China’s economic slowdown is drawing a lot of attention in Manhattan boardrooms. While Asia’s largest economy is not faltering, its 4.8% growth rate in the third quarter—the slowest this year—is sending up warning signs everywhere.

Even the positives come with (serious) asterisks. For now, external demand is keeping China on track for this year’s 5% economic growth target. But amid rising trade tensions—including a looming 130% tariff from the United States—it’s easy to see why many see China as one of the biggest downside risks to U.S. growth—and indeed to all Western economies.

Stephen Miran, a senior economist on Trump’s staff, is firmly in that category. The newest member of the Federal Reserve board is not just worried about the deflation that Xi Jinping’s economy is exporting – due to excess capacity and modest consumption.

He also fears the economic fallout if Beijing uses its control over rare earth metals as a weapon in retaliation for U.S. President Donald Trump’s tariffs.

“I had been operating on the assumption that the uncertainty had dissipated and therefore I felt more optimistic about some aspects of the growth outlook,” Miran told CNBC.

“Now, potentially, that is coming back because the Chinese are backing out of deals that had already been made. So I think it is incumbent on us as policymakers to think about introducing a new tail risk” (from the “tail” of the probability distribution curve – that is, extreme, unlikely but very serious events).

In this context, Miran, who served as Trump’s chief economic adviser, is advocating for further rate cuts of 125 basis points.

“To the extent that I think policy is quite accommodative right now, that makes us vulnerable to shocks,” Miran noted. “If you get a shock when policy is very accommodative, the economy will react differently than it would if policy were not so accommodative. I think it is even more important now than I thought a week ago to move quickly to a more neutral stance,” meaning to put a short end to the Fed’s monetary tightening process.

Trust Economics analyses report that “deflation in China has reinforced deflationary forces in advanced economies in recent years, reducing the consumer price index by about 0.3-0.5% on average. Tariffs will likely reverse this trend in the US. But elsewhere, policymakers will likely seek to preserve some of the benefits of lower prices for consumers while protecting key sectors from increasing competitive pressures.”

The Monster of Over-Indebtedness

However, the real danger may be that China will lose its balance, at a time when the United States is not exactly on a positive path.

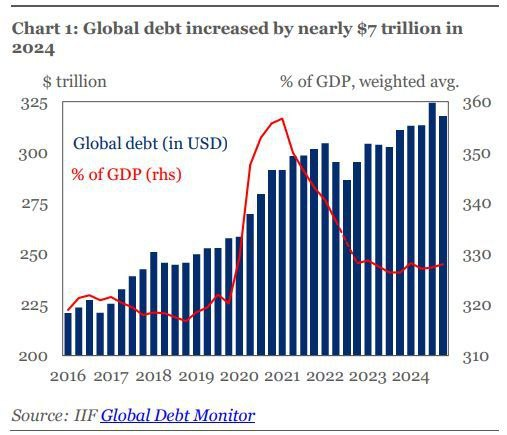

Having the world’s two largest economies, with a combined annual economic output of $50 trillion, at odds with each other is not in anyone’s best interest. Especially developing countries, whose total debt stood at $109 trillion in the second quarter, according to the Institute of International Finance (IIF).

Moreover, global debt reached a record high of $337.7 trillion at the end of June, partly as a result of easing global financial conditions as many central banks became less accommodative.

The IIF reports that global debt levels rose by more than $21 trillion in the first half of 2025, with China, France, the United States, Germany, the United Kingdom and Japan recording the largest increases.

“The scale of this increase was comparable to the surge seen in the second half of 2020, when pandemic response policies led to an unprecedented accumulation of global debt,” the IIF said. The increase in military spending will further strain government budgets amid rising geopolitical tensions.

However, bond market reactions have been more chaotic in more advanced economies. For example, yields on 10-year bonds in the G7 countries are near their highest levels since 2011.

The only constant… volatility

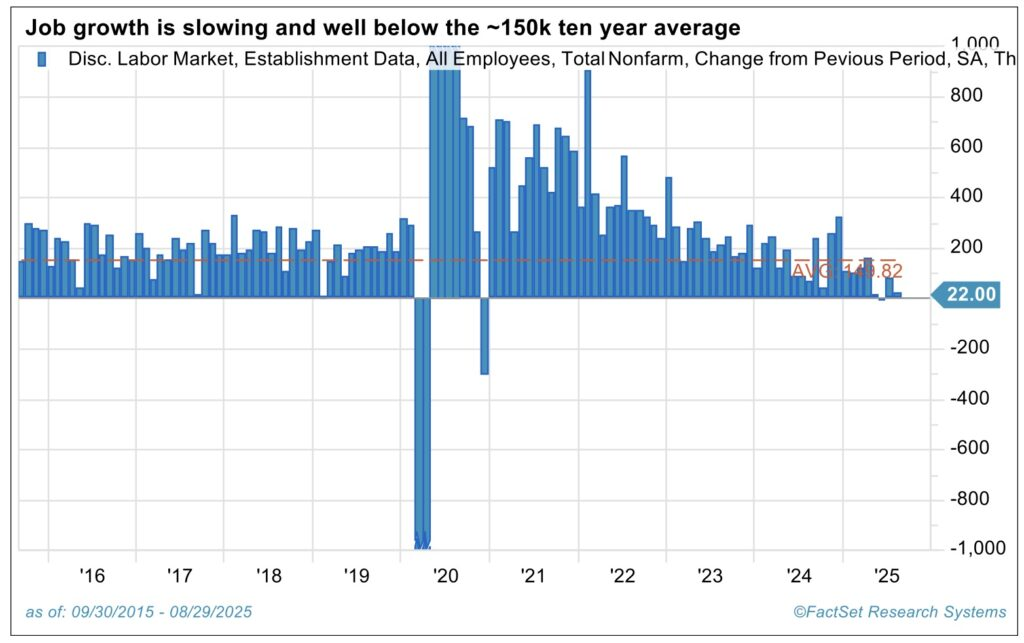

The volatility of the world’s largest economies is hard to ignore. Employment in the US is slowing at an alarming rate. Trust Economics economist Thanos Chondrogiannis believes that “US growth of 3.8% in the second quarter and 3.3% in the third quarter may be overstated based on the weakening of employment. The expected change in the unemployment rate over the next year has never been this bad outside of recessions since the University of Michigan began studying the question in 1978. Given that labor market indicators often provide more reliable information about current growth than preliminary GDP estimates, this weakness reinforces our belief that the second and third quarter data send an overly positive message.”

In the eurozone, industrial production weakened in August, amid growing uncertainty among industrial companies affected by the global trade war. Output fell by 1.2% month-on-month, up from 0.5% in July. The outlook for industrial production remains poor for the foreseeable future. August reinforced the view that the eurozone economy barely grew in the third quarter, a similar slowdown to the second.

The double trap for Japan

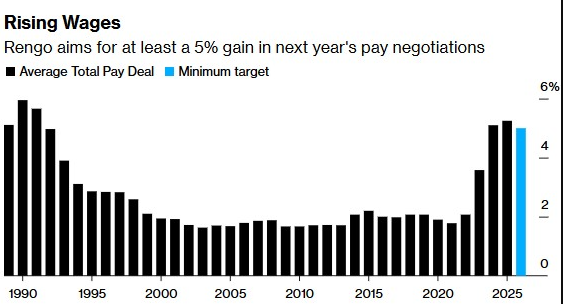

Japan “is caught between a worsening trade outlook and fragile domestic demand.” “Exports and industrial production are falling as tariffs hit and foreign competitors squeeze manufacturers. At home, persistent inflation and weak wage increases are undermining household spending power. And the government is holding back major investment spending.”

Inflation will eventually ease, but slowly, as producers continue to gradually pass on cost increases to consumers. This will take real wage growth and, with it, a substantial recovery in domestic demand. Policy uncertainty at home and abroad adds to the concerns.

Japan’s economic outlook looks challenging. Trade tensions, geopolitical rifts and the possibility of further disruptions to supply chains remain at the top of the list of risks.”

The China Problem

China’s ambitious growth target of “around 5%” this year is increasingly having a Trump problem. Every time the US president raises tariffs on mainland Chinese goods — 130%, at least for now — it makes it harder for Xi Jinping to avoid the fate of Beijing in 2022 and 1990, the only two times in the past 35 years that China has missed its GDP growth target.

There is reason to believe that Xi can achieve the seemingly impossible in 2025, provided the Communist Party mobilizes a two-pronged response to Trump’s unilateral “tariff war.”

The first leg is a wave of targeted fiscal stimulus to offset the strong headwinds that are looming.

The second is to encourage China’s 1.4 billion citizens to save less and consume more.

The only uncertainty surrounding the first goal is the scale of measures Xi’s team is willing to implement to boost consumption, stabilize the housing market, and end deflation. The pressure is mounting.

China’s consumer spending, in general, is estimated at about $7 trillion. Annual exports to the U.S. are about $450 billion. If Trump’s tariffs wipe out, say, half of that, Xi will have to rely mostly on domestic consumption to fill the gap.

That’s possible, according to Trust Economics, as long as Beijing acts quickly and boldly. Increased fiscal spending could be complemented by cuts in interest rates and reserve requirements.

In March, Beijing announced new fiscal measures, including a higher fiscal deficit target of about 4% of GDP, from 3% in 2024. The broader deficit will support the economic outlook, but it remains uncertain how large the fiscal stimulus will be or whether it can sustainably boost domestic demand.

Deflationary pressures in China remain persistent.” In addition, “political uncertainty in the United States remains elevated. It seems unlikely that measures to support consumption will be fully sufficient to offset weaker exports. As a result, negative consequences from overcapacity look set to worsen, intensifying downward pressure on prices and the problem of deflation. All of this adds drama to this year’s summit of top Chinese Communist Party officials.

The so-called “Fourth Plenary Session” will outline development plans through 2030. Consumption is likely to be the focus of the 15th Five-Year Plan, given the government’s continued emphasis on boosting consumption by 2025. But the key indicator of the seriousness of the leadership’s intentions will be whether the five-year plan goes beyond rhetoric, presenting a realistic plan to boost consumption.

This summit could prove crucial to Xi’s desire to shift China decisively toward high-value-added industries.

Central to this shift is building stronger social safety nets to encourage households to spend more and save less.

Xi’s inner circle has signaled moves ranging from reducing regulations, boosting the birth rate and subsidies for certain exports, to creating a stabilization fund to support the stock market.

But the real priority must be building the social safety nets that the central government and local governments have been promising for years.

Meanwhile, China’s vulnerabilities are adding to the reasons why officials around the world are bracing for downside risks as 2026 approaches—including Federal Reserve officials in Washington.