Geopolitical Inflation and Deflationary Globalization

For more than fifteen years, global markets have operated within a system based on extremely low government bond yields, cheap money, and structurally low inflation. Central banks have so distorted the value of money that investors have increasingly been pushed into stocks, technology companies, and speculative assets simply to secure returns. But this framework is now beginning to unravel. The world is moving from a regime of deflationary globalization to a regime of geopolitical inflation. Globalization has reduced labor costs, extended supply chains, reduced production costs, and allowed central banks to maintain extremely low interest rates for decades. However, this model is being dismantled under the pressure of- tariffs,

- industrial policy,

- increased defense spending,

- economic protectionism in supply chains, and intensifying geopolitical competition.

The role of the conflict in the Middle East

The conflict in the Middle East is further accelerating this process. Brent crude has risen above $110 a barrel as the war with Iran intensifies and the risks to Gulf energy infrastructure increase. Asia remains particularly vulnerable because it is heavily dependent on imported energy. Japan, South Korea, and India absorb inflationary shocks through energy prices much more readily than the United States. Higher oil prices are quickly passed on to production and transportation costs, food inflation, and consumer demand. At the same time, governments are now borrowing on a wartime scale. Japan is reportedly preparing new debt issuance to finance emergency fiscal spending related to the conflict. The United States continues to run huge deficits despite high interest rates and persistent inflation, while Europe is also increasing defense spending as fiscal pressures mount.

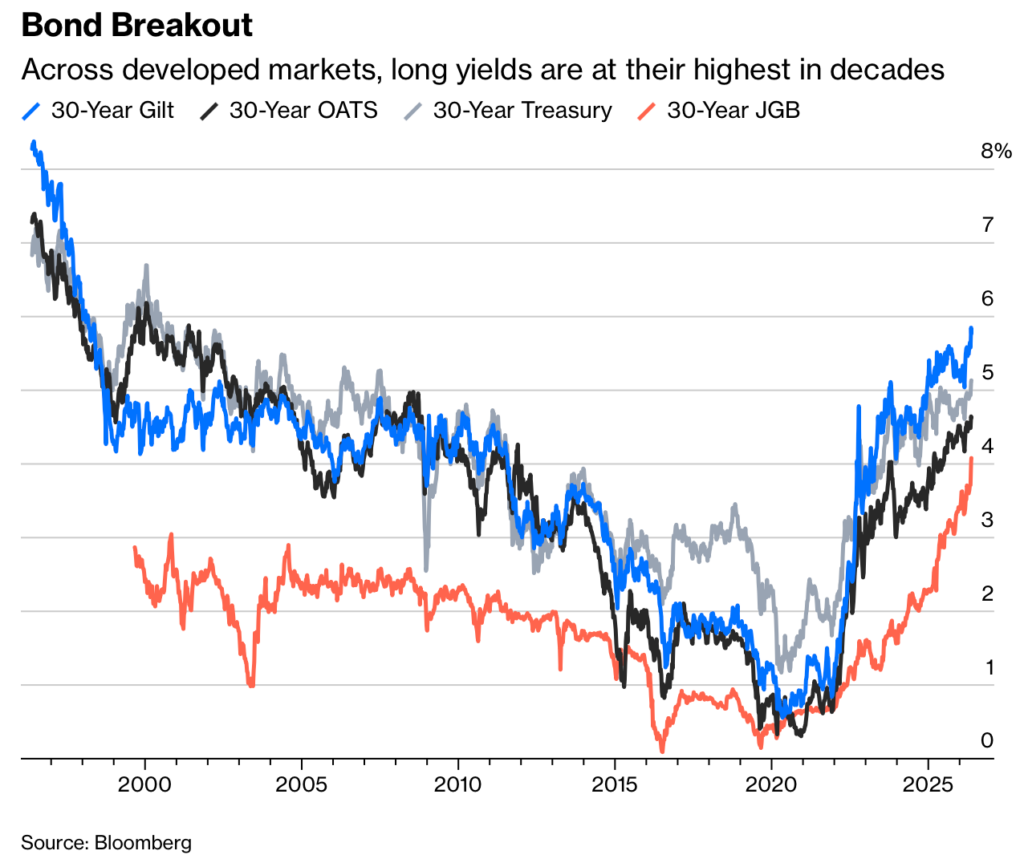

The post-2008 certainties are over

Investors are now beginning to question whether sovereign debt paths remain sustainable in an environment of structurally higher interest rates. That’s why, according to the analysis, the bond market decline matters far beyond fixed income markets themselves. The investment model of the post-2008 period was based on the assumption that liquidity would remain abundant, inflation would remain under control, and capital would continue to be cheap. Bond markets are now challenging all three of these assumptions at once. Some Asian economies may be better positioned to adapt to the new environment. India continues to benefit from its demographic momentum, domestic consumption, and expanding industrial production, while Indonesia and Vietnam are attracting investment related to the diversification of supply chains. At the same time, Singapore may further strengthen its role as a financial safe haven in times of geopolitical instability. However, broader Asian markets remain highly sensitive to international liquidity conditions, sovereign borrowing costs and the strength of the dollar. The era of “free money” inflated almost every major asset class at the same time. The regime that succeeds it will be much more selective, much more volatile and much less forgiving. Investors who continue to treat Asia as if there is still infinite liquidity may end up positioning themselves for a world that will no longer exist.Please follow and like us: