The new logic in relation to the financial crisis

If the Fed extends these lines to Gulf countries such as the United Arab Emirates, Qatar and Bahrain, it will be based on a different logic than in the past. In 2008, the swap lines were given to central banks of the G7 countries (European Central Bank, Bank of Japan, Bank of England, etc.), as well as to smaller developed countries with close ties to the US (Switzerland, Sweden, Denmark). They were then extended to some emerging economies such as Mexico, Brazil and South Korea, which were considered important for the US and had reliable institutions. In the minutes of the Fed’s closed meetings of that period (2007–2008), which were later published, geopolitical factors do not appear as a key criterion. The emphasis was on the risk that dollar disruptions in these markets would negatively affect the U.S. economy. In the past, swap lines were a tool to maintain dollar dominance, based on concerns about the stability of the U.S. financial system—not a means of bolstering allies in a complex geopolitical environment.The geopolitical support for the dollar

The issue is less about economics than politics, and is a sign of how the US is trying to maintain the dominance of the dollar in a changing geopolitical environment. In practice, foreign central banks exchange their domestic currencies for dollars. The US Treasury has limited ability to open such lines, while the Federal Reserve (Fed) has more resources. The Fed maintains standing swap lines with the central banks of key allies, such as Canada, Japan and the European Union, and in times of crisis—such as at the beginning of the pandemic or during the 2008 financial crisis—it has expanded the network.

A signal of discontent over the war

Swap lines could support the ability of Gulf countries to continue investing in the United States under petrodollar agreements and, politically, strengthen their ability to meet large investment commitments that the White House often makes. For countries that seek to be seen as major players in the global dollar system, access to such mechanisms is also a sign of weakness. At the same time, the demands also serve as an indirect signal of discontent over the war. Swap lines are ideally suited to countries with strong and reliable economies, as they involve risks: the United States provides dollars in exchange for foreign currency, which is at risk of depreciation. For this reason, counterparties must be carefully selected to avoid losses for taxpayers. Nevertheless, extending these mechanisms to more countries could strengthen the international dominance of the dollar. Overall, dollars may be exchanged, but in reality much more is at stake.The petroyuan emerges as a factor of monetary stability

