Investors around the world spent much of 2024 worrying about China’s problems with the housing market and deflation. In 2025, it’s the US’s turn to be the star of the negative scenarios. While Donald Trump’s trade war is making headlines, the rapid decoupling between US net foreign investment and the level of federal debt is expected to take center stage. And forcing the incoming Treasury team to come up with a plan to stabilize the US economy, facing the serious possibility that the world’s largest economy will pay a high price for fiscal mismanagement by both investors and credit rating agencies. Until now, Washington has been able to avoid confronting reality — and living wildly beyond its means. However, this current account imbalance may become more difficult to finance during the Trump 2.0 era that begins on January 20.

- One reason is the reduced time horizon due to Washington’s chronic complacency. The bill for President Joe Biden’s post-Covid-19 spending spree to stimulate consumption is looming as foreign investors show less appetite for U.S. assets.

- Another is the risk stemming from Trump’s planned extravagance of tariffs. These two dynamics are set to clash in spectacular and unpredictable ways — and at a time when buyers of U.S. national debt are reluctant to increase exposure to a volatile dollar.

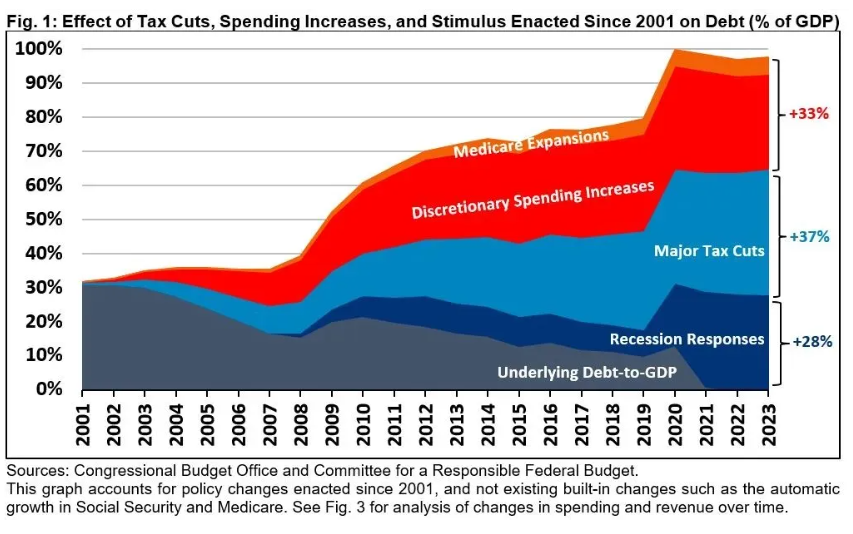

As Biden prepares to hand over the reins to President-elect Trump, he leaves the incoming administration with a U.S. national debt that exceeds $36 trillion. Trump’s desire to make permanent the $1 trillion in tax cuts from his first term, 2017-2021, and add more will only make the problem worse. Currently, the size of the U.S. net foreign investment position—the difference between foreign assets held by Americans and U.S. assets held abroad—is nearly the size of U.S. GDP. It is negative $24 trillion, compared with a negative $18 trillion when Trump left office in 2021.

The Trump Administration’s Dilemma

However, under Trump 2.0, the US will face a dilemma: push the fiscal deficit further into the red or devise a strategy to reduce Washington’s reliance on imports. So far, the Trump team seems more willing to take the former route than the latter.

Further tax cuts would increase America’s reliance on the savings of developing countries in Japan, China, and the Global South. His tariffs and trade barriers would fuel US inflation and curb consumption.

That could mean slower U.S. growth and less demand for Chinese goods at a time when Beijing is grappling with weak retail sales and deflation. Chinese households may have even less ability to buy U.S. goods. It could also increase the chances that China will weaken the yuan to keep its exports competitive, starting a massive currency war. If other countries retaliate, overall U.S. exports—and global trade overall—could fall. In addition, high U.S. tariffs would fuel domestic inflation, forcing the Federal Reserve to raise interest rates, which would likely cause the dollar to appreciate, which in turn would lead to lower exports and higher imports.”

That could mean slower U.S. growth and less demand for Chinese goods at a time when Beijing is grappling with weak retail sales and deflation. Chinese households may have even less ability to buy U.S. goods. It could also increase the chances that China will weaken the yuan to keep its exports competitive, starting a massive currency war. If other countries retaliate, overall U.S. exports—and global trade overall—could fall. In addition, high U.S. tariffs would fuel domestic inflation, forcing the Federal Reserve to raise interest rates, which would likely cause the dollar to appreciate, which in turn would lead to lower exports and higher imports.”

The Twin Deficits

Trump is also set to increase the US budget deficit, as he has promised sweeping tax cuts without making spending cuts to make up for the lost revenue.

As budget deficits erode national savings and investment, the trade deficit will also widen.

The rising cost of goods, combined with possible supply-side constraints on the labor market as a result of Trump’s proposed immigration policies, could also lead to a one-percentage-point increase in inflation. Of course, Trump will point the finger at others, accusing Washington’s trading partners of “damping” goods or maintaining artificially low exchange rates.

Unless Trump takes a prudent approach to tariffs on imports from the rest of the world, the US will be the one to be limited, both in terms of economic dynamism and global influence. Adding to the uncertainty, Trump has signaled that he will create a weaker dollar exchange rate and put pressure on the Federal Reserve to ease monetary policy. Neither trend bodes well for global inflation, America’s creditworthiness, or investor confidence in the dollar.

Falling Demand for U.S. Bonds

As 2025 begins, all eyes are on Moody’s Investors Service, the only major credit rating agency that still has a AAA rating for the U.S. economy. That could change quickly if the next U.S. Congress plays games with the debt ceiling or forces a government shutdown to score political points.

All of this comes against the backdrop of declining foreign demand for U.S. government debt. For more than a decade now, foreign official institutions have been reducing their holdings of U.S. bonds. Domestic financial institutions have been filling the gap.

The problem is that a sharp decline in U.S. stocks could make domestic assets less attractive to foreign buyers, sending funds into the red. This would make it even more unlikely that U.S. financial institutions will be able to finance a public deficit of 6% of GDP.

Trust Economics shows how America must reduce its addiction to imports

The “key” is to

1. increase productivity,

2. revive entrepreneurial innovation, and

3. create a new model of production.

That means increasing training to strengthen human capital, incentivizing a new generation of industrial entrepreneurs, and improving infrastructure.

It also means investing more in semiconductors, artificial intelligence, and other areas to bring innovation to the fore. The ways in which Boeing, General Motors, Intel, and other pioneering brands are in danger of decline should prompt Washington to try to revitalize corporate America.

The War on Manufacturing

Biden has shifted somewhat toward building more manufacturing capacity. The Trump 1.0 era was all about… stumbling China in the race. Biden has focused more on easing up to compete with China through organic economic growth.

Case in point: The (Semiconductor) and Science Act that Biden signed into law in 2022. It allocated $300 billion to boost domestic R&D.

It also took steps to incentivize innovation, increase America’s semiconductor capabilities, and increase productivity.

It marked a shift from the Trump era, which focused on a $1.7 trillion tax cut that did little to boost competitiveness or increase domestic manufacturing capacity. If Trump’s tax regime boosted innovation and productivity, US inflation might not be rising at a rate of 2.7% annually.

Regulations are driven by the industries they target, not the public interest

Biden has kept most of the trade restrictions of the Trump 1.0 era, which he estimates are reducing U.S. GDP by $55.7 billion, reducing wages, and costing full-time equivalent jobs.

During Trump’s first presidency, the U.S. trade deficit soared to its highest level since 2008, rising from $481 billion to $679 billion. Washington’s expansionary fiscal policies mean the U.S. will continue to spend more than it produces, perpetuating “the root cause of the trade deficit.” The import tax is, therefore, effectively a tax on exports.

The impact is both direct, through raising the cost of goods imports, stifling productivity-enhancing competition, and provoking international retaliation and worsening terms of trade, and indirect, through currency appreciation.

Unfortunately, neither the Trump 1.0 era nor Biden developed credible plans to compete with Beijing’s multi-trillion-dollar push to lead the future of electric vehicles, robotics, semiconductors, renewable energy, artificial intelligence, biotechnology, aviation, high-speed rail, and other sectors. Instead, Biden has also resorted to tariffs, reinstating policies from the 1980s, when such policies might have worked.

