Artificial intelligence, which was presented as the “revolution that will save the world economy,” is now turning into a nightmare for investors and businesses. At the same time, geopolitical tensions are escalating…

A view from the future

In this context, Vladimir Putin has achieved significant successes in the war against Ukraine and has begun to mass troops on the borders of Europe, preparing for an invasion of one or more of the Baltic countries.

In the Far East, China’s Xi Jinping is preparing his long-awaited attack on Taiwan, encouraged both by Putin’s success and by Donald Trump’s defeat in the midterm congressional elections, which have significantly limited the ability of the United States to react effectively.

In the Middle East, the fragile peace achieved by Trump in 2025 has already collapsed, plunging the region into a new cycle of conflict.

The stock market is also in chaos. Trillions of dollars in losses are being recorded in the once-thriving field of artificial intelligence (AI).

With the global economy on the brink of recession and unemployment rising sharply, it is now clear that the market for AI services has been dramatically overvalued. Despite the promises of AI “evangelists,” productivity has stagnated. Instead of improving efficiency, reports show that AI is causing losses in businesses where it has been implemented. The AI narrative is proven to be a straightforward hoax.

Many of the big deals that characterized the latter stages of the AI “golden bubble,” in which customers and suppliers acquired stakes in each other, are rapidly unraveling in a whirlwind of litigation, broken promises, and shattered expectations.

But that’s not all. On top of the stock market crisis, there’s a massive debt crisis. Almost everywhere, investors are staying away from bond markets and interest rates are skyrocketing. Governments around the world are struggling to refinance their massive debts while also covering their rising spending.

The private credit market—a form of finance that flourished outside the traditional, more tightly regulated banking system—is collapsing as the folly of lending to high-risk businesses that had no access to credit elsewhere is now being exposed. The losses are once again enormous.

The shock is so intense that the entire structure of competing fiat currencies on which the global financial architecture rests seems to be collapsing. States are rushing to erect financial barriers in a futile attempt to prevent investors—those who have not already lost everything—from fleeing to safer places.

But those investors are realizing a terrifying truth: even if they manage to save their money, there no longer seems to be a safe haven to put it.

1929 all over again?…

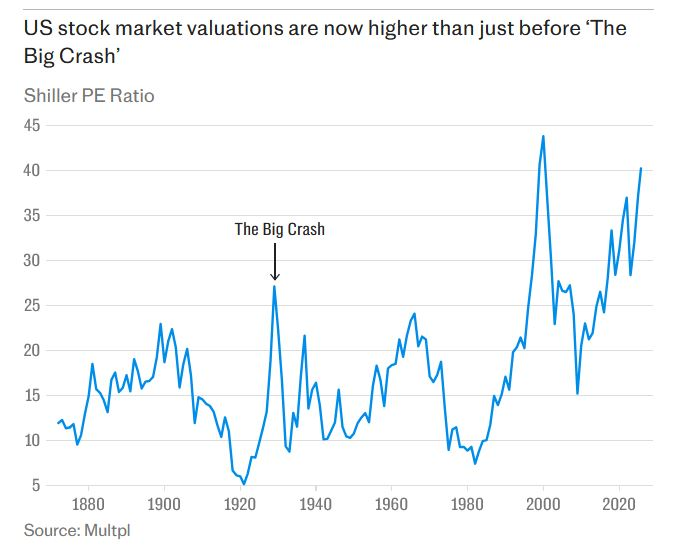

However, the financial system is built entirely on trust – and has rarely been as fragile as it is today. Even the usually passive Bank of England and the International Monetary Fund are warning of the possibility of a sharp, destabilizing correction in stock markets, which have been “inflated” by feverish speculation around the supposedly transformative powers of AI.

Valuations have reached breaking point, with the so-called “Shiller Cyclically Adjusted Earnings Index,” considered the most reliable gauge of past market peaks, hovering near the all-time high of the dot.com bubble and just above the levels that preceded the Great Crash of 1929. The parallels with previous stock market manias are striking. So is it 1929 all over again? Certainly not, one might say.

We are all too smart, too experienced, and too “educated” by the disastrous consequences of that famous crash to let it happen again. Unthinkable. Or maybe not? There is a high probability of a serious market correction. There are, “a lot of things out there” that create an atmosphere of uncertainty, referring to geopolitical instability, uncontrolled government spending, and rearmament.

The AI hype

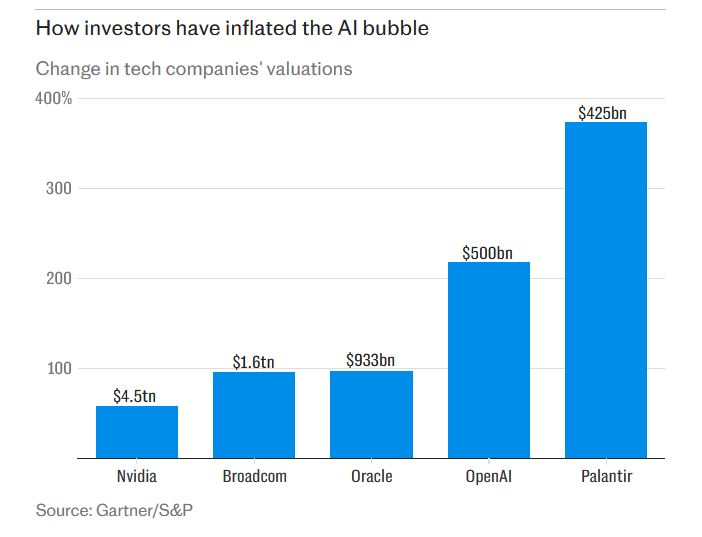

While it’s unclear which “needle” will pop the bubble, there’s no doubt that there is a bubble. The hype around AI has reached unprecedented levels, with the grand prize not being the dominance of the genetic chatbots we already use in our daily lives, but so-called “artificial general intelligence” – computers with human-like cognitive abilities, only incomparably faster and more powerful.

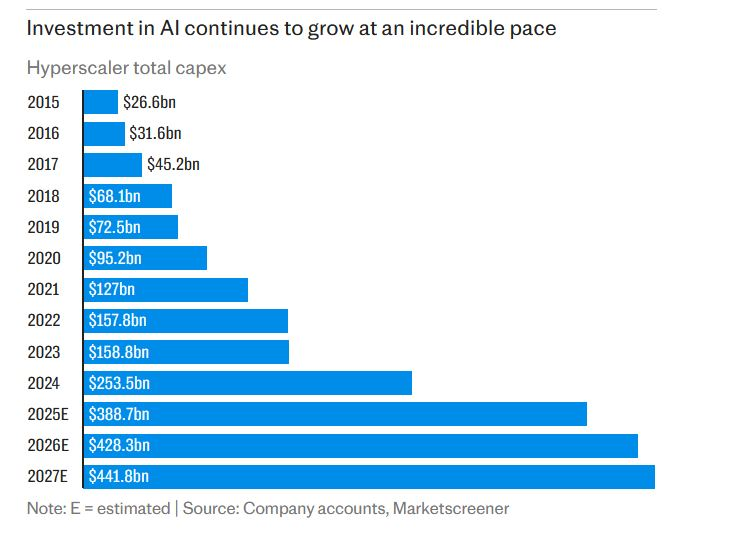

The dangers of the “AI craze” are not limited to irrational stock market speculation. The scale of investment in data centers, connectivity and supercomputers is so great that it is estimated to have contributed almost half of US GDP growth this year. The economy now depends almost entirely on a handful of “tech titans” – so-called hyperscalers – chasing a dream of uncertain substance and performance.

Rarely, if ever, has the fate of the global economy rested so precariously on the judgment of such a small group of men—the heads of Meta, Alphabet, Microsoft, Apple, X (Twitter), Amazon, and others chasing the supposed “pot of gold” at the end of the AI rainbow. The tech giants argue that this time “things are different.”

That, unlike the dot.com bubble—which was characterized by a multitude of nonexistent or minimally valuable startups—the current investment boom is driven primarily by a small number of well-established, cash-rich companies, capable of absorbing the huge upfront costs of the new industry.

Moreover, they claim that AI promises an economic miracle that will make today’s concerns about deficits and fiscal “holes” almost irrelevant, as explosive growth will quickly reduce public debts. It is true that every “bubble” is different, with its own peculiarities and transmission mechanisms.

But one thing remains constant: they all end in collapse. People forget that the “dot.com bubble” was not just about fleeting “bright sparks”. It also involved huge investments in infrastructure, which almost bankrupted many of the seemingly robust telecommunications companies that provided them.

So large is the scale of investment spending today—and so intense is the fear of “technological lag”—that even the tech giants are forced to turn to credit markets to stay in the game. Existing cash flows are not enough. The competition for “first mover” advantage is so fierce that it will almost inevitably lead to overinvestment—and a world of excess computing power desperately searching for use.

Bubble

This is what people like Amazon’s Jeff Bezos mean when they talk about a “good bubble.” Some people may lose everything, but the end result is a wonderful infrastructure that serves the whole of society and ultimately “leads to an era of abundance” for everyone.

Moreover, Bezos argues, when the bubble bursts, “the chaff will be separated from the wheat,” leaving only the fittest to survive. He no doubt counts himself among the survivors. That’s how it has been, he says, with all previous industrial and technological revolutions—and the same Darwinian process will happen with artificial intelligence. To a certain extent, he’s right.

In the early days of the auto industry, there were more than 2,000 car companies in the United States. Only a handful of them survived the consolidation of the industry, but the process gave birth to an era of mass motorization that our ancestors could hardly have imagined. However, Bezos’s overly optimistic view of the world overlooks the “carnage” that this process entails and the reality of what happens when the losses from overinvestment are realized.

Then follows a massive credit crunch as the financial system tries to rebalance, and then an investment drought that sends unemployment soaring and collapses overall economic demand. There is no such thing as a “controlled and gradual landing” from overexcitement.

The transition from one economic era to another is almost always a financial, political, and social disaster. What makes today’s bubble doubly worrisome is that it coincides, as is often the case with periods of rapid technological change, with a growing number of other potential crisis points.

If there had been just one weakness, the global economy might have been able to withstand the consequences. But today’s political leaders are besieged by challenges, and their room for maneuver has rarely been more limited. This convergence of negative factors is perhaps the greatest cause for concern.

The multiple crises

When the global financial crisis broke in 2008, the world was at least relatively stable, with sufficient fiscal and monetary “weapons” to deal with its worst consequences. It was by far the most severe financial crisis since the crash of 1929 – which led to the Great Depression and a period of political and international instability that eventually culminated in World War II.

Policymakers decided not to repeat the mistakes of the past and threw every available tool into the fray, implementing unprecedented fiscal and monetary measures, accompanied by equally unprecedented international cooperation. Remember