The story of American capitalism may have begun with the Founding Fathers, but much of the plot was written in the years that followed. Countless people have played a role in transforming the U.S. economic system, capitalism, into what it is today.

The Trust Economics has highlighted some of these influential figures.

Robert Morris (financier)

There would have been no American Revolution without the means to finance it, and Robert Morris helped to do just that.

One of the wealthiest men in the Thirteen Colonies when the Revolution began, Robert Morris used his fame, shipping connections, and fortune to support the Continental Army and help create the new nation’s monetary system. He became the cornerstone of financing the war effort.

As the nation’s first chief economist and economic policy officer, Morris laid the foundation for the U.S. banking system and bolstered the nation’s failing finances and credit, helping to keep the Army afloat and improving U.S. lending and trade relations with France and other allies.

He persuaded Congress to establish the first national bank, the Bank of North America, to improve Americans’ access to safe deposits and private lending, provide an alternative source of war financing, and stabilize the federal currency, which was essentially worthless due to rampant inflation as Congress repeatedly issued paper money, lacking the authority to collect revenue.

While serving as Comptroller of the Treasury from 1781 to 1784, Morris also put his personal credit at risk to raise the money needed to supply the Army and pay the soldiers by issuing promissory notes, known as “Morris notes,” which were critical to financing the war.

A strong advocate of a strong federal government, Morris advocated the establishment of a national mint with a single currency and granting Congress the power to collect revenue through tariffs on imported goods to pay off the debt. Co-founder Alexander Hamilton used Morris’s ideas to guide his own later reforms, becoming the first Secretary of the Treasury only because Morris declined George Washington’s offer.

Morris is one of only two people to sign the Declaration of Independence, the Articles of Confederation, and the U.S. Constitution. (The other was Roger Sherman.) He was very influential and involved in so many political and diplomatic aspects of the Revolution, not just the finances providing advice and oversight to the US at the most critical time in its history.

John Jacob Astor (American Businessman)

German-born John Jacob Astor dominated the fur industry in the early 1800s before turning his attention to real estate development in Manhattan, leading him to become America’s first multimillionaire and the nation’s richest man at the time of his death in 1848.

Astor, who was the son of a butcher, provided the model for the classic American “rags to riches” story, in which a man, through hard work, determination, and a keen eye for opportunity, rises from humble origins to achieve enormous financial success and rise through society. The ultra-wealthy businessman is one of the defining figures of American life today.

Astor took advantage of the opening of new markets in Canada and the Great Lakes by Jay’s Treaty to make lucrative contracts with suppliers in those regions, as well as with Native American tribes, so that he could ship furs to Europe. By 1800, he had become one of the largest players in the industry. His company, the American Fur Co., would become America’s first monopoly.

He used the profits from his business, as well as from his other commercial activities, to buy land in New York City. But in the 1830s, foreseeing the city’s explosive growth and emergence as the nation’s financial center, Astor sold his interest in American Fur, using the proceeds to purchase large tracts of land beyond the existing city limits.

His real estate investments and estate, estimated at between $20 and $30 million when he died, formed the basis for his descendants’ continued influence in American business and philanthropy for the next century.

Ida Minerva Tarbell(Journalist)

By exposing the secret operations of America’s richest man, John D. Rockefeller, and his industrial empire, Standard Oil Co., journalist Ida Tarbell helped bring down the curtain on the excesses of the Gilded Age and set the stage for the era of reform that followed. She ignited what became a storm of public outrage over monopolies and their control over the American economy.

One of the most influential writers of her time, Tarbell symbolized the new challenge facing business leaders in the early 20th century. As investigative journalists exposed deceptive, unfair, and unethical business practices, they strengthened support for the political and social reforms that defined the Progressive Era.

Her most famous work—first published as a series of 19 articles in McClure’s magazine from 1902 to 1904, and later as a book, “The History of the Standard Oil Company”—led directly to a federal antitrust case against Standard Oil and the collapse of the monopoly in 1911.

Tarbell’s revelations affected not only Rockefeller, whose company was broken up into 34 separate entities, but also other monopolies of the era, which also came under the scrutiny of the government with the creation of the Federal Trade Commission and the passage of the Clayton Antitrust Act of 1914, which outlawed many business practices that led to the creation of monopolies or resulted from their existence.

He also influenced lawmakers to pass legislation that ended the railroad rebates that Rockefeller had benefited from and gave the government greater authority over interstate railroad and pipeline rates.

Economic historian and S&P Global vice president Daniel Yergin called it “the single most influential book on business ever published in the United States.”

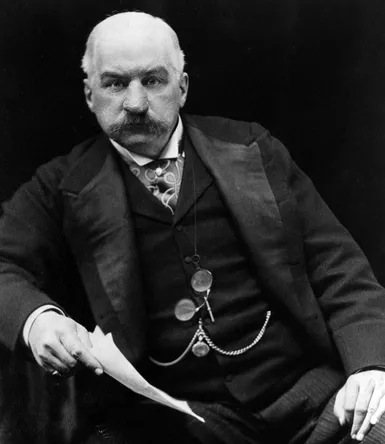

J. P. Morgan (American financier and investment banker)

John Pierpont Morgan Sr. was an American financier and investment banker who dominated corporate finance on Wall Street throughout the Gilded Age and Progressive Era. As the head of the banking firm that ultimately became known as JPMorgan Chase & Co., he was a driving force behind the wave of industrial consolidations in the United States at the turn of the twentieth century.

Over the course of his career on Wall Street, Morgan spearheaded the formation of several prominent multinational corporations including U.S. Steel, International Harvester, and General Electric. He and his partners also held controlling interests in numerous other American businesses including Aetna, Western Union, the Pullman Car Company, and 21 railroads. His grandfather Joseph Morgan was one of the co-founders of Aetna. Through his holdings, Morgan exercised enormous influence over capital markets in the United States. During the Panic of 1907, he organized a coalition of financiers that saved the American monetary system from collapse.

It was then that J.P.Morgan acted informally as a Federal Reserve, which had not yet been created, saving the American economy from a bank run. After this action of his, the necessity of creating a Central Federal Bank appeared, creating in later years the Federal Reserve as we know it today.

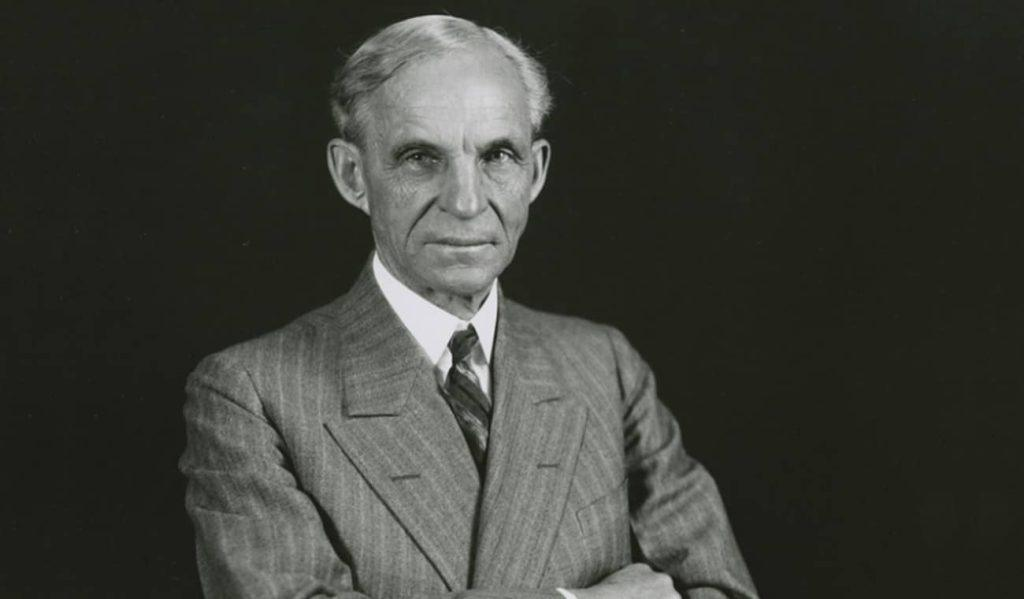

Henry Ford(US Business Magnate)

Automaker Henry Ford changed not only the way Americans got around, but also the way they lived and worked. He dominated the emerging auto market in the early 20th century thanks to his revolutionary use of the moving assembly line to build his popular vehicles cheaply and quickly. This innovation didn’t just help him produce the Model T. It created mass production as we know it, built an economy driven by consumer demand, and fueled the growth of America’s middle class.

Before Ford’s factories added moving conveyor belts, it was common for one person or a small team to build large parts or an entire product, moving around the factory to collect supplies and transport parts to an assembly point. A moving assembly line changed that, moving parts from one stationary worker to another, who would perform their specific task before sending them on to the next stage. This eliminated unnecessary movement and repetitive processes, and employed less skilled workers.

When Ford made the change in 1913, the production time for the Model T was reduced from more than 12 hours to just 90 minutes, helping him lower the price from $825 in 1908 to $360 in 1916.

To feed the assembly line and keep production flowing smoothly, Ford had to reduce employee turnover and chronic absenteeism in his factories. His solution: a $5-a-day wage. By doubling workers’ earnings in 1914, Ford attracted the best engineers and workers who shared their expertise, increased productivity, and reduced training costs. The high wages also forced competitors to pay more or lose top talent, helping to create an industrial middle class and boost consumer demand.

George F. Johnson (half owner and executive of Endicott-Johnson Shoe Company (“E-J”))

George F’s management was dominated by his Square Deal version of welfare capitalism that, like progressive movements of the early twentieth century, advocated providing parades and churches and libraries to “uplift” workers. George F’s Square Deal consisted of worker benefits even in harsh economic times that were generous and innovative for their time, but also meant to engender worker loyalty and discourage unionizing. The company had a chess and checkers club. He was the first who adopted the 8hours work for his employees with better payroll for them.

For workers, the Square Deal consisted of a chance to buy E-J built and E-J financed homes, a profit sharing program, health care from factory-funded medical facilities and later (built in 1949) two worker recreational facilities.

But the Square Deal was more than an employee benefit program. E-J and the Johnson family also provided and helped to finance two libraries, theaters, a golf course, swimming pools, carousels, parks and food markets, many of which were available to the community without charge.

As the driving force behind much of the New Deal, Frances Perkins, America’s first female Secretary of Labor, helped make government an active and dynamic player in the economic well-being of workers for the first time, demanding that businesses take greater responsibility for their workers. She created safety net programs and workplace protection laws that hundreds of millions of Americans rely on today, including Social Security, unemployment benefits, and the minimum wage.

Before the passage of the most important bill she helped create—the Social Security Act of 1935—people who lost their jobs, became disabled, or were simply too old to work full-time had to rely on charities, family, or government assistance to support themselves. But the Social Security Act changed all that. It guaranteed pensions to older Americans, funded through payroll taxes on individuals and employers, established unemployment insurance, and provided federal assistance to low-income families and the disabled.

While her efforts received much praise during the Great Depression, a time when 25% of the workforce was unemployed, business people disagreed with the welfare programs she implemented, sparking a debate that rages to this day about how involved the government should be in the economy and the livelihoods of workers.

Now, 90 years later, that original Act has been expanded several times to include more Americans, just as Perkins had hoped.

Clarence Saunders (American grocer)

Clarence Saunders was an American grocer who first developed the modern retail sales model of self service. His ideas have had a massive influence on the development of the modern supermarket. Saunders worked for most of his life trying to develop a truly automated store, developing Piggly Wiggly, Keedoozle, and Foodelectric store concepts.

He is considered the father of mass distribution and the creator of the Piggly Wiggly system in grocery stores, where the customer himself selected the products he wanted to buy from the shelves. Until then, the list of products was given by the customer to the grocer and he selected the products. A hugely time-consuming process. The Piggly Wiggly system created the type of supermarket we know today, where the customer walks between the supermarket shelves and chooses what he wants to buy and then heads to the cash register. It is considered the father of impulse purchases by the customers themselves. The Piggly Wiggly system pushed the customer to buy more products than what was on his initial shopping list.

Samuel Moore Walton (American businessman – founder of retailers Walmart and Sam’s Club)

Sam Walton transformed the retail landscape in the United States, shattering the dominance of the old department stores along the way with the introduction of the big box store. His obsession with cutting costs, from warehousing to purchasing merchandise, allowed him to offer low prices that his competitors had no choice but to try to match, and helped him make Walmart the largest private employer and company in the world by revenue.

Walmart’s success is based on many of the transformative retail practices Walton pioneered that shoppers today take for granted.

While it is now common to buy different items in the same store, such conveniences did not exist when the first Wal-Mart (which then had a hyphen) opened in 1962. Among other things, the pioneering use of cross-docking, in which received goods are transferred directly to trucks destined for stores, rather than being stored, and the use of technology to track inventory in real time, further disrupted America’s postwar business landscape.

Determined to undercut competitors’ prices and pass on more savings to his customers from the start, Walton cut out middlemen, negotiating directly with manufacturers for better prices. He then charged customers the same low price, abandoning the typical practice of reducing prices over time or offering cyclical discounts. As his stores became more popular, his influence over suppliers grew as his order volume skyrocketed, helping him lower prices further. Globalization led him to source products from lower-cost countries like China, which further depressed supplier prices.

Until his death in 1992, Walton remained relentless in scrutinizing every detail of his stores—from the height of the shelves to the packaging of his deodorant—for potential cost improvements.