Donald Trump has long been trapped in that era, in which Japan played the hostile role that China has today. Between 2017 and 2021, Trump’s advisers tried to repeat what happened in the financial crisis of the 1980s. They failed, as did Trump’s top Asian ally in Tokyo.

Then-Prime Minister Shinzo Abe also believed that the recipe for greater prosperity was rising stocks. But wages did not rise as much as they needed to, undermining the broader economy.

The dollar problem

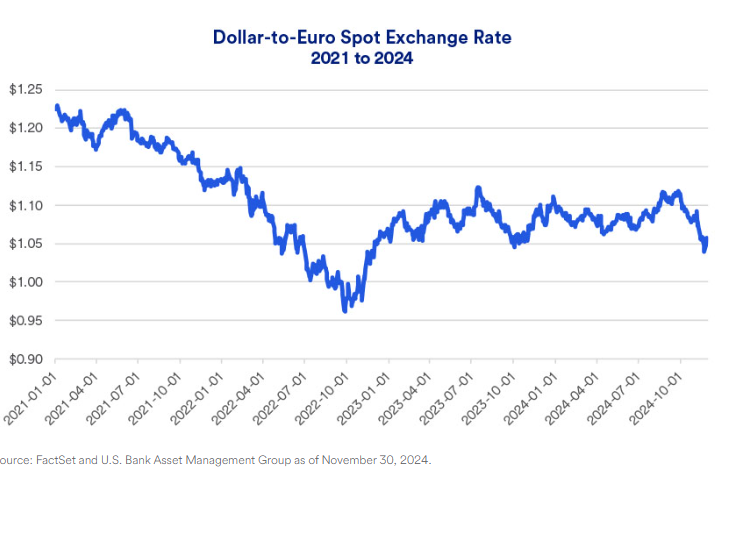

The barrage of tariffs that Trump is now promising may come just as his incoming administration is grappling with what has been called the “dollar problem.” In recent months, Trump “has demonstrated a clear preference for a weaker exchange rate to support the competitiveness of U.S. exports and help reduce the U.S. trade deficit.”

And yet, as the market has sensed since the U.S. election, the far more likely outcome is that his policies will end up strengthening the dollar. The risk is that the dollar – which is already expensive – will become more overvalued, and that could increase the risk of global financial instability.

The dollar probably has plenty of room to keep rising, as it is not yet overvalued. The U.S. current account deficit – the broadest measure of a country’s trade deficit and a rough but useful measure of financial vulnerability – was just over 3% of GDP last year. This is about half the level reached in 2006, just before the 2008 global financial crisis, meaning that the risks arising from an overvalued dollar may concern the latter part of Trump’s second presidency.

A strong dollar can often be bad news for the global economy. It tends to slow the growth of world trade, restricts developing countries’ access to international capital markets, and makes it harder for countries whose currencies are weakening to keep inflation under control. If and when the dollar becomes unsustainably expensive, a further problem will arise: how to deal with an overvalued currency without risking major economic damage. It is unclear how Trump’s desire for a weaker dollar might be realized, and what it might mean for Asia or Europe by 2025. But the plan to reverse decades of American fiscal mismanagement in the era of Trump 2.0 could be in jeopardy as Washington sends huge headwinds and openly perceives it as a threat.

A strong dollar can often be bad news for the global economy. It tends to slow the growth of world trade, restricts developing countries’ access to international capital markets, and makes it harder for countries whose currencies are weakening to keep inflation under control. If and when the dollar becomes unsustainably expensive, a further problem will arise: how to deal with an overvalued currency without risking major economic damage. It is unclear how Trump’s desire for a weaker dollar might be realized, and what it might mean for Asia or Europe by 2025. But the plan to reverse decades of American fiscal mismanagement in the era of Trump 2.0 could be in jeopardy as Washington sends huge headwinds and openly perceives it as a threat.

- The Plaza Accord was signed on September 22, 1985, at the Plaza Hotel in New York, between France, West Germany, Japan, the United Kingdom, and the United States, to devalue the U.S. dollar against the French franc, the German mark, the Japanese yen, and the British pound sterling by intervening in foreign exchange markets. The U.S. dollar depreciated significantly from the time of the agreement until it was replaced by the Louvre Accord in 1987. Some economists believe that the Plaza Accord contributed to Japan’s asset price bubble of the late 1980s.