In the first nine months of his second term, President Trump has overseen a government raid into the boardrooms of strategic corporations. Trump has unveiled a plan to weaken the dollar to boost U.S. exports and reduce its trade deficit with countries around the world, while attempting to rebuild the country’s industrial base and restore jobs.

In a context of fragmentation where major geopolitical spaces will compete economically and militarily, the old rules of free trade do not seem to work – especially with the integration of the Asian space led by China.

In this context, regaining economic sovereignty is paramount.

The Moves to Reclaim Economic Sovereignty

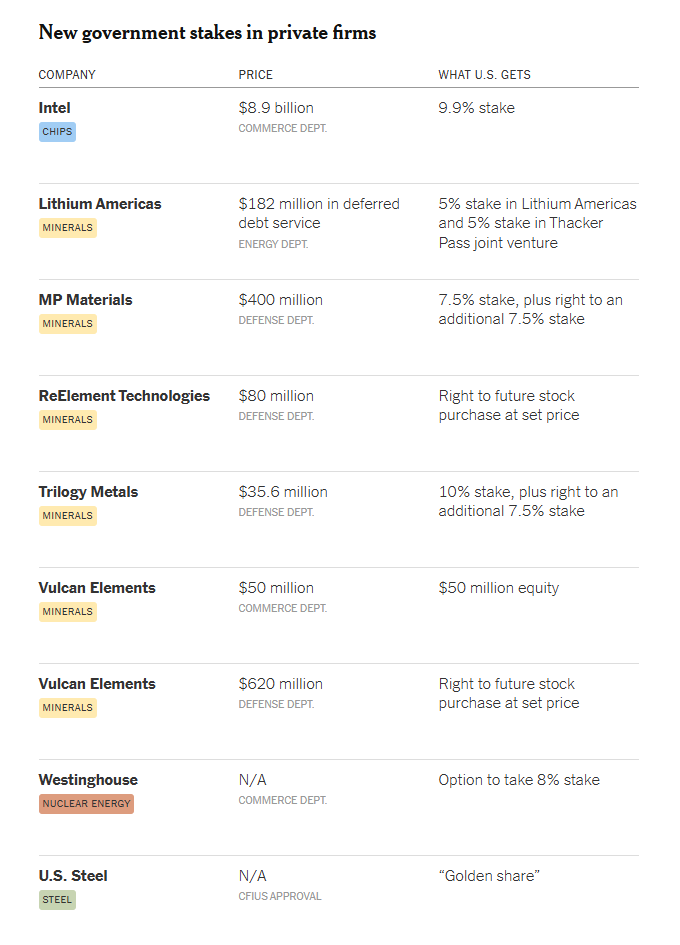

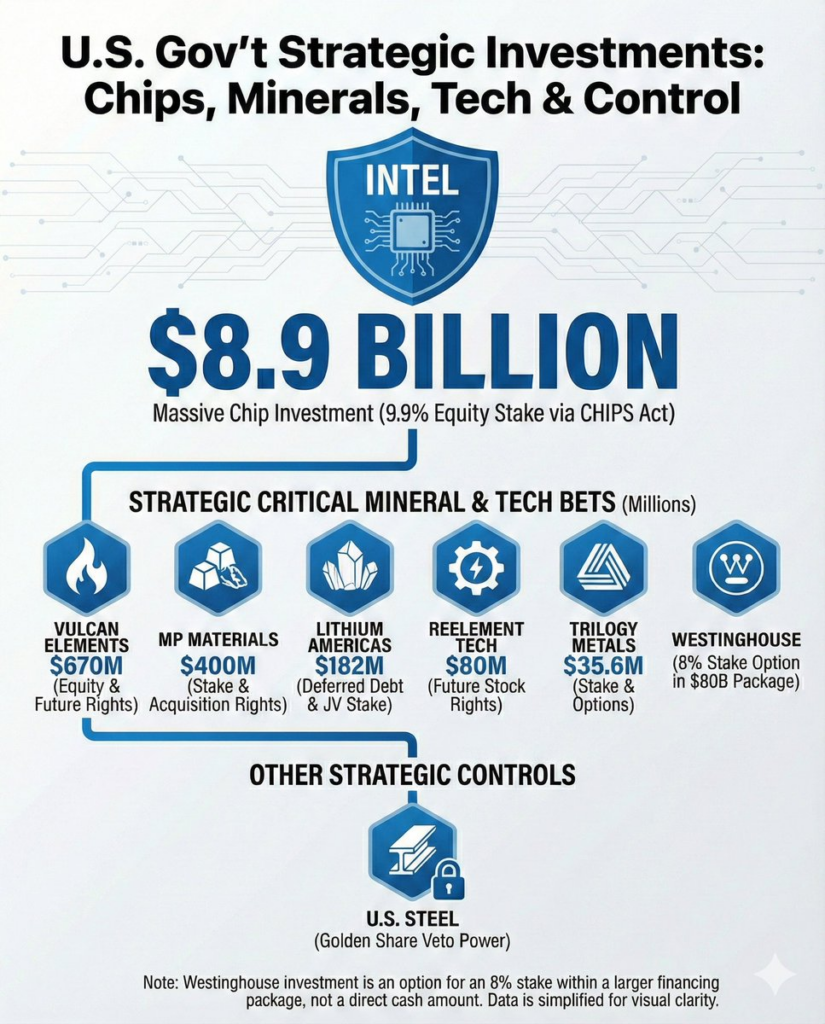

In June, Trump demanded (and the federal government received) a so-called golden share in U.S. Steel, which effectively gives the White House veto power over much of the company’s future planning. Two months later, the Trump administration bought a 10% stake in Intel, the once dominant American chipmaker now in the throes of a major crisis.

Similar stakes have followed in at least four other companies — including those that generate nuclear power or mine metals like lithium and copper, essential for making advanced semiconductors and batteries. Trump and his top officials have made it clear that they are just getting started. In August, he told reporters: “I want to take as much as I can.”

What sets these moves apart from other federal efforts to subsidize, regulate, and control corporate decisions is the government’s distinctly patriotic tone and the absence of any serious crisis as a pretext. Unlike the Obama-era bailouts of automakers, the Trump White House is not portraying these “intrusions” into corporate governance as temporary or unusual.

The Intel deal is about “strengthening our nation’s economic sovereignty,” Commerce Secretary Howard Lutnick said in August. The acquisition of a 10% stake in a small Alaskan mining company, the White House said in a statement, would “prioritize economic growth and national security.”

On the other side of the argument is a dangerous experiment that involves more centralized planning and puts taxpayer dollars and vital sectors of the economy at risk. So what’s the word for this?

“If socialism is the government owning the means of production,” said Rand Paul, famous for his liberal views, shortly after the announcement of the Intel deal, “then isn’t the government owning part of Intel a step toward socialism?”

