The European Central Bank (ECB), especially after the Greek adventure, has a long history of intervening in government bond markets in order to contain yields during periods of turmoil in the debt market.

However, this is not an exercise of monetary policy but an intervention by the Brussels deep state. The most characteristic — and perhaps the most extreme — of these occurred in July 2022, when the combination of post-pandemic inflation and Mario Draghi’s resignation as Italian prime minister caused Italian yields to rise sharply due to the rise in political risk. The ECB’s purchase of Italian debt was so large that it effectively wiped it out of the market.

At the same time, there were public interventions regarding lending conditions: an extraordinary meeting of the ECB was held and the new tool against the fragmented debt market (Transmission Protection Instrument – TPI) was presented, which institutionalized the ECB’s intervention when yields deviate from what it considers to be a justified level.

In short, the ECB “threw all its weapons into battle” for Italy in 2022.

It should be noted that the TPI (Transmission Protection Instrument) is the tool introduced by the ECB in 2022 and its purpose is to protect the “smooth transmission” of monetary policy in bankers’ parlance — that is, to prevent large divergences between the interest rates of the Eurozone countries.

In simpler words:

If the interest rate on Italian bonds rises much more than that of German bonds, the ECB can buy Italian bonds to “close the gap”. . This is a politically charged tool, because it gives the ECB the ability to determine which countries “deserve” protection and which do not – let us remember that such a mechanism was never activated for Greece.

Thus, the ECB is transformed from a neutral central bank into a fiscal risk manager at the discretion of the Brussels clergy. At the same time, the activation of this tool does not mean, of course, subjection to international financial control, as happened in Greece, but extensive fiscal adjustment measures.

Is it possible to ultimately rescue a bankrupt economy? What remains to be seen is whether their implementation is politically feasible by any government that emerges, as the opposition as a whole does not seem willing to accept deep cuts in fiscal policy beyond some concessions on the pension.

The ECB’s problematic intervention creates substantial distortions

After the outbreak of the COVID-19 pandemic, Christine Lagarde temporarily abandoned the “capital key” rule as part of the Pandemic Emergency Purchase Programme (PEPP). This meant that the ECB could buy more bonds from countries with high debt, such as:

Italy,

Spain,

and now France.

The aim was to avoid a sharp rise in their bond yields — which would increase the cost of borrowing and could trigger a debt crisis. This practice:

distorts the market,

reduces pressure for fiscal discipline,

and ultimately politicizes monetary policy.

This type of intervention is extremely problematic for several reasons.

It creates the expectation among politicians that the ECB will always be there to bail them out in times of crisis — thus reducing the pressure to reduce public debt.

At the same time, it causes complacency in financial markets, as they too begin to believe that there is an ECB “safety net” (the so-called ECB put).

Perhaps most importantly, however, these monetary practices have the character of direct political intervention.

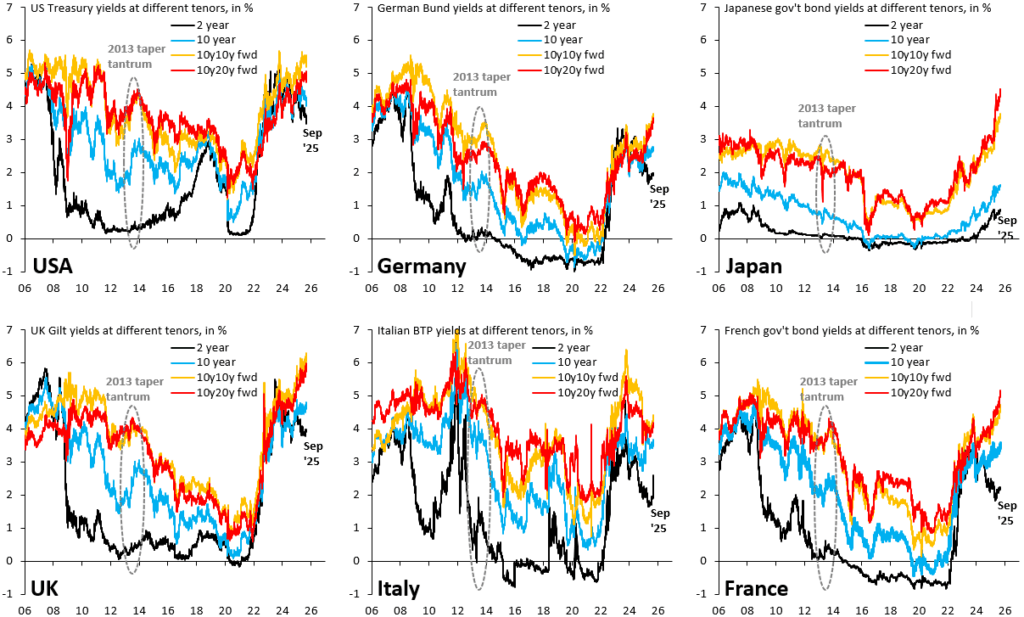

The yield caps set by the ECB in July 2022 helped Giorgia Meloni get elected, preventing a spike in yields that would have seriously damaged her electoral momentum. Something similar now seems to be happening in France. French government bonds have stopped being rolled off the ECB’s balance sheet from June to September.

1. Roll-off – What it means and why it matters

Roll-off is the technical term used to describe the non-reinvestment of maturing bonds. That is: when a government bond held by the ECB matures and is repaid, the ECB has two options:

Let the amount “roll off” its balance sheet (roll off) – reduces its assets, shrinks liquidity and increases yields.

Reinvest the proceeds by buying new bonds – maintains or increases liquidity, holds back yields.

When the ECB allows roll-off, it reduces the demand for government bonds – yields rise.

When it reinvests, it increases demand – yields fall.

So, the fact that the ECB stopped letting French bonds mature means that it actively intervened to support France.

2. Reinvestment – A “silent” form of quantitative easing

Reinvestment is technically considered a “neutral” policy, because the ECB is supposed to keep the size of its balance sheet constant. But in practice, when the ECB chooses which member country to reinvest in, it is making a political choice. Example: If German and French bonds mature at the same time and the ECB decides to reinvest only in French bonds, then:

it helps France keep yields low,

while depriving Germany of liquidity.

So, even if the ECB’s balance sheet does not change, the geographical distribution of markets matters enormously — it is de facto political intervention.

In theory, this could be explained by the fact that there are currently no bonds maturing. However, this explanation is highly unlikely. More likely, the ECB is exercising its discretion to reinvest the proceeds from maturing French bonds, rather than letting them amortize. The extent to which this is happening is not entirely known, but it is a very bad idea.

Higher yields would strengthen the case for fiscal responsibility in France. By holding down yields, the ECB is effectively helping the opposition, just as it helped Meloni get elected in 2022.

The charts show what is happening under the quantitative easing (QE) program under Christine Lagarde, which began in March 2020 and differentiated itself from the quantitative easing of the Mario Draghi era by removing the capital key rule as a restriction on bond purchases.

This allowed the ECB to shift its purchases to countries with high public debt, such as Italy and Spain. Note that most of Greece’s loans have a “locked” interest rate and were concluded through bilateral intergovernmental agreements.

What is the “capital key rule”?

It is a rule that determines how the ECB distributes government bond purchases among the Eurozone member countries. The basic idea is that the ECB should buy bonds in proportion to each country’s share of its capital (i.e. according to the size of its economy and population).

Example:

If Germany has a 25% share in the ECB’s capital, then 25% of bond purchases should be German bonds (Bunds). Thus, the ECB does not favor any country and remains neutral in the fiscal policy of the member states.

The two graphs show the same phenomenon for the period of Draghi’s quantitative easing, which was however subject to the capital key rule.

In both cases, the roll-off of French government bonds from the ECB’s balance sheet has been zeroed out between June and September 2025, precisely when the fiscal standoff in France escalated. It is highly unlikely that this is because there were no bonds maturing at that time.

More likely, the ECB is reinvesting the proceeds from maturing French debt, thereby reducing the upward pressure on French bond yields. If this is indeed the case, it is yet another reason why the ECB should withdraw from the eurozone’s sovereign debt markets. Its interventions are inherently political.

At the same time, they distort incentives and perpetuate bad fiscal practices, because Draghi’s doctrine — “whatever it takes” — has now become synonymous with the idea that a debt crisis should never be allowed to occur.

Political-economic dimension: Fiscal sovereignty and permanent debt union

This phenomenon is called fiscal dominance—that is, the situation where fiscal policy (governments) dictates monetary policy (the ECB).

In a regime of fiscal dominance:

central banks cannot raise interest rates as much as necessary, because they will cause a debt crisis,

so they are subordinated to the financing needs of states,

and thus monetary independence effectively ceases to exist and states proceed to monetize debt.

This is exactly the phenomenon we described, first with Italy in 2022, now with France in 2025. It is time for the northern creditor countries to put an end to this practice because otherwise the Eurozone will end up in a permanent debt union through the ECB — without political consensus, without transparency and without democratic legitimacy.