax receipts correlate with asset prices. So most austerity attempts that hurt asset prices can blow out the deficit.

US Recessions Are Global

A characteristic of US recessions is that they have a global impact.

2. In the current monetary regime, especially in the post-GFC environment of abundant bank reserves, dollars are more readily available domestically than abroad. However, the needs of foreign banks and nonbanks for dollars are just as significant.

This means that financial crises—whether a small bank failure or a global financial crisis—tend to start abroad, where dollars may be scarce but US-denominated debt obligations exceed $13 trillion.

The crisis then returns to the US as funding pressures spread throughout the banking system.

Credit events and bank failures signal recessions

There are no recessions or economic slowdowns—even those that are covered up and not officially recognized—without some systemic credit event, that is, the failure of a lender.

This could be either the failure of a commercial bank that lends to the public or the failure of a hedge fund that “lends” to the U.S. government through arbitrage transactions in government bonds (basis trades).

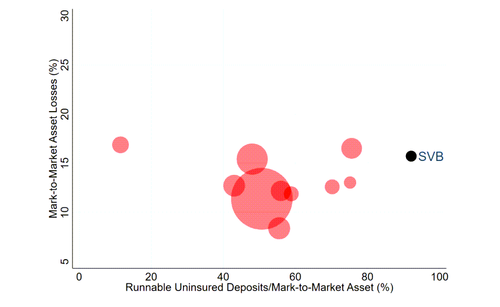

The failures of Silicon Valley Bank and Credit Suisse in March 2023 were characteristic features of a recession, as were the two consecutive quarters of negative real GDP and the bear market that preceded them.

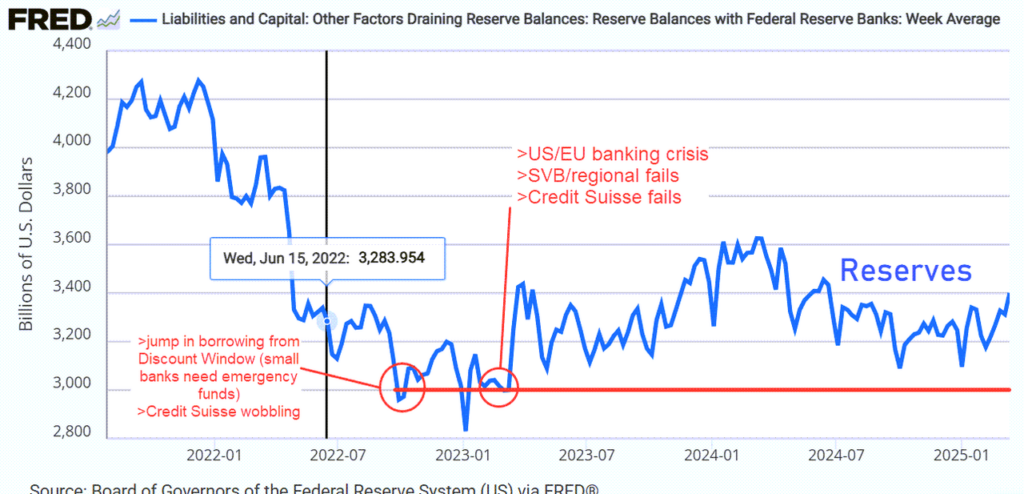

The Fed has been pumping reserves (liquidity used only by banks to settle payments between themselves) through quantitative easing (QE) programs for the two years after March 2022. However, even reserves are counted as leverage on bank balance sheets, and banks have limits on how much they can hold.

What is not counted as leverage are overnight loans to the Fed through the reverse repo facility, so that’s where the excess reserves were placed.

Reserves are the core of banks’ liquidity — they are used in their day-to-day operations and by dealing desks to execute transactions, such as buying government bonds.

Reserves have remained stable within a certain range since the start of quantitative easing (balance sheet taper) in June 2022. There is a “red line” below which they are considered insufficient, known as the Lowest Comfortable Level of Reserves (LCLoR).

It is not clear exactly where this line lies, but based on the pressures of 2022-2023, a good estimate is around $3 trillion or slightly above. While liquidity levels have been approaching this line, they have not breached it since March 2023.

If liquidity shortages lead to bank failures, and bank failures signal recessions, then liquidity shortages are a structural feature of a recession.

“Liquid,” “reserves,” “dollars” — these are all, in essence, the same thing, as are the terms “shortage,” “scarcity,” and “tight liquidity.” It’s hard to have a recession when lenders have a surplus of dollars. But that “surplus” seems to be peaking — especially outside the United States.

How do foreign banks obtain liquidity?

A recent and typical example of a crash due to a global dollar shortage was the Covid crisis. The shock of lockdowns in the first quarter of 2020 caused massive defaults, forcing more and more businesses to become “deficit agents” as they relied on borrowing to cover their cash flows.

As the crisis unfolded, banking systems around the world also became “deficit agents” — foreign banks suddenly needed immediate liquidity to continue lending to their businesses. Local central banks can manage defaults in their domestic currency.

The Bank of Japan can print reserves in yen, the People’s Bank of China can print reserves in yuan, and so on. However, foreign banks’ need for dollar funding is not as easily managed. The main problem during the Covid crisis was not local currency payment defaults, but a shortage of dollars — as everyone seemed to need dollar funding, but only the Fed could print dollar reserves and provide liquidity when other sources dried up.

Dollar funding is always the forgotten child of crises, but the Fed, the world’s de facto central bank, takes time to add liquidity. In “allied” countries and under normal circumstances, foreign banks have no problem obtaining dollar liquidity.

Many hold US Treasury bonds and can borrow dollars through the repo market. But if they don’t have government bonds or don’t have room on their balance sheets for repos, they can secure dollars through foreign exchange swaps (FX swaps) with a G-SIB (a globally systemically important bank, such as a large U.S. bank).

If the price is right, Citi, for example, will lend its dollar reserves to Deutsche Bank. In repos, government bonds serve as collateral for the dollar loan. In FX swaps, foreign currency reserves serve as collateral to secure the dollar loan.

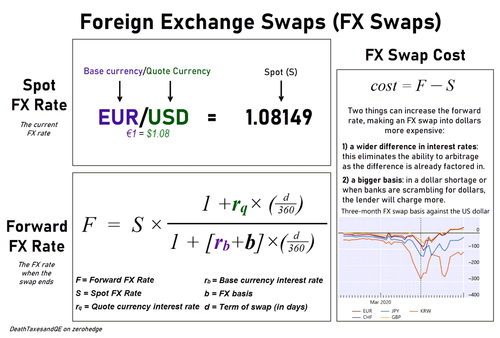

Exchange Rates and FX Swaps

The spot rate is the exchange rate of the day – for example, where is EUR/USD trading today? This is the price at which the currencies are initially exchanged.

The forward rate is the price at which the two parties to the transaction (e.g. Citi and Deutsche Bank) agree to “swap” the currencies at the end of the FX swap.

In this sense, the difference between the forward rate and the spot rate represents the cost of the FX swap.

The Opportunity and Cost of Currency Conversion

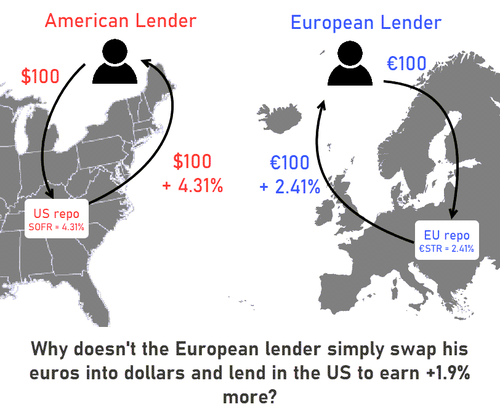

Let’s say I’m a European investor who earns 2.4% by lending euros within Europe. What’s to stop me from converting my euros into dollars, lending the dollars at a 4.3% yield in the US, and then converting them back into euros to earn a higher return? Absolutely nothing, but this strategy carries risks.

If EUR/USD rises during the trade, then my profits will be reduced or even eliminated when I convert them back into euros.

I can eliminate this risk by using an FX swap, but that means I have to pay the expected exchange rate, which increases as the interest rate difference between the two currencies increases.

If repo rates (i.e. the cost of money and the reference rate set by central banks) in Europe were equal to those in the US, then the expected and current exchange rates should be the same. The cost of the FX swap reflects the interest rate differences.

In the example above, we note that under normal circumstances, Deutsche Bank pays $0.51 to borrow $108.10 for three months. That means it would earn $0.51 more if it lent that money to the US instead of Europe, and that opportunity is already built into the pricing. But, as is often the case in markets, there is no such thing as a free lunch.

Demand, Supply, and FX Basis

Supply and demand is the most fundamental law in finance.

If everyone wants to own an asset, its price increases.

If lenders are in short supply, the price of money—i.e., interest rates—increase.

In foreign exchange markets, the same is true for the demand for dollars.

When there is high demand for dollars and/or lenders are reluctant to lend in dollars, FX swaps reflect this imbalance through the FX basis.

A negative FX basis means an increased need for dollars.

The FX basis is unique for each currency pair. For example, if European banks need more dollars than Japanese banks, the EUR/USD basis will become more negative than the JPY/USD basis.

In contrast, countries like Australia, which invest less in US assets, have a more positive AUD/USD basis, meaning Australian banks are net dollar providers.

In March 2020, everyone was scrambling to secure dollars, but the problem was even more acute for Korean banks, who were forced to pay extremely high interest rates as the FX basis of the Korean won collapsed.

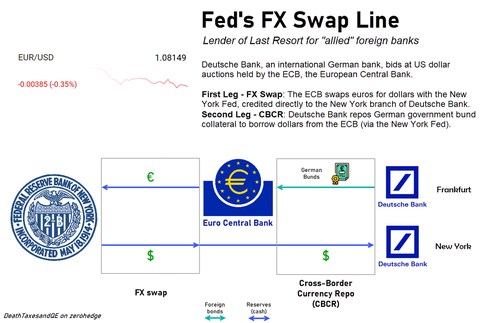

The Fed’s FX Swap Lines

When private FX swaps become too expensive due to a lack of liquidity and an increased FX basis, many banks can obtain dollars through the Fed’s FX swap line.

This is done through their local central bank, which enters into an FX swap with the Fed. For example, if Deutsche Bank needs dollars but private lenders in the US avoid EUR/USD FX swaps, the FX basis widens and expected rates rise, making the use of the FX swap expensive.

If the interest rate calculated by the FX swap increases from 4.31% to 6.31%, then most banks will consider the cost excessive. However, Deutsche Bank does not need to go through Citi – it can simply participate in the dollar auctions held by the European Central Bank (ECB).

Through the Fed swap line, Deutsche Bank essentially borrows dollars from the ECB.

It does not need to provide US Treasury bonds as collateral – it can use German government bonds (Bunds), but receive dollars in a special repo transaction with the ECB.

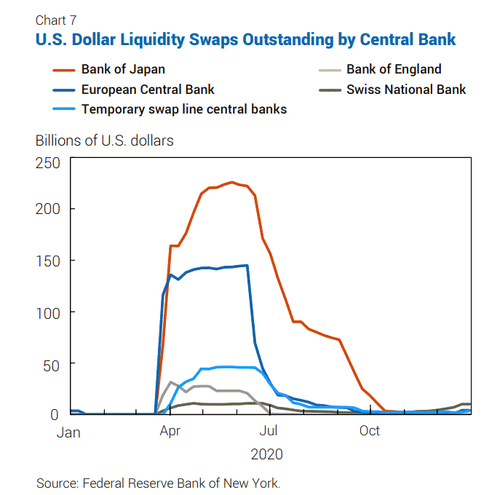

The Fed’s main and emergency FX swap lines

The Fed has five permanent FX swap lines, which are a key mechanism of the global dollar system:

Bank of Japan

Bank of England

European Central Bank

Swiss National Bank

Bank of Canada

On March 19, 2020, amid a liquidity panic, the Fed added nine temporary FX swap lines to support the global dollar supply:

Reserve Bank of Australia

Banco Central do Brasil

Danmarks Nationalbank (Denmark)

Bank of Korea

Banco de Mexico

Reserve Bank of New Zealand

Norges Bank (Norway)

Monetary Authority of Singapore

Sveriges Riksbank (Sweden)

Japanese banks have huge needs for dollars, as shown by their negative FX basis and heavy use of swap lines in 2020. Although Europe is less dependent on dollar liquidity than Japan or Korea, the removal of these swap lines could cause serious solvency problems in the European banking system.

But not all jurisdictions are allies and therefore not all have access to the Fed’s FX swap lines.

However, many of these jurisdictions, like every one of the “90+ countries” where Citi operates, still need dollars.

If a country has a surplus in its trade balance with the US (as is now the case with ASEAN countries, which suffered a dollar crisis in 1997), this is a source of dollars. The largest foreign banks have offices in New York, so when reserves held in large US banks (G-SIBs) are plentiful and funding costs are low, they first borrow dollars from private sources.

But what if the demand for borrowing dollars is not met by the supply?

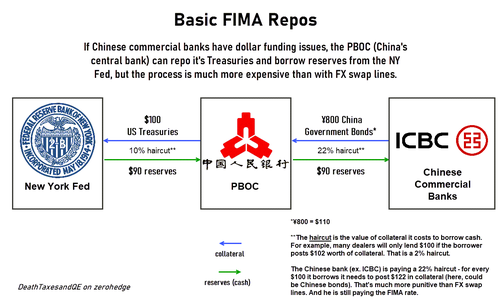

The cost of such funding can increase prohibitively or even skyrocket. Without central bank swap lines, what is the alternative? In March 2020, a new mechanism was created that provided dollars to banking systems that fell into this category.

It was called the Foreign and International Monetary Authorities (FIMA) Repo Facility and it gave foreign central banks access to Fed repos. Unlike FX swaps, it required the central bank to pledge US Treasury bonds as collateral instead of its local currency.

It may seem that only a few international banking systems fall into this category, that is, having large dollar needs but not being “allies”, however, 30 central banks (in addition to the 19 that had access to the FX swap lines) signed up and used the FIMA repo facility during the Covid pandemic.

It is also known as the “China Repo Facility,” as Chinese banks need dollars, and the People’s Bank of China (PBOC) has huge reserves of U.S. Treasury bonds—$760 billion today. Rather than depreciating the yuan or selling its dollar reserves in a tight situation, the PBOC can use them to raise liquidity through repos.

FIMA repos allow foreign central banks to “liquidate” their bonds without selling them directly to the market, thus avoiding potential turmoil.

This is particularly important for China, as it is a special case: it has large dollar funding needs but no access to the Fed’s swap lines. US banks are less willing to accept Chinese yuan as collateral in FX swaps, or at least not on favorable terms, which limits Chinese banks’ ability to raise dollars on international markets.

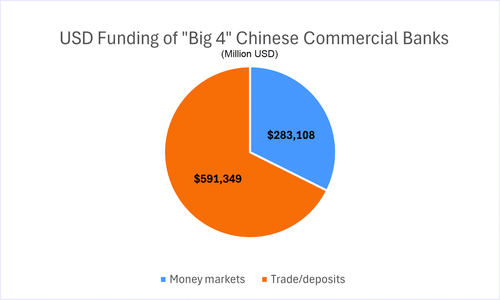

However, despite the obstacles, China has managed to secure dollars in the most classic way: through its trade surplus.

“Chinadollars”

Even without access to Fed swap lines and with fewer dollar lenders in the FX swap markets, Chinese banks have managed to manage their dollar funding because they maintain a stable trade surplus with the US.

As long as Chinese merchants continue to accept dollar payments from American customers and deposit them in Chinese banks, pressures for dollar financing in China only emerge during crises.

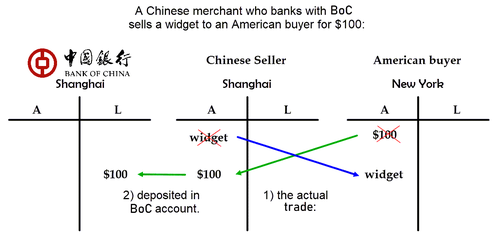

Bank deposits – the money that you, I, and everyone else use every day – are recorded as liabilities on banks’ balance sheets: it’s our money, and the banks owe it to us.

A Chinese trader who receives $100 from a transaction with an American will deposit that money into his account at the Bank of China (BoC).

These dollars, when deposited anywhere outside the US, are called “Eurodollars” (a misleading term, as they do not have to be in Europe). For simplicity, they could be called “Chinadollars”.

One of the most important features of the Eurodollar system is that bank deposits in dollars outside the US can act as a form of short-term financing and replace bank reserves. This is because every dollar deposit anywhere must have a corresponding dollar position – an asset that the bank can use for payments or withdrawals.

In the US, this usually takes the form of bank reserves at the Fed. Outside the US, it can be a claim on dollars held at a “correspondent” bank, usually in New York. The Eurodollar system has facilitated the expansion of dollar credit in China, affecting everything from local government bonds to cross-border loans for the Belt and Road Initiative.

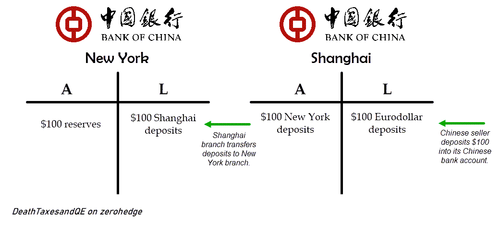

How the BoC handles those $100 million in Eurodollar deposits is critical. It has several options:

Of course, the BoC could convert those dollars into yuan through the PBOC. But as one of China’s largest banks, which deals in dollars every day, it would probably want to keep the dollars as dollars.

Like most major Chinese banks, the BoC has an international presence, including a branch in New York, where it maintains a reserve account with the Fed.

Foreign banks can transfer Eurodollar deposits from their offshore branches to a domestic branch.

This is the key mechanism that allows China greater autonomy in the dollar system, reducing its dependence on American banks – a change that Chinese banks have quietly implemented.

Dollar Shortage

Despite the fluctuations we’ve seen on the issue so far—where steep tariffs are imposed on some countries, only to be lifted days or even hours later after “successful negotiations”—the sweeping tariff wall that comes into effect will undoubtedly restrict the international flow of dollars.

Initially, this will appear dimly, as the understaffed US Department of Commerce (USTR) faces a huge workload in enforcing Section 301 tariffs, but the situation will evolve over time.

The market, however, continues to ignore this reality.

The tariff wall is focused primarily on China, targeting not only most of its industrial imports, but also countries it has used or could use to circumvent tariffs, such as Mexico and Canada.

To determine how the dollar shortage is spreading throughout the system, we need to consider which banking structures are most dependent on dollars and to what extent. Is there precedent for dollar shortages to hit some systems harder than others? Yes, there is.

During the Covid pandemic, dollar financing has been strained globally.

Lockdowns have disrupted global trade, leaving many businesses unable to repay their dollar-denominated debts — payments that foreign banks rely on.

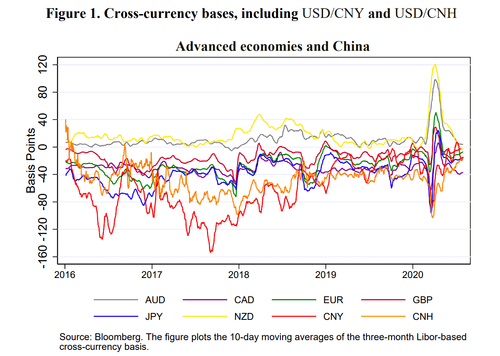

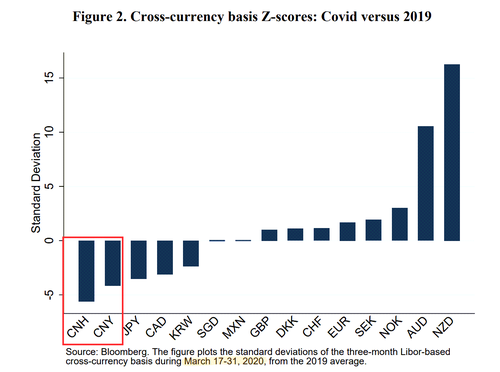

We can determine which banking systems were most vulnerable at the time by looking at the FX basis.