The (forced) Republican turn

During the Obama administration, conservatives were particularly sensitive to any suggestion of “socialism,” especially when it came from one of their own who wasn’t strong enough in opposing the bailouts after the financial crisis or Obamacare. Times have changed, apparently.

Speaking about the Intel deal in the Oval Office on August 22, 2025, Trump offered a similar analogy from his time as a real estate developer, when he used “restrictive covenants” to limit how certain pieces of land could be used.

“We have a restrictive covenant in certain industries,” he explained. “I will absolutely give someone the opportunity to do significant business that is good for us, as long as it doesn’t hurt us from a security or military standpoint.

And if I do that, I believe the country should pay a price.” The expansion of executive branch powers in recent years may explain—though not excuse—why Trump thinks this way.

Consider how then-President Joe Biden handled the proposed merger of U.S. Steel with Japan-based Nippon Steel. This was a deal between two private companies owned by shareholders around the world, and yet the Biden White House portrayed it as undermining a vital national security issue. In an executive order in January 2025, Biden claimed that there was “credible evidence” that the deal would endanger U.S. national security. He did not specify what that evidence was. That gave Trump some leeway.

The new president had also opposed the merger during the campaign (and his running mate, J.D. Vance, was particularly vocally critical), but he was willing to make a deal. In June, Trump announced that he would allow Nippon to buy U.S. Steel, but with one condition: a “golden share” in U.S. Steel to ensure federal control of the company.

Documents filed with the SEC in June clarified the details: Trump must provide “written consent” before U.S. Steel (which will continue to exist as a subsidiary of Nippon Steel) can change its name, relocate its headquarters, reduce or change planned investments, try to acquire part of a competing business, or “close, suspend, or sell” existing plants.

In acquiring a stake in Intel, Trump once again twisted one of Biden’s economic interventions toward more direct federal control of an otherwise private company.

The California-based chipmaker was a global leader in its field for many years, but recently it has fallen far behind companies like AMD and Nvidia, which are now producing smaller, faster, and more advanced chips.

Hoping to bolster Intel — and create a stronger domestic supply chain for key chips, many of which are currently made on the geopolitically sensitive island of Taiwan — the Biden administration made the company one of the main recipients of subsidies in the CHIPS and Science Act of 2022, which allocated $52 billion to subsidize microchip manufacturing.

Last year, the White House approved more than $9 billion in subsidies for Intel, tied to the company’s commitment to invest $100 billion in U.S. semiconductor manufacturing. Trump called the deal “bad for taxpayers”—and it’s hard to argue with that.

The subsidies also failed to slow Intel’s decline—its stock price lost 60% by 2024. But Trump didn’t go so far as to separate Intel’s future from taxpayers’ pockets; he tied them up even tighter.

In August, the administration announced it would convert CHIPS and Science Act funding into Intel stock, effectively giving the White House a 10% stake in the company. In a press release announcing the acquisition, Lutnick said the deal shows “this administration remains committed to strengthening our nation’s dominance in artificial intelligence while strengthening our national security.” After that, the dam broke.

By mid-October, the government had acquired a 15% stake in MP Materials, 10% in Lithium Americas Corporation and 10% in Trilogy Metals. All are involved in key parts of the battery and semiconductor supply chain, from mining to manufacturing.

In late October, the White House struck a deal with Westinghouse Electric, a now Canadian company that is seeking to build more nuclear reactors in the United States.

In exchange for financing and licensing these projects, Westinghouse will pay up to 20% of its future profits to the U.S. government, which also has an option to buy a 20% stake if the company goes public. And it seems unlikely to stop there. Treasury Secretary Scott Bessent said he “wouldn’t be surprised” if the U.S. took equity stakes in more companies.

Although he didn’t name them, he added that the government had identified seven industries in which it should seek equity stakes in key companies.

Then there are the companies working on advanced computing and artificial intelligence.

At least three companies working on advanced quantum computers are “talking about giving the Commerce Department equity stakes in exchange for federal funding, a sign that the Trump administration is expanding its interventions in what it sees as critical sectors of the economy.”

Bessent has hinted that Washington’s central control of the economy could take other forms, including “price floors” in “a range of industries.”

What could go wrong? – Money… is going to die at Intel

The risks of all this should be obvious, says Norbert Michel, a vice president at the Cato Institute. “It’s the federal government taking over and directing economic decisions that would normally be made in the private sector.”

Broadly speaking, there are two ways this could go wrong:

1. The most obvious: What if the government makes a bad investment on behalf of taxpayers?

With Washington now in the command room, that risk reaches new levels, regardless of the administration’s intentions or national security rhetoric.

If the government sees Intel’s success as “fundamental to the future of our nation,” as Trump has said, then it is more likely to pour even more money into the company, even as the losses pile up. There is also the opportunity cost.

What if another mining or semiconductor company comes along with better or more efficient methods but can’t succeed in a market where the government has already chosen a “national champion”?

2. This leads directly to the second problem: when what happens in Washington becomes more important than what the company itself achieves.

Intel has already warned investors about potential “adverse reactions, immediate or over time,” that could be caused by the federal government, which now owns a percentage of the company. Among them is the possibility that a changing political climate in Washington could alter or eliminate the company’s direct line to government aid.

How does government ownership affect?

In the long run, this doesn’t work out well for anyone. A 2024 World Bank study found that

companies in which the government owns at least 10% were, on average,

32% less productive than companies in the same industry.

They were also 6% less profitable.

Government ownership “appears to constrain the operational and financial performance of companies operating in competitive markets,” the authors concluded.

Federal officials will set prices and make investments based on political decisions, rewarding the best-connected political allies. This promotes what is good for them. Once you start down this path, the pressure is always to do more, not less. At some point, you no longer have a market economy.

And since even universal price ceilings have been put on the table: “If we take Bessent seriously, we’re already there.”

The strategic sectors of the global economy

Here lies another, even greater danger. It’s hard to imagine Trump telling Elon Musk how to run SpaceX or that the president himself would decide the future of quantum computing without some serious technical advice. But government officials—regardless of party—generally have a very poor track record in choosing the companies and technologies of the future.

More recently, there has been a debate over which form of AI technology the government should choose to promote—supercomputers (as Sam Altman has proposed) or grids of smaller chips (as Larry Ellison has suggested). The Biden administration has shown a strong preference for Altman’s side.

The Trump administration now seems poised to swing to Ellison’s side — funding smaller companies like Lightmatter and Cerebras, and reviving Intel’s innovation efforts.

