The increasing frenzy in gold purchases by central banks suggests that the effects of Donald Trump’s fiscal policy are only just beginning to be felt. As the world’s leading monetary authorities accumulate gold at historically high prices, the real goal of the above move is to reduce exposure to the dollar.

This dynamic belies US President Donald Trump’s claims that his multi-trillion dollar tax cuts are self-financing and highlights the fact that the US fiscal position is deteriorating (with all that that means…). It is also a response to the policy of retaliatory tariffs.

The Washington-based Committee for a Responsible Federal Budget (CRFB) calls the “Big Beautiful Bill” that Republicans just passed the House as the most expensive “reconciliation” bill in history: It would add $4.1 trillion to the national debt by 2034. If the temporary provisions are made permanent, that amount jumps to $5.5 trillion.

A reconciliation bill is a special type of legislation in the United States that deals primarily with fiscal issues, such as spending, taxes, and the federal deficit.

It is used to speed up the passage of economic measures by Congress and allows the bill to pass the Senate with a simple majority (50+1 votes), bypassing the possibility of a filibuster (blocking legislative action), which usually requires 60 votes.

As the Trump Treasury Department draws up plans to finance the huge public spending, it will necessarily have to rely on China and the rest of Asia with which it has large trade deficits — they are, after all, the largest holders of US public debt. Many of them, such as Japan and South Korea, are now facing what are known as “retaliatory” tariffs.

What are the gold markets showing?

Things are not going according to plan, judging by the trends in the gold market. China, for example, is not known for being a bull market hawk. Yet that is exactly what the People’s Bank of China (PBOC) did, increasing its official gold reserves for the eighth consecutive month in June, even as prices were near record highs. The PBOC’s holdings of the precious metal rose by 70,000 ounces last month.

Since the current wave of central bank purchases began in November, the PBOC under Governor Pan Gongsheng has added 1.1 million ounces, or about 34.2 metric tons, to its reserves.

And that is despite gold having surged more than 26% since the start of the year. It’s no coincidence that this rally — and the accumulation of the precious metal by central banks — intensified after Trump’s election victory in November and the official start of the Trump 2.0 era in January.

That’s prompting China to reconsider its overall reliance on the dollar. China’s net gold purchases this year have reached 19 metric tons. Trump, after all, returned to power with even bigger plans to curtail the independence of the Federal Reserve and accelerate the ballooning of the U.S. national debt to and beyond $30 trillion.

That makes it difficult for economists to assess the true trajectory of U.S. fiscal policy. The dollar’s recent 13% decline appears to be accelerating.

But the issue is not that simple, as in some circles there is also a surge in demand for the dollar due to Trump’s new 50% tariffs on copper and Brazil.

Central banks buy gold to diversify their reserves, reduce dependence on the dollar and hedge against inflation risk and uncertainty over economic developments. It is “a trend that we believe will continue, especially amid uncertainty around tariffs and the US budget deficit,” Trust Economics notes.

Central bank gold purchases mainly come from governments that are not particularly friendly to US interests, including China, Egypt, Hungary, India, Kazakhstan, Kyrgyzstan, Pakistan, Turkey, Uzbekistan and Gulf states such as Qatar.

The BRICS countries (Brazil, Russia, India, China and South Africa) have made no secret of their desire to move away from the main reserve currency. The push to create an alternative currency may now accelerate as Republicans — and now Trump himself, in a highly personal way — ratchet up the pressure on Brazil.

Trump has linked the 50% tariff to what he calls Brazil’s “attacks” on American technology companies and its “witch hunt” against former President Jair Bolsonaro.

The Trump ally is being prosecuted for his alleged role in efforts to rig the 2022 election. BRICS members may see this attack as part of US efforts to use its economic dominance as a geopolitical weapon.

Economic warfare

Trump’s threats to punish countries that consider using other currencies have not been well received by currency markets.

And while Congress recently abandoned a plan that would have allowed the White House to impose taxes on companies and individuals from “unfriendly” countries, there is serious concern that such efforts may return.

The idea “challenges the openness of US capital markets by explicitly using taxation on foreign owners of US assets as a lever to advance US economic goals,” says economist Thanos Chonthrogiannis of Trust Economics.

This use of US capital markets as a weapon, he adds, creates the possibility that the US could turn a trade war into a war on capital flows if it so chooses.

The problem is that this tactic has become so common that foreign investors can no longer ignore it. There are costs to being seen as using the dollar as a weapon.

Case in point: freezing an adversary’s access to its foreign exchange reserves, as the Biden administration did to Russia after its invasion of Ukraine. The more the US uses this tool, the more other countries will seek currency diversification for geopolitical reasons.

In 2022, Congress gave the Biden administration the authority to seize Russian dollar-denominated assets to help Ukraine. The so-called REPO provision allowed then-Treasury Secretary Janet Yellen to transfer Russian state assets to a Ukrainian reconstruction fund.

This has reignited debate about the long-term costs of abusing the dollar’s dominance.

The Role of the BRICS

For now, the dollar remains dominant for many reasons: it is the most liquid currency, it is freely traded, and it remains the world’s primary means of borrowing. However, as Trump increases pressure on the BRICS, this could accelerate the move away from the dollar.

Globally, BRICS members control more than 40% of central bank dollar reserves. Their determination to reduce their reliance on the dollar includes a domestic push to create a single currency among themselves. As the BRICS countries seek ways to strengthen their financial ties, Beijing has been among the most enthusiastic advocates of diversifying their reserves.

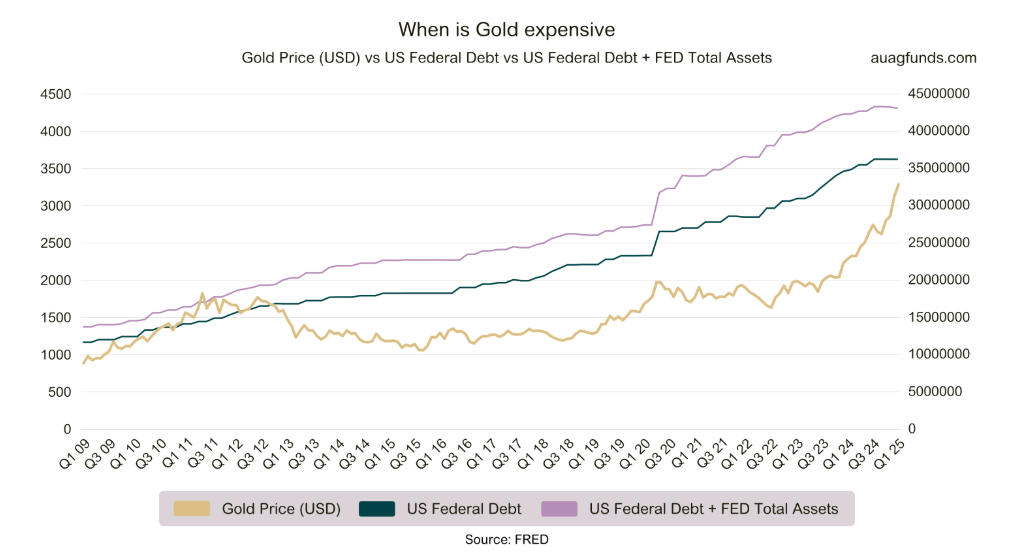

China’s accelerated gold purchases come amid the chaos of Trump’s trade war and the ballooning US federal deficit.

In recent years, China has also been reducing its holdings of U.S. Treasuries. Its current holdings stand at $760 billion, leaving Japan as Washington’s main lender in Asia. Today, Tokyo holds about $1.1 trillion in U.S. Treasuries.

The smell of the 1929 crisis…

Are we in a similar environment to that of the 1929 crisis, that is, the beginning of the Great Depression? In recent years, we have seen frequent comparisons with infamous economic crises, such as the inflation and recession of the 1970s. References have also been made to the Great Depression during the lockdowns due to the health crisis, when the price of gold also saw huge jumps.

But today, the price of gold is almost double what it was at the beginning of the lockdowns, which may confirm this particular question-theory. This view, rather than adopting the view that the openings of the economy prevented a 1929-style crisis, considers that we are simply in the early stages of a new global economic recession.

The reason is the US “debt trap”, given that gold may already have surpassed the dollar in importance as a reserve currency for central banks. Demand for long-term US government debt has reached historic lows. Very few are willing to bet that the dollar, in 20 or 30 years, will still be a desirable asset.

The economy is no longer growing (and there are doubts whether it can), while an annual budget deficit of more than 6% is a serious sign of stagnation. Also approaching the idea of the gold-war dichotomy, the dollar and US debt are actually the preferred refuge in times of armed conflict.

This, in turn, makes the US economy even more vulnerable if or when the threat of war disappears, as investors begin to pull out of US assets.

It is believed that China’s “de-dollarization” narrative aimed at strengthening the yuan was simply a way to paint a better picture for the dollar – whose role as the global reserve currency cannot be directly challenged.

We see this unfolding month after month, with a recent report revealing that 32% of central banks expect to buy gold in the near future. The situation is so critical that central banks are even starting to accept other currencies as reserves – as long as they reduce their exposure to the dollar.

In addition to being undervalued, COMEX open interest suggests that gold may still be in the early stages of a very bullish trade, which makes the rally to $3,500 all the more remarkable.

It’s the first time since 1977 that U.S. assets have fallen overall while gold prices have risen — but, he said, perhaps the comparison to 1929 is more apt.

Central banks buy gold because they have a particular view of the future — and that view doesn’t seem to include the currencies they print as “real money.”

The role of silver shouldn’t be overlooked. There have been well-documented allegations of silver price manipulation for over two decades, with JPMorgan often named as a primary culprit.

China’s silver reserves may be even more impressive than its gold reserves. The Shanghai Gold Exchange, as a reminder, is wholly owned by the People’s Bank of China (PBoC) and appears to function primarily as a tool for the state to acquire more gold, while at the same time restricting information about these markets.

Gold may be entering a summer doldrums, interestingly its price is twice as high as it was in the summer doldrums two years ago. Not much has changed in terms of fundamentals since then, so we have to ask ourselves what investors can expect over the next two years.

And if we are indeed in a 1929-style economic environment, which is just not so hidden, what can investors in turn expect in gold over the next decade? The only fact is that Donald Trump, with his fiscal policy and trade war, made gold great again.