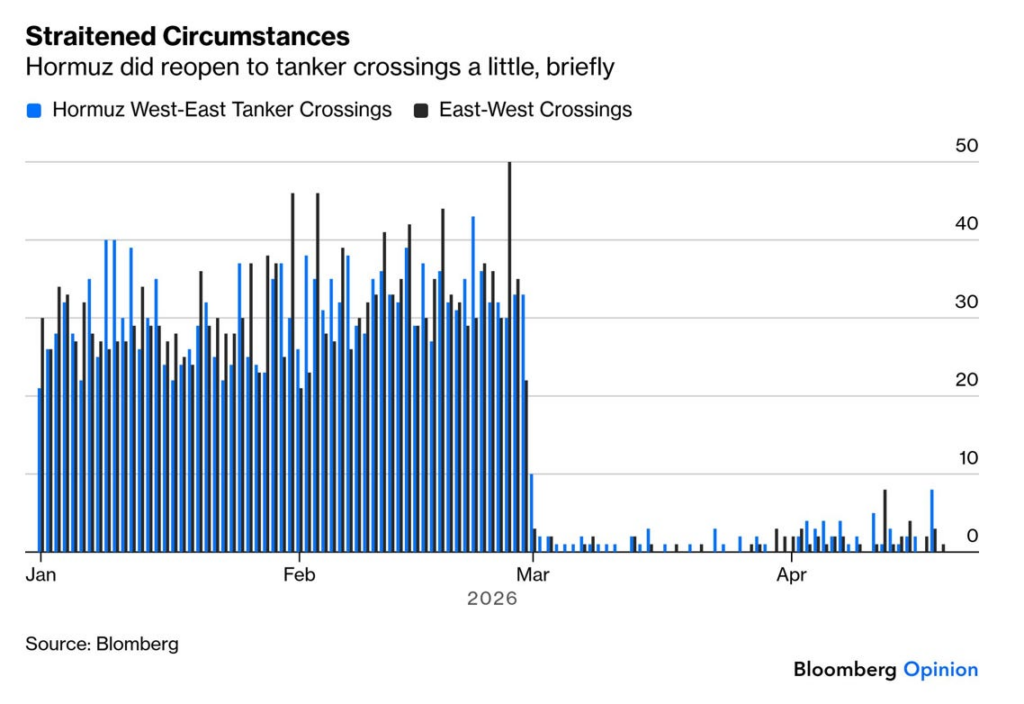

The petroyuan is also emerging as a financial powerhouse because, under pressure, states need an alternative way to complete transactions. This distinction is important, because it will determine how the petroyuan will evolve relative to the petrodollar. Most analyses still view this shift as gradual and structural: a slow erosion of the dollar’s dominance, reflected in reserves and payments shares over time. But the data do not support this as the main mechanism. The dollar still accounts for about half of global payments via SWIFT, and almost 60% if intra-eurozone transactions are excluded. The yuan remains in the low single digits. In foreign exchange reserves, the gap is even wider. These numbers are real, but also misleading, because they describe stability at the core of the system and say little about what happens at the periphery — when the system is under stress. Energy markets operate in this “periphery.” About a fifth of the world’s oil supply passes through the Strait of Hormuz, while Asia depends on Middle Eastern oil for about half or more of its imports. When this flow is disrupted, the question is not which currency dominates, but which can clear the transaction. That’s where the petroyuan comes in. Recent transactions provide a clear indication: Indian refiners have already settled cargoes from Iran in yuan under US sanctions, while African banks are creating direct yuan settlement channels to avoid going through the dollar. These are not ideological moves but operational decisions. That is why the petroyuan will not develop linearly, but will strengthen in waves. The next phase is likely to occur within the next 12 months. A new disruption in the Gulf’s energy supply—whether due to shipping restrictions, tighter sanctions, or military escalation—will force some of the oil flows outside long-term contracts and established supply chains to switch to alternative settlement channels. In such a scenario, the use of the yuan will increase sharply — not universally, but enough to affect flows and price formation. It will then likely decline as tensions ease, dollar channels reopen, and liquidity is restored. At first glance, it will appear that nothing has changed. That reading will be wrong. Each episode leaves “traces”: more counterparties will be willing to trade in yuan, more banks will be able to intermediate in that currency, and more businesses will hold yuan. The infrastructure for the petroyuan will gradually expand in the background.

The Decline of the Dollar System

The system will not be overturned abruptly — it will decline gradually. This will create a pattern for which markets are not prepared: intermittent, crisis-driven increases in the use of the petroyuan, each time larger and more efficient. Foreign exchange markets are based on marginal flows. They respond not to the volume of trade, but to changes in the “periphery.” If even a small portion of energy trade moves away from the dollar in a crisis, then the way in which stress is transmitted to the financial system changes. In a typical oil shock, the demand for dollars increases immediately. Importers need financing, businesses hedge risks, and banks tighten liquidity. The result is synchronized: the dollar strengthens rapidly and broadly. With parallel settlement channels, this uniformity is fractured. Many transactions will continue to require dollars, but more and more will not. Demand becomes uneven as part of the system settles transactions through alternative routes. The result is not a collapse of the dollar, but a distortion in the way monetary pressure is transmitted: dollar gains will be less “clean,” funding pressures less synchronized, and prices less predictable. That is where the first substantial impact will be seen—not on reserves or market shares, but on the behavior of markets in times of stress. Second, when a solution proves effective in a crisis, it becomes part of normal practice. Financial operations do not return to a single-currency system when they discover viable alternatives. They maintain flexibility and diversify settlement channels. Thus, temporary adjustments become permanent features. The petroyuan does not need to displace the dollar to be significant; it just needs to perform reliably when the dollar system is under stress. This threshold is lower than many investors believe. The petroyuan will mature through repeated episodes of geopolitical tension. Each crisis will expand its use, each calm period will cover it — and the cycle will repeat itself at an ever higher level. Over the next three years, this process will become evident in market behavior. Energy shocks will no longer trigger a single, immediate increase in demand for dollars, but a more fragmented and gradual response. By then, the transition to the petroyuan will be well established.Please follow and like us: