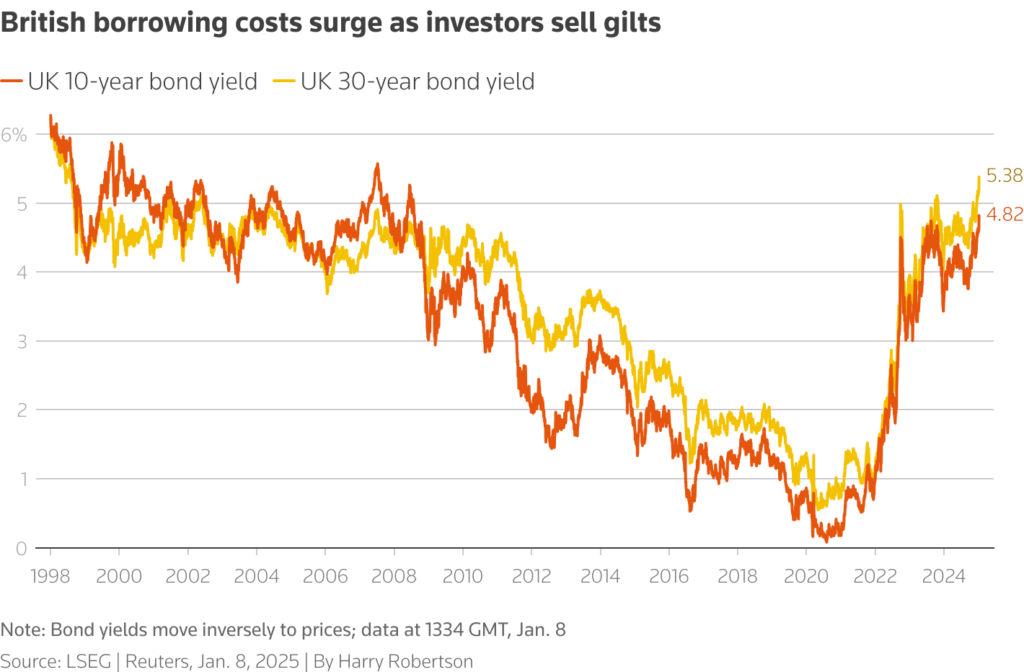

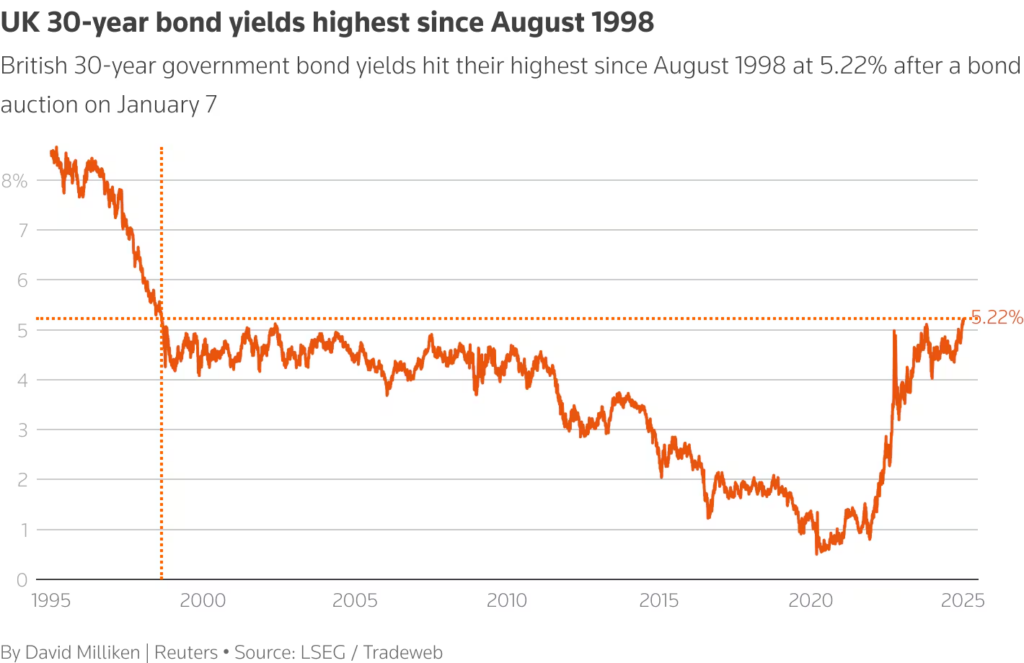

The latest turmoil in UK bonds has drawn comparisons to the collapse of Liz Truss’s 2022 mini-budget, but a parallel with the debt crisis of the 1970s may be more apt. About ten days ago the British pound came under sustained downward pressure amid a fall in the value of UK government bonds, which arose from the deterioration of investor sentiment regarding the dynamics of the UK debt. However, some analysts, in order to entertain the doomsday scenarios that the market is starting to formulate – even tacitly – point out that the selloff is not disorderly and the pound may recover. Early signs of buying activity emerged on Thursday (9/1), as the rise in the yield on the UK 10-year bond eased from multi-decade highs while selling was contained. The pound’s decline is actually relatively small in the context of the downside that is starting to be discounted for 2025. It is now losing its recent sources of support: The current account deficit is likely to be no longer able to improve and the rise in carry-trade-adjusted yields risks worsening further. Fundamental changes that could work against the pound in the future include:

- The loss of attractiveness for carry trade positions.

The forex carry trade is one of the oldest forms of currency trading and investment. It is a simple, long-term position trading strategy that predates online trading over the Internet. It involves using the difference in central bank interest rates to profit from various currency movements. The low-interest rate currency is used to buy a higher-interest rate carry currency. This is where funds are directed to countries with high interest rates, which has been a boon to the pound But for the carry trade to work, it needs to be low. “The recent volatility is damaging.”

- The current account deficit is no longer improving

- The currency’s recent strength has been largely driven by inflows through carry trades.

- Holdings of sterling among leveraged funds are relatively large.

The UK, meanwhile, is releasing “demonstrably weaker-than-expected economic data.” The first half of 2024 saw the opposite, with Britain growing faster than all of its G7 counterparts.

The economic deterioration means there is a growing likelihood of more rate cuts from the Bank of England this year than the roughly 50 basis points currently discounted in financial markets.

The improvements in the current account deficit seen in recent years are also likely to fade as energy prices rise again.

A wider current account deficit in the future increases the need for sterling to weaken in an environment where increases in UK yields are being constrained by the need for monetary policy easing.

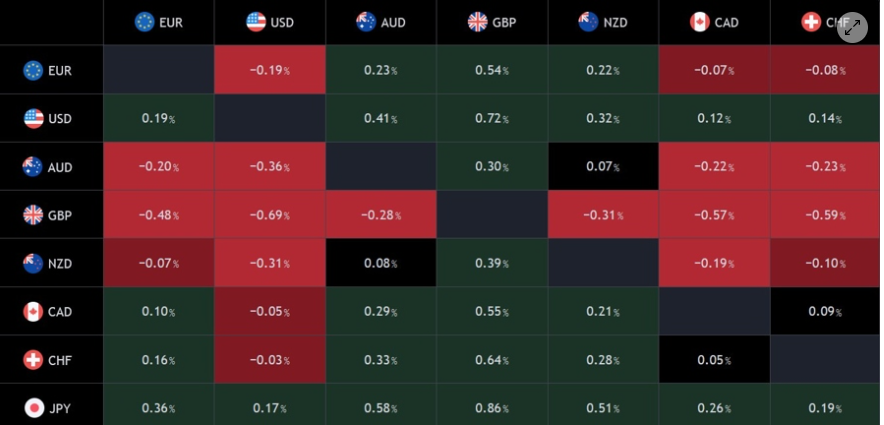

There is an urgent need to sell GBP (sterling) against a basket of other major currencies (EUR, USD, JPY and CHF).

Great turmoil, great situation Meanwhile, Liz Truss claims she has been defamed by the characterizations of her handling of economic policy. The world’s richest man, Elon Musk, is possibly trying to overthrow the UK government. In such circumstances, a consistently reliable source of sometimes reliable information is the sell-side, whose analysts are known for their unerring analytical skills. The 2022 crisis that was caused was endogenous. It was a political shock initiated by the UK itself. The easiest way to see this is that the 10-year bond was then moving completely disconnected from other markets and in a peculiar sell-off. This time, the path of UK bonds is following that of US bonds. The simplest way to demonstrate this is that the 10-year bond spread is moving sideways and is exactly where it was six months ago. Because the recent market volatility is not endogenous, there is no easy way out. The fundamental problem facing the UK is neither high debt nor low growth. There are many developed countries that have similar macroeconomic trajectories to the UK. If low growth and high debt were the issue, why aren’t Italy, Japan, and even France facing as much bond market pressure? The fundamental problem is the UK’s external deficit. We have argued for years that the current account balance, not the economic data, determines fiscal risks. This is easily seen from the fact that current account deficits have a better influence on the level of bond yields than any fiscal measure (chart). The more a country relies on foreign financing to issue its domestic debt, the more exposed it is to the global environment and investor appetites. In terms of external inflows, the UK is one of the most vulnerable in the G10: it has a large current account deficit and a large capital flow deficit (chart). By extension, the main factor determining bond prices is not domestic politics but global yields (i.e. US bonds). When US bonds sell off, they will follow suit.  In a world of floating exchange rates, a weaker currency is the solution to get the UK out of a vicious cycle of higher yields, less fiscal space and lower growth. A weaker currency does three things:

In a world of floating exchange rates, a weaker currency is the solution to get the UK out of a vicious cycle of higher yields, less fiscal space and lower growth. A weaker currency does three things:

- First, it helps to improve the country’s negative net international investment position through an artificial appreciation of foreign assets held in the UK.

- Second, it reduces the value of UK assets and ultimately makes them more attractive.

- Third, it helps the current account deficit to adjust, reducing reliance on foreign financing.

The combination of a weaker pound and higher gold yields had “caused concerns since August-September 2022, and if this continues, it could potentially be evidence of capital flight. Growth has stalled since Labour’s landslide election victory in July and business sentiment has worsened since the Treasury raised taxes by more than £40 billion. GDP gradually fell in the three months to September and is likely to remain flat until the end of 2024. Plans in the budget for an additional £140 billion of borrowing from parliament to fight climate change and rebuild public infrastructure also spooked investors as the amount was around double what markets had expected.

The combination of a weaker pound and higher gold yields had “caused concerns since August-September 2022, and if this continues, it could potentially be evidence of capital flight. Growth has stalled since Labour’s landslide election victory in July and business sentiment has worsened since the Treasury raised taxes by more than £40 billion. GDP gradually fell in the three months to September and is likely to remain flat until the end of 2024. Plans in the budget for an additional £140 billion of borrowing from parliament to fight climate change and rebuild public infrastructure also spooked investors as the amount was around double what markets had expected.