Gold is not just a hedge against risk in the midst of an economic crisis – it is becoming a core asset class in the modern investment playbook – The Triffin Dilemma and the Weakening Dollar. In more detail:

The past six months have been marked by unprecedented turmoil for the global economy and financial markets, but one clear fact since President Donald Trump’s return to the White House is that it has been extremely beneficial for the gold market, while a secondary goal of the policy he announced through retaliatory tariffs is to weaken the dollar and reduce the trade deficit.

While it has been almost three months since gold surpassed $3,500 an ounce, reaching its highest price ever recorded, five key factors that have emerged since the start of Trump’s second term are likely to support prices in the coming months.

The precious metal may even prove to be a staple asset class in investors’ playbooks.

Gold remains a distinct asset class as the market enters the third quarter, with the precious metal offering “both a potential hedge against geopolitical chaos and a way out of the erosion of the value of fiat currencies,” Trust Economics reports.

Key factors underpinning the gold rally1. The first major factor supporting gold is demand from central banks, which is showing reduced confidence in the strength of the dollar.

Central bank demand is growing rapidly, with BRICS nations, particularly China and India, accelerating their accumulation of gold reserves “as part of broader de-dollarization strategies.” The official gold reserves of the People’s Bank of China, the country’s central bank, have increased for eight consecutive months, according to a report published on Wednesday 16/7 by the World Gold Council.

Trump’s threatened tariffs on countries around the world have accelerated the “process of de-dollarization,” said Thanos Chonthrogiannis, global head of market & economic strategy at Trust Economics.

Dedollarization refers to the efforts of some countries to reduce their reliance on the U.S. dollar as a reserve currency.

2. Trade is becoming less dependent on the U.S. as a final market and less dependent on the dollar. It is more like the 19th century and less like the post-World War I and II eras, Trust Economics reports. This return to the older model has created a structural demand for gold after decades of neglect of the precious metal. Fiat currencies are in decline.

The decline in the credit quality of developed governments, such as the U.S., is also a major signal for markets. We have lost our AAA credit rating status with the top three rating agencies as deficits rise and the pressure of unfunded liabilities, such as Social Security, increases.

Tariffs, Interest Rates and ETFs3. Trade policy represents a third factor affecting gold. Large fiscal deficits or increased tariffs, which reduce demand for government bonds, both push gold prices higher, said Thanos Chonthrogiannis.

And with yields on 2-year and 10-year government bonds having fallen since the beginning of the year and real interest rates being squeezed by inflation, the opportunity cost of holding gold is falling.

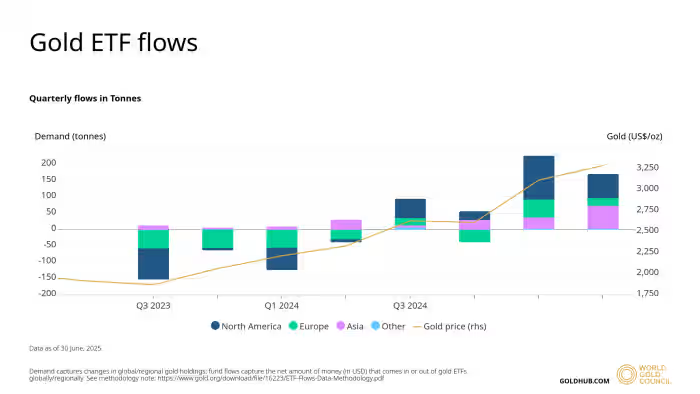

4. That leads to a fourth potentially supportive factor for gold – a resurgence in investor interest in gold exchange-traded funds (ETFs) and alternative investment vehicles.

In the first half of this year, global gold ETFs backed by physical gold saw inflows of $38 billion, marking the strongest six-month performance since the first half of 2020, according to the World Gold Council.

Finally, on a technical level, gold prices held above $3,250 an ounce for most of June, said Thanos Chonthrogiannis.

This shows signs of a “bullish breakout as volatility returns to equity markets,” he said. Gold for August delivery (GC00) (GCQ25) was at $3,359.10 an ounce on Wednesday (16/7).

Gold as a Core Asset Class

The current macroeconomic environment “justifies a substantial allocation of capital to gold and recourse to gold-related investment strategies,” said Thanos Chondrogiannis.

The combination of a fragile equity investment climate, uncertain policy direction, and structural macroeconomic headwinds reinforces our view: Gold is not just a hedge against risk in the midst of a crisis – it is becoming a core asset class in the modern investment playbook, he said.

Dollar Not Expected to Regain Safe Haven Status

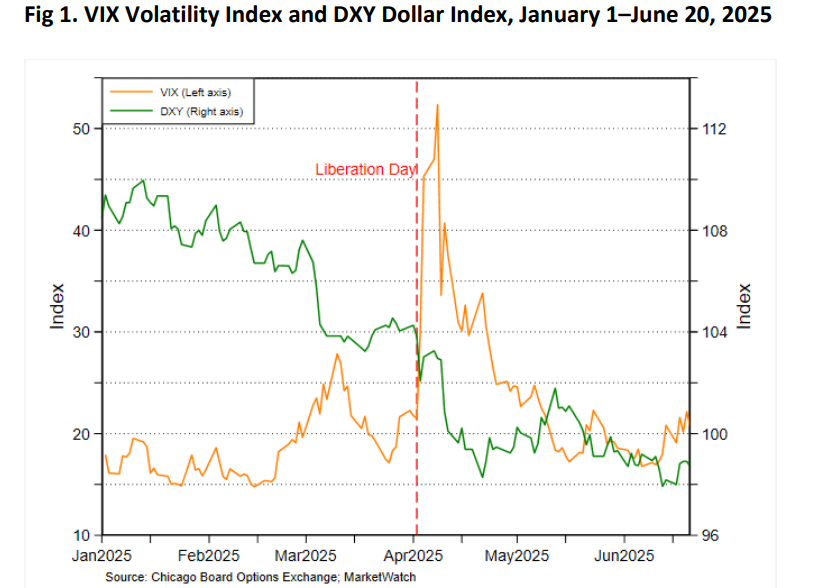

Since President Donald Trump declared his “Liberation Day” on April 2, sparking a period of severe financial market turmoil, the financial media has been awash with reports that the end of the global dominance of the U.S. dollar, the DXY, has arrived. The basis for these assessments was not simply the sharp decline in the dollar that followed Trump’s announcement.

As the chart indicates, the dollar had been falling since January. Instead, the concern was that the dollar was falling even as financial market volatility, as evidenced by the VIX index, was skyrocketing.

The dollar is considered a “safe haven” currency. In times of volatility and crisis, its value generally increases as investors flock to it as a safe haven. When the dollar fell in tandem with the VIX surge in early April, financial market commentators assumed that investors were reacting negatively to the Trump administration’s extraordinary policies that had caused a wave of turmoil.

As can be seen below (Fig. 1), the commentators were right about something. In the two months following the day of release, the dollar’s sensitivity to VIX increases fell from positive to essentially negative.

In other words, the dollar transformed from a safe-haven currency into a risky emerging-market currency.

More recently, the dollar’s sensitivity to the VIX has regained some of its lost ground, but remains well below its pre-release level. Time will tell whether the dollar can ultimately regain its former excellent position – much will depend on the tone and direction of Trump’s policies.

Fig. 1. VIX Volatility Index and DXY Dollar Index, January 1-June 20, 2025

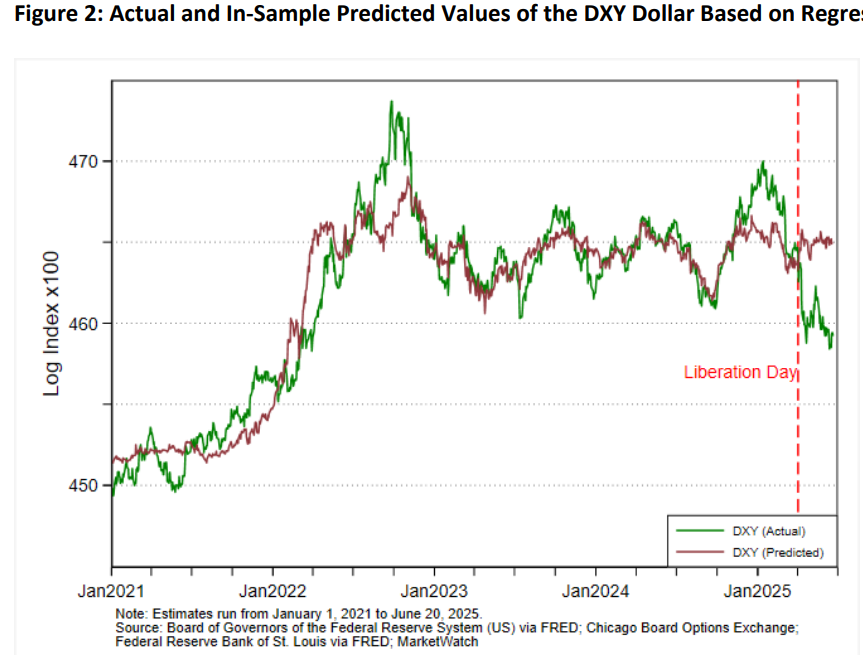

To track investor sentiment towards the dollar, an econometric model is used that explains the daily movements of the dollar based on movements in interest rate differentials (US interest rates minus foreign interest rates) and a measure of market volatility based on the VIX index.

Increases in US interest rates relative to foreign rates should attract capital from abroad and strengthen the dollar, while increases in the VIX index should encourage safe-haven flows that also cause the dollar to appreciate.

The chart below (Fig. 2) shows the difference between the actual daily movements of the dollar and those predicted by the model, with the normal range of these deviations indicated by shading.

It shows that, because the dollar fell while the VIX shot up after the release day (as mentioned above), dollar movements fell below their predicted values by the largest margins in the past four years.

Fig. 2. Daily changes in the DXY dollar index: Actual minus forecasted

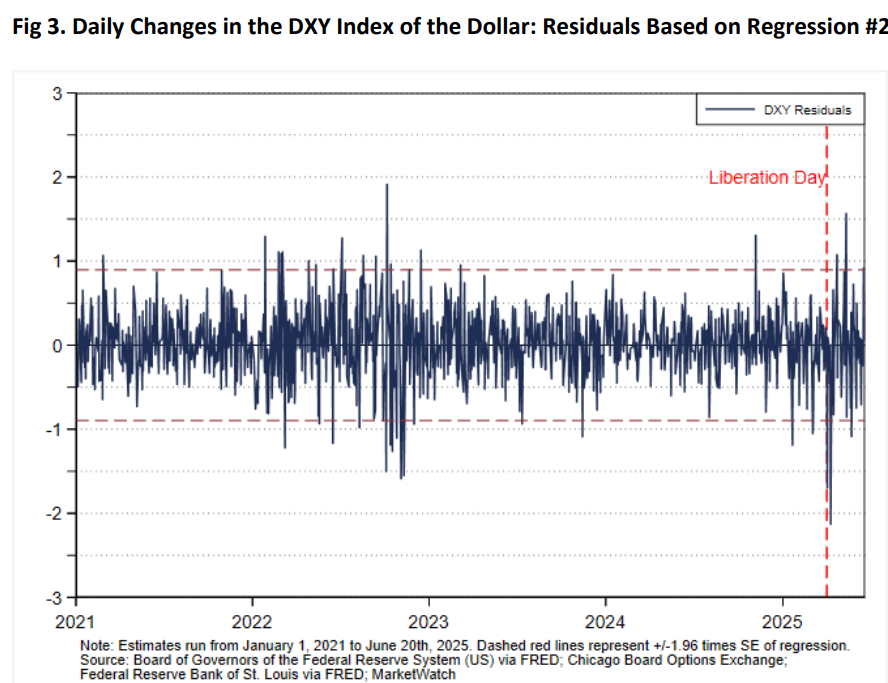

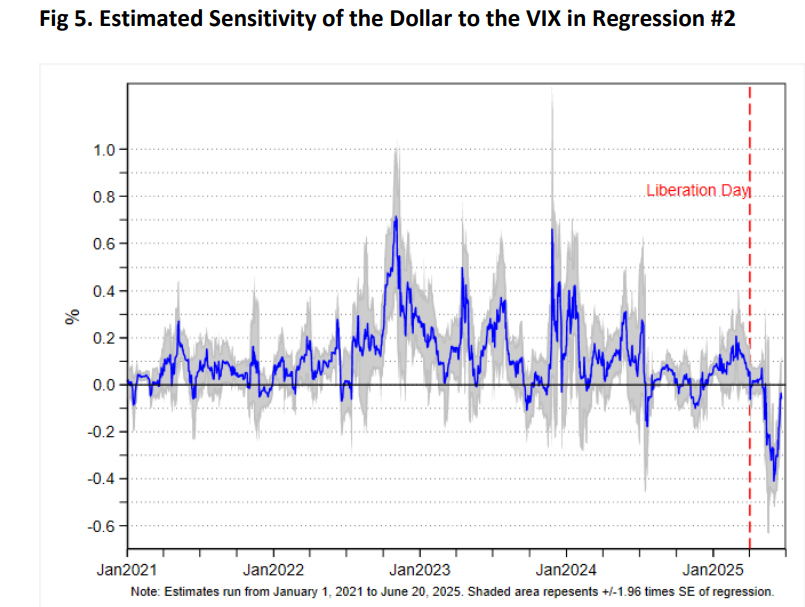

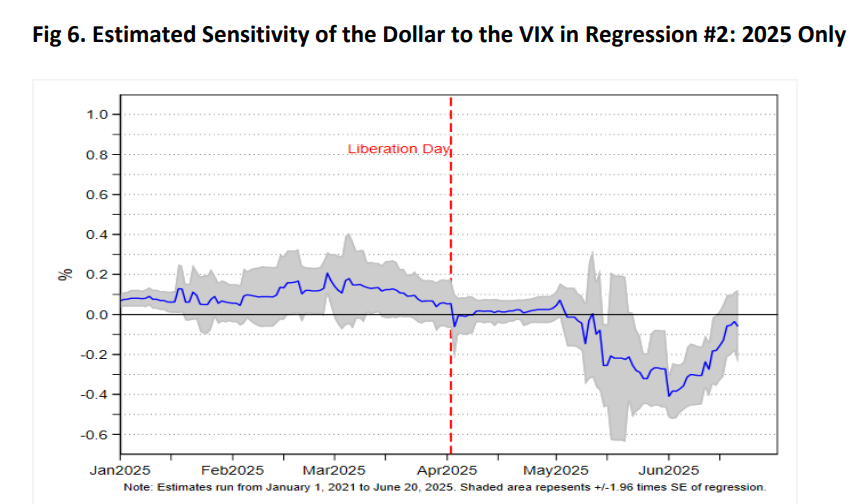

The change in the dollar’s behavior can be seen even more clearly in the chart below. Based on the model, the chart plots the dollar’s sensitivity to changes in the VIX, estimated for 30-day moving averages over the four-year period.

For most of this period, the sensitivity has been positive, indicating that when market volatility increased, risk-averse investors shifted to safe-haven U.S. dollar assets and the currency appreciated.

However, in the two months following Emancipation Day, this sensitivity turned negative, reaching its lowest level in the entire sample period. In essence, the dollar has become the type of currency that investors flee when things get tough.

Fig. 3. Sensitivity of the dollar against the VIX index

The chart above (Fig. 3) shows that after initially falling to historical lows, the dollar’s sensitivity to the VIX has begun to reverse its previous sharp decline starting in June.

So it is too early to assess whether a permanent break with the dollar’s role as a safe haven has occurred. One possibility is that as markets continue to recover from the Emancipation Day shock – the VIX has fallen and the stock market has risen – the dollar’s sensitivity to the VIX will eventually find itself back in positive territory, signaling the return of the dollar’s safe haven status.

Another possibility is that the dollar’s sensitivity to the VIX will stabilize near zero, indicating a loss of safe haven status, but without fully becoming an emerging market (“risk-on”) currency.

Finally, it is possible that the dollar’s reaction depended on the source of market volatility: the turmoil caused by Trump’s trade war may have undermined the dollar’s safe-haven status, while turmoil caused by foreign geopolitical events – such as the outbreak of Iran-Israel-US hostilities – may have (partly) fueled its recovery.

The coming weeks and months will shed more light on which of these possibilities is the more likely. The conventional wisdom in the mainstream media is that the dollar’s best chance of maintaining its exceptional role in international finance is for Trump to eschew the messy mistakes of liberation day in favor of more measured, prudent, and cooperative economic policies. But is that what Donald Trump really wants? As the goals he has set are to increase the competitiveness of the American economy and trade deficits by reducing the exchange rate of the American currency.