As mentioned above, when a foreign borrower needs dollars, they are willing to pay higher market interest rates.

In foreign exchange swaps (FX swaps), the more negative the spread, the higher the future interest rate and the more a foreign bank is willing to pay for dollars.

Australian and New Zealand banks are the exceptions, as they are US allies and invest less in dollar assets. We observe how the interest rate differential for most currencies collapsed in early March 2020, before rebounding on the day the Fed announced unlimited swap lines with 19 countries.

This announcement on March 19 reassured private lenders in the swap market, making financing easier for countries that did not have access to swap lines. However, after March 19, the interest rate differential for the Chinese currency (both CNY and CNH) remained well below 2019 levels—lower than any other major foreign currency.

This is a clear indication that, without access to swap lines and even at “normal interest rates,” Chinese banks were struggling to raise dollar funding.

The Covid pandemic was a special case, and much has changed in the intervening five years. Beyond the record trade balance with the US, China has diversified its use of the dollar in its imports.

It is striking to consider that until early 2020, China paid for almost all of its raw material imports in dollars—including those from Russia—a reality that has now changed dramatically. China’s trade surplus with the US remains its main source of dollar financing.

A balance of payments also includes capital flows (such as foreign direct investment, or FDI), but this is omitted here due to data ambiguity.

The 2016 decline mirrors August 2015, when Chinese authorities devalued the yuan. In effect, this made imports cheaper in dollar terms — it didn’t reduce the flow of value, but rather increased the value of dollars against the Chinese yuan.

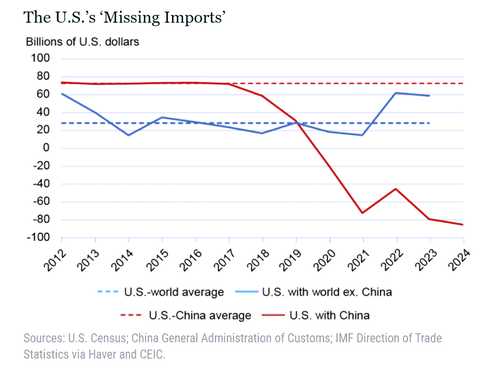

However, a significant portion of the trade surplus involves American companies manufacturing products in China’s “special zones,” with their profits never actually entering the Chinese system. In fact, this repatriated production explains much of the contraction since 2018 — not that fewer dollars were flowing into mainland China.

This makes it difficult to measure the impact of trade sanctions since 2018, as, according to balance of payments (BoP) data, the US deficit with China appears to have peaked in 2018 and never recovered. However, the New York Fed pointed out a year ago that while the US trade deficit with China fell from $375 billion in 2018 to $295 billion in 2024, the Chinese surplus with the US increased from $278 billion to $360 billion. This represents at least $65 billion in “missing imports.”

It is clear that China has circumvented trade barriers, mainly through “entrepot trade,” where Chinese goods are first shipped to pipeline countries like Mexico and Vietnam before being re-exported to the United States.

Thus, Chinese traders continue to earn dollars, even if this is not evident in the balance of payments accounts.

Contrary to what advocates of tough US sanctions believe, Chinese banks are well prepared to deal with a shortage of dollars until the United States is forced to change course.

Strengthening the Dollar & Hong Kong

China, of course, is fully aware and has been closely following America’s shift towards deglobalization, especially in trade, repairing its weaknesses in the process.

While the reality is that China cannot fully wean itself off the dollar, there have been significant moves in that direction, such as buying a neutral reserve asset – gold – to settle trade, as well as restructuring the balance sheets of its commercial banks.

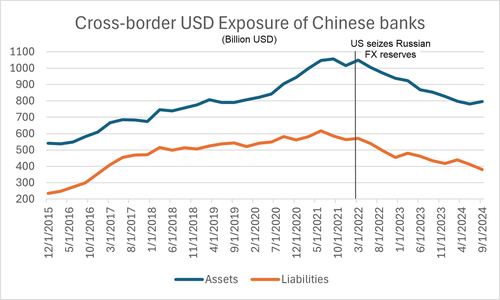

Below is the total “dollar book” of Chinese commercial banks, that is, the assets (such as claims on nostro accounts) and liabilities (such as dollars borrowed from New York) held outside China.

We can clearly see a gradual decline; and yes, the peak coincides with March 2022, around the same time that Zoltan Pozar predicted the birth of a multipolar financial system.

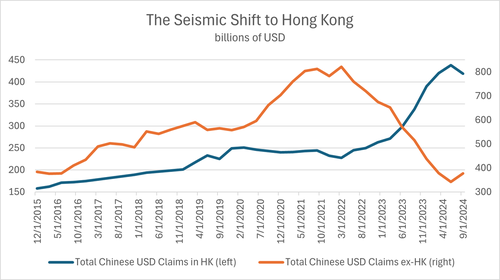

By analyzing the distribution of Chinese commercial banks’ cross-border dollar exposure, we can see that, although they have generally de-dollarized their balance sheets, many of their cross-border dollar claims have simply shifted, likely from New York and London, to the “international financial center connecting East and West” – Hong Kong.

The data showing the shift of dollar claims to Hong Kong is confirmed by two things.

CHATS, a large-value settlement system used by at least 30 Chinese financial institutions, saw dollar trading volumes double in 2023, matching the increase in cross-border dollar claims.

Could this simply mean that China wanted to avoid the watchful eyes of the US and therefore moved its claims from New York to Hong Kong? That’s what it seems.

One might say, “Don’t rush! These are claims in gold.” That’s probably true, as Chinese banks were buying gold in a frenzy in mid-to-late 2023 (to sell to the People’s Bank of China – PBOC), and the volumes on CHATS reflect that.

But if we look at the balance sheets of the largest banks with a presence in Hong Kong, such as Citibank Hong Kong, we also see an increase in their liabilities to foreign banks, which is consistent with the 2023 surge.

Potential Risk for US Banks

In 2023, during the period of the regional bank run, a group of four academics from different universities presented evidence showing that one of the four largest US banks, with assets of over $1 trillion, was essentially insolvent.

In the US, there are only four banks with assets of over $1 trillion: JPMorgan, Wells Fargo, Bank of America and Citibank.

With a small team of hedge fund analysts, we went through their financial reports in detail and found that the only bank that matched our findings was Citibank.

Citibank’s most recent reports show that 88% of its deposits are uninsured! This makes it extremely vulnerable to outflows. If Chinese banks need dollars, they will first draw from the Hong Kong reserve – which is mostly held by Citibank! This would mean a gradual “attack” on one of the largest US banks, which is already in a precarious position.

If Hong Kong banks are pressured, they will turn to the interbank markets for liquidity, increasing the cost of trading dollars.

If that is not enough, they will seek emergency funding from their parent banks in the US, possibly leading to forced asset sales, further worsening the financial situation.

If this happens to Citibank, it could trigger a broader banking crisis.

Gold, Tariffs, and the “Three Strategies”

Chinese culture is, to put it simply, deeply rooted in history. Henry Kissinger, in his book On China, describes how China sees itself as the center of the world and the greatest civilized power.

In the ancient Chinese strategic treatise Three Strategies, Huang Xigong identified three key principles for victory:

Moral Legitimacy (道德欃威) – Power must be based on popular support and morality.

Strategic Deception (詐) – As Sun Tzu said in The Art of War, deception and adaptability are crucial.

Military Power (武力 兵势) – The use of force must be decisive and applied when the time is right.

China appears to be implementing these principles:

Moral legitimacy: It is bolstering its gold reserves and promoting trade through alternative currencies.

Strategic deception: It is redirecting financial flows to make it harder for the US to deglobalize.

Military power: The interpretation of its moves is left to the reader.

Wall Street may be ignoring these elements, but China appears to be playing a long-term game, something that Western markets often underestimate.