Government bond prices collapsed globally as investors rushed to bet on higher interest rates after major central banks showed renewed concern that rising oil prices would trigger an inflationary shock.

Three weeks after the start of the Iran war, the fallout has put upward pressure on short-term bond yields, defying until recently widespread expectations that central banks would cut rates this year to boost growth.

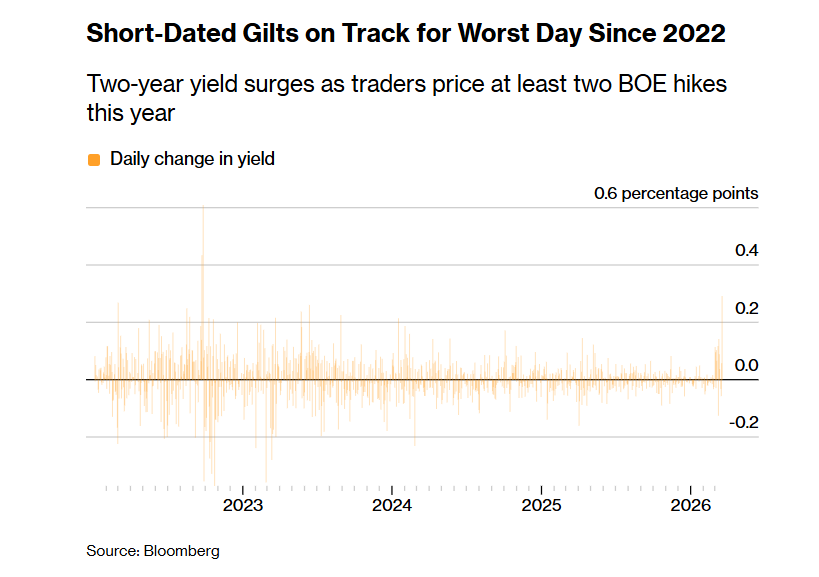

The sell-off was led by the United Kingdom, where the rise in yields was somewhat reminiscent of 2022, when former Prime Minister Liz Truss’s fiscal plans sent the debt market into a tailspin.

The yield on two-year bonds rose as much as 40 basis points to 4.49% after the Bank of England said on Thursday (19/3) that it “stands ready” to act to prevent inflation from accelerating.

The depth of the decline eased as the trading day progressed, while longer-term bonds remained largely unaffected. However, yields on short-term German bonds rose by about 14 basis points as investors maintained bets that the European Central Bank will raise interest rates at least twice this year.

In the US, yields on two-year US Treasury bonds rose by 10 basis points to 3.87% after comments from Federal Reserve Chairman Jerome Powell led investors to expect interest rates to remain steady throughout the year.

The market decline – which was mainly focused on short-dated securities that are more sensitive to monetary policy changes – highlighted how quickly the global outlook has changed since the US launched a war with Iran late last month.

Before that, investors had expected the Fed to cut interest rates twice this year, while the BOE was expected to do the same to support a weakening UK job market.

However, the war in the Middle East and disruptions to global energy and trade have defied those expectations, with the conflict showing no sign of ending anytime soon.

Oil and gas prices rose further on Thursday (19/3) as intensifying attacks in the Persian Gulf threatened long-term damage to major energy facilities.

In the US, although the Fed still expects a 0.25% rate cut this year, markets now see this as unlikely.

Statements by central bankers last week suggest they are largely focused on upside risks to inflation, even as rising energy prices threaten to slow economic growth.

This stance appears to have bolstered confidence that central banks will ultimately rein in consumer prices, leaving long-term bonds relatively stable while short-term bonds have fallen.

Tight monetary policy

The European Central Bank kept interest rates unchanged for a sixth meeting. However, markets still expect tighter monetary policy later this year to curb inflation, even as its president, Christine Lagarde, also highlighted the risks to growth from the war. ECB policymakers are ready to raise rates even at their next meeting if inflation rises significantly above target.

BoE Governor Andrew Bailey said policy must “address the risk of more persistent effects on UK consumer price inflation.” Although UK bonds recovered from the day’s lows, two-year yields remained more than 30 basis points higher.

“Central banks are starting to adjust their guidance away from rate cuts and toward hikes on the back of higher inflation expectations,” said Thanos Chonthrogiannis of Trust Economics. “So far, they have been giving more weight to the inflationary impact of the energy shock than to the potential impact on unemployment.”

A more dovish stance was also evident in Japan, where yields rose slightly after Bank of Japan Governor Kazuo Ueda left open the possibility of a rate hike in April.

In the United States, where the central bank has a dual mandate to protect the labor market and contain inflation, Powell said further progress in reducing inflation was needed before interest rate cuts could resume.

However, the possibility that the Fed could intervene if the economy slows may have limited the extent of the bond market decline. Still, futures are no longer pricing in a single rate cut this year.

At the same time, labor market data remains subdued, with hiring and layoffs both on the rise. In short, the market is increasingly concerned about stagflation.

What do the data show?

Treasury bonds, particularly U.S. Treasuries, have long been seen as a safe haven during recessions, geopolitical crises, and other market-shaking events.

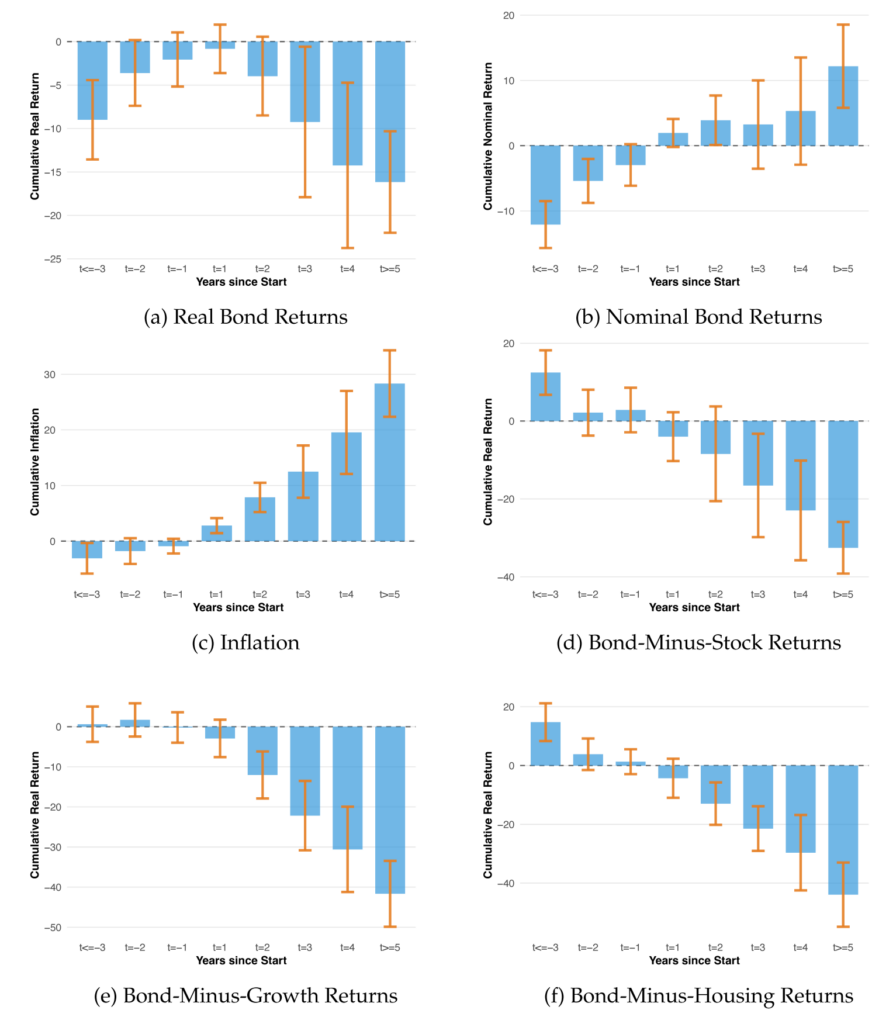

However, looking back over 300 years in the U.S. and U.K. history, the Center for Economic Policy Research found that wars and pandemic-scale crises have taken a toll on bondholders.

“The historical evidence reveals a striking pattern: government bonds have repeatedly generated significant real losses during these extreme periods,” wrote Zhengyang Jiang, Hanno Lustig, Stijn Van Nieuwerburgh, and Mindy Xiaolan.

“Indeed, they have underperformed stocks and real estate, which are traditionally considered riskier assets.”

That’s because wars typically trigger large increases in government spending — averaging about 7% of GDP per year in the first four years — while tax increases are rarely enough to cover financing needs.

The finding comes as the United States is at war with Iran, and the national debt has ballooned to $39 trillion. The Pentagon is seeking more than $200 billion to finance the conflict, according to sources.

According to the research, bondholders suffered an average real loss of about 14% in the first four years of the wars. The losses were so great that they reduced the real value of the entire national debt.

And as if that weren’t enough, cumulative bond returns were more than 20% lower than stock and real estate returns — the opposite of what usually happens in financial crises or recessions.

A key driver of the losses is inflation, with its cumulative rate averaging about 20% in the first four years of the wars.

In the current US-Israeli conflict with Iran, Treasuries and other government bonds have fallen sharply as rising oil prices fuel expectations of higher inflation and worsening budget deficits.

Since the war began three weeks ago, the yield on the 10-year US Treasury note has risen more than 40 basis points.

However, increased spending is not the only reason why inflation is hitting bonds. According to the research, it is often the result of policy choices aimed at reducing debt without a formal default — such as suspending the link to the gold standard.

Another reason is so-called “financial repression,” policies that keep interest rates artificially low through market intervention, preventing bond yields from keeping pace with inflation.

For example, during World War II, the Federal Reserve implemented yield curve control, limited Treasury interest rates, and engaged in massive bond purchases.

The findings are particularly relevant to U.S. debt today, as Treasuries remain the backbone of the global financial system, with the dollar serving as the global reserve currency.

This regime allows the U.S. to borrow more cheaply than markets would normally allow. However, interest on the U.S. debt is now the fastest-growing component of the budget, already reaching $1 trillion a year.