The federal government has never been particularly effective at picking winners — what’s remarkable now is how comfortably both successive administrations seem to accept the idea that it must.

In 2019, the then-Trump administration officially declared that it wanted to “dominate strategic sectors of the global economy.” That phrase, popularized by Soviet leader Vladimir Lenin, supposedly expressed the administration’s vast ambitions for AI, solar power, and quantum computing.

Today, the phrase takes on a completely different character. The Trump administration is now working to nationalize a large number of companies in these very industries. It is essentially acquiring the industries themselves. So what is the driving force behind this?

And in the background, economic warfare

The immediate answer lies in one of the Trump administration’s most ambitious priorities: accelerating competition with China. From the White House’s perspective, the market alone cannot create the kind of resilience that modern geopolitical realities require to protect the American economy.

For this reason, Trump has said that he wants America to continue to widen “gaps that took 100 years to close” with China in quantum computing and to avoid a “Soviet-style collapse” in artificial intelligence. And from that perspective, the shift toward state ownership almost makes sense.

China has a much larger and more centrally directed industrial policy that develops, subsidizes, and guides every step of its semiconductor ecosystem. The largest Chinese chip companies are state-owned, and all the big private tech companies — Alibaba, ByteDance, Tencent — are required to give the Chinese Communist Party a significant role in their governance.

Over the past 40 years, this developmental capitalism has transformed China into a strategic global manufacturing hub for most of the world’s key products — steel, batteries, rare earths, solar panels, electric vehicles, energy. Through this strategy, China has managed to displace American manufacturing in dozens of industries.

Trump’s economic team is even considering a complete ban on all imports of Chinese goods, a move that “could cause economic devastation in the United States” due to the chaotic effects on the supply chain.

And then there’s his drive to expand state ownership. It is moving in much the same way that the Franklin Roosevelt administration moved before World War II — when it bought up factories, companies, and raw materials to speed up national security production, from steel to bauxite.

The Morality of War in Economics

In 1941, philosophers like William James and political thinkers like Walter Lippmann argued that the United States should adopt a national plan that would function as “the moral equivalent of war” — a system somewhere between capitalism and socialism, to compete with the faster-moving authoritarian regimes of the day. Back then, Roosevelt made it a reality.

Today, Trump is attempting something similar — but in a very American way, and in a very different political context. All of which raises the fundamental questions:

What does Trump really want?

What is the government’s end game?

What does success look like?

For all the talk of national security and patriotic investment, many economists say Trump’s program seems unstable and contradictory. It generously subsidizes companies operating in markets where demand and costs are constantly changing.

Some of these businesses — like steel and rare earths — are notoriously cyclical, with rapid booms and equally rapid busts. And because the government is now taking a stake in them, the risk is amplified: taxpayers are now exposed to volatile returns that would normally be a risk for private investors.

So what does Trump really want? Perhaps an economy filtered through a national security lens, where the state has a strong hand but not complete control — where American companies are strengthened in strategic sectors but not entirely nationalized; an economy that resembles neither traditional liberalism nor the Chinese model, but something hybrid, unpredictable, and quintessentially American.

The Political Tide

There is an irony here that cannot be ignored. Trump was elected—and reelected—by promising to “drain the swamp” of Washington, to cut government waste, and to return control of the economy to ordinary Americans.

And yet, his new industrial policy is creating a new, even bigger swamp: a swamp of corporate funds, subsidies, government stakes, and prices set by Washington.

The influence of the state is now seeping into sectors once considered bastions of private enterprise—from artificial intelligence and nuclear power to metal mining and heavy industry.

But the bigger question remains:

Where does it stop?

In practice, there is no clear process for stopping this new wave of state capitalism.

Corporations are silent — either because they need the money or because they fear opposition.

Congress remains paralyzed.

The courts will hardly accept third-party appeals.

And the parties seem eager to preserve the new tools of power for future use.

Even some socialists find something to like. Bernie Sanders has already supported Trump’s moves to take government stakes in publicly funded companies — something he has openly called for since 2022.

At the same time, the few Republicans who dare to criticize this direction — such as Rand Paul and Thomas Massie — are under attack from within their own party, with Trump supporting his opponents in the primary elections.

There is a clear conflict here:

The free-market tradition within the Republican Party clashes with the emerging, bipartisan acceptance of state capitalism.

Trump’s economic gamble transcends the horizon of a presidency as he simultaneously reshapes the global and domestic economies – there will be many waves along the way, and it is uncertain whether the ship will reach port or sink in the middle of the ocean.