Donald Trump’s economic policy aims to reduce US trade deficits with third countries and relocate the production base to the United States. At the same time, he has to deal with a monstrous public debt that has exceeded 36 trillion dollars and interest payments have exceeded defense spending for the first time! A tool for this strategy is the weakening of the dollar, while at the same time it should not lose its reserve currency status. A key problem with any attempt to substantially weaken the dollar is that, while the currency looks strong, it is difficult to argue that it is significantly overvalued. (It is estimated that it is about 10% overvalued on a real weighted basis). Previous attempts to realign exchange rates (including the Plaza Accord, which we will refer to) were most successful when they a) corrected the valuation bubble in the markets and b) were supported by policies to correct the underlying causes of the exchange rate misalignment. (It is often forgotten that as part of the Plaza Accord, the US committed to restrictive fiscal measures.) In this sense, the various financial solutions that have been proposed to weaken the dollar – from debt swaps to SWFs – are the market’s tail chasing the economic dog. None of them address the fundamental cause of trade imbalances. The final way in which U.S. policymakers could address the imbalances is to target capital flows. While we have focused on the current account balance, it is forgotten that every foreign transaction represents a corresponding capital flow. The dollar’s global role drives demand for U.S. assets, pushing up their value and hurting exports. Restricting capital inflows – such as through withholding taxes – could help reduce the current account deficit. If this also weakens the dollar, it could boost export competitiveness and improve the trade balance. But this would not come without a cost. Capital controls would jeopardize the dollar’s status as the global reserve currency, which relies in part on a large and readily liquid market for dollar-denominated assets that can be traded at low cost.

Austerity is inevitable

And the dollar wouldn’t have to lose its reserve to have significant macroeconomic consequences. A drop in global demand for dollar-denominated assets would, among other things, raise the cost of borrowing in the United States, leading to lower domestic demand and lower output.

And while the Fed could respond by cutting interest rates, that would only partially offset the pressure on consumer spending. For all Donald Trump’s complaints about America’s trading partners, the flip side of the US current account deficit is the willingness of foreigners to lend large sums to the US, allowing it to consume more than it produces.

Squeezing capital flows into America means squeezing consumption by Americans. With the US now at full employment, the inescapable truth is that any short-term effort to create space for higher net exports would mean that consumption in other parts of the economy would have to be reduced.

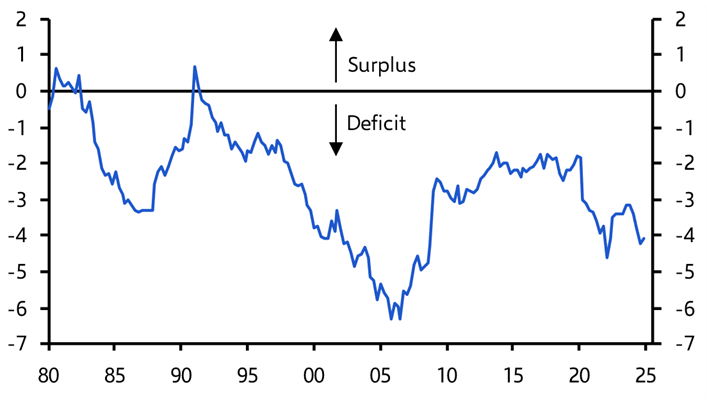

The US trade balance is shown in the bottom graph

The Historical Context

Let’s look at the issue in its historical dimensions. The Mar-a-Lago Accord comes in the wake of three major international monetary agreements since the original Bretton Woods agreements of 1944.

- The first was the December 1971 Accord. It came about after President Richard Nixon decided on August 15, 1971, in agreement with the United States’ trading partners, to end the convertibility of the dollar into physical gold at a fixed exchange rate of $35.00 per ounce. The major countries of the global monetary system (the United States, the United Kingdom, France, Germany, Italy, Japan, the Netherlands, Sweden, Switzerland, Canada, Belgium, and the Netherlands) met at the Smithsonian Institution in Washington to decide how to reopen the gold “window.”

The main goal of the United States was to devalue the dollar. In the end, the price of gold rose by 8.5% to $38.00 per ounce (revalued to $42.22 per ounce in 1973), which was equivalent to a 7.9% depreciation of the dollar. Other currencies also appreciated against the dollar, including the Japanese yen by 16.9%. The attempt to reopen the “gold window” failed. Instead, major countries turned to floating exchange rates, which remains the norm to this day.

Gold is traded on the open market and currently hovers around $3,050 per ounce. The current price of gold represents a 98.8% depreciation of the dollar in terms of gold since 1971.

- The period from 1971 to 1985 was turbulent in the foreign exchange markets, including the petrodollar agreement (1974), the collapse of the Herstatt Bank (1974), the sterling crisis (1976), US hyperinflation (50% from 1977-1981), a major global gold price boom (1908), and a major global recession (1981-1982). By 1983, inflation was low, the dollar had made significant gains, and the US enjoyed strong economic growth under Ronald Reagan.

The next major economic meeting on exchange rates was the Plaza Accord in September 1985. It was convened by US Treasury Secretary James Baker at the Plaza Hotel in New York and included the US, Germany, the UK, Japan and France. At the time, the dollar was at an all-time high against other currencies. The dollar had also strengthened against gold, which had fallen in price from $800 per ounce in January 1980 to around $320 per ounce in 1985.

The aim of the meeting was to gradually devalue the dollar. In this respect, the meeting was a success. It is important that the method of devaluation was to be gradual and to be achieved by interventions by the central bank and the Treasury in the foreign exchange markets. In practice, market interventions were quite limited. Once investors got the message, they took the dollar where it needed to go on its own. No investor would want to be on the wrong side of the trade if central banks decided to intervene on a particular day.

- The Louvre Agreement, signed on February 22, 1987, between the United States, the United Kingdom, Canada, France, Japan, and Germany, was, in effect, a confirmation of the success of the Plaza Accord.

Between 1985 and 1987, the dollar depreciated against other currencies. The dollar also depreciated against gold, which rose from $320 per ounce to $445 per ounce by the time of the meeting. The mission for Treasury Secretary James Baker had been accomplished. The purpose of the Louvre Agreement was to “lock in” the achievements of the Plaza Accord, stop further depreciation of the dollar, and return to a period of relative stability in the foreign exchange markets. This agreement was also successful.

The dollar was mostly stable after 1987, despite the introduction of the euro in 2000 (the euro jumped between $0.80 and $1.60 in the early 2000s. Today it is $1.09, not far from its original parity of $1.16). The other wild card was gold. After hitting a low of around $250 an ounce in 1999, gold surged to $1,900 an ounce in 2011, a 670% gain and a de facto depreciation of the dollar. The period of relative stability in currency markets lasted until 2010, when President Barack Obama launched a new currency war.

A New Mar-a-Lago Accord

Which brings us to the discussion of a possible new international monetary conference in the chain of conferences from the Smithsonian Accord and the Plaza Accord to the Louvre Accord. Given Donald Trump’s dominance of the global financial scene, and his love of… ornate architecture of the kind seen at the Plaza Hotel (Trump owned the Plaza Hotel from 1988 to 1995), it’s not hard to expect him to convene any new global monetary conference at his equally famous Mar-a-Lago in Florida.

The first discussion of a Mar-a-Lago Accord appears in Chapter Six of James Rickards’s book Aftermath (2019), published 6 years before the current juncture. This chapter is titled “The Mar-a-Lago Accord” and includes a discussion of the evolution of the international monetary system that began in 1870, including the more recent agreements noted above.

It then includes his private meetings with IMF Managing Director John Lipsky and Treasury Secretary Tim Geithner, focusing on a possible new gold standard and the attempt to replace gold with the Special Drawing Rights (SDRs), created in 1969 and used by IMF members ever since. It ends with Pierpont Morgan’s classic 1912 quote that “money is gold and nothing else” and recommends that investors acquire physical gold for their portfolios.

The dollar value of gold has increased by 120% since its introduction. The current hype about the infamous “Mar-a-Lago Accord” began with a November 2024 paper written by Stephan Miran, who was appointed chief economic adviser to Donald Trump, entitled “A User’s Guide to Restructuring the Global Trading System.” Although the title refers to the trading system, it explains how currency depreciation can be used to offset the impact of tariffs and refers to “the persistent overvaluation of the dollar.” From there, it jumps to the Plaza Accord and the need for a new Mar-a-Lago Accord.

Issuance of 100-Year Bonds

In the section on monetary developments (pages 27-34), Miran not only proposes a devaluation of the dollar, but also that the United States issue 100-year bonds.

In Miran’s view, 100-year bonds would be attractive to foreign exchange managers and would reduce any dollar sales required to support their own currencies. These long-term dollar holdings would mitigate the short-term depreciation of the dollar in a way that would regulate the international monetary system as a whole, ensuring long-term equilibrium.

Miran specifically uses the term Mar-a-Lago Accord to describe his proposed system for monetary changes.

There are many more technical details in Miran’s plan, including the use of the Treasury’s Transaction Stabilization Fund, the Fed’s Liquidity Financing and Provisioning Program, and the Fed’s swap lines. Miran also proposes using the International Emergency Economic Powers Act of 1977 (IEEPA) to impose withholding taxes on interest payments to foreign holders of Treasury securities (a form of capital controls since it imposes a burden on foreign investors to own bonds) as a way to discourage trading partners from owning bonds and thereby devalue the dollar. Trading partners would be rated using a “traffic light” system. Countries would be rated green (friendly), yellow (neutral), and red (hostile). Green countries would receive U.S. military protection and the most favorable tariffs, yellow would receive reciprocal tariffs, and red countries would receive no security assistance, punitive tariffs, and possible capital controls.

There are many more technical details in Miran’s plan, including the use of the Treasury’s Transaction Stabilization Fund, the Fed’s Liquidity Financing and Provisioning Program, and the Fed’s swap lines. Miran also proposes using the International Emergency Economic Powers Act of 1977 (IEEPA) to impose withholding taxes on interest payments to foreign holders of Treasury securities (a form of capital controls since it imposes a burden on foreign investors to own bonds) as a way to discourage trading partners from owning bonds and thereby devalue the dollar. Trading partners would be rated using a “traffic light” system. Countries would be rated green (friendly), yellow (neutral), and red (hostile). Green countries would receive U.S. military protection and the most favorable tariffs, yellow would receive reciprocal tariffs, and red countries would receive no security assistance, punitive tariffs, and possible capital controls.

An Economic Disaster in Progress

In reality, Miran wants to devalue the dollar while keeping the dollar at the center of the International Monetary System. Nixon did this in 1971 and Baker in 1985

The success of the Plaza Accord depended entirely on close cooperation between the major countries’ treasury departments. There is no such cooperation today, given sanctions on Russia, tariffs on China, and the EU’s disengagement from the US over the war in Ukraine.

Since Miran’s work, the issue has completely spiraled out of control. A recent MarketWatch headline says: “Wall Street Can’t Stop Talking About the Mar-a-Lago Deal.”

Some analysts suggest that the gold on the Federal Reserve’s balance sheet (actually a gold certificate) will be revalued from $42.22 per ounce at market price (now $3,050 per ounce with the general account). Another idea is to use U.S. assets such as land and mineral rights as collateral against U.S. debt.

At this time, no one knows what a Mar-a-Lago Deal would actually be or if it would happen, so it is impossible to predict the impact. However, the most well-known version of the plan would have unintended consequences that could lead to a global economic disaster.

You don’t have to force holders to exchange short-term debt for long-term. You just let the short-term debt mature and replace it with new 100-year bond issues through the existing underwriting system. There is no need for coercion as there would be huge demand for the 100-year debt. Depreciating the dollar does not combat the potential inflation that the tariffs will cause. It actually causes inflation by raising the cost of imported goods. Any increase in the price of gold on the Fed’s books is just an accounting entry.

You don’t have to force holders to exchange short-term debt for long-term. You just let the short-term debt mature and replace it with new 100-year bond issues through the existing underwriting system. There is no need for coercion as there would be huge demand for the 100-year debt. Depreciating the dollar does not combat the potential inflation that the tariffs will cause. It actually causes inflation by raising the cost of imported goods. Any increase in the price of gold on the Fed’s books is just an accounting entry.  The proposed “inspection” of Fort Knox by Trump and Elon Musk (if it happens…) will be nothing more than a staged media event. Gold has a global price completely unaffected by the accounting games between the Treasury and the Fed. Again, the Mar-a-Lago Deal, as currently envisioned, would cause a global financial crisis. This is because it fails to understand the importance of short-term Treasury debt as collateral for interbank lending and derivatives. Replacing 100-year Treasury debt with short-term Treasury bills would make those bills scarce. Treasury bills are the most liquid collateral in the world and are the foundation of the Eurodollar system and the $1 trillion derivatives market. The scarcity of Treasury bills would destroy bank balance sheets and lead to the biggest banking crisis in history. The big winner in this context is gold. The BRICS are moving into gold as fast as they can. Investors will follow…

The proposed “inspection” of Fort Knox by Trump and Elon Musk (if it happens…) will be nothing more than a staged media event. Gold has a global price completely unaffected by the accounting games between the Treasury and the Fed. Again, the Mar-a-Lago Deal, as currently envisioned, would cause a global financial crisis. This is because it fails to understand the importance of short-term Treasury debt as collateral for interbank lending and derivatives. Replacing 100-year Treasury debt with short-term Treasury bills would make those bills scarce. Treasury bills are the most liquid collateral in the world and are the foundation of the Eurodollar system and the $1 trillion derivatives market. The scarcity of Treasury bills would destroy bank balance sheets and lead to the biggest banking crisis in history. The big winner in this context is gold. The BRICS are moving into gold as fast as they can. Investors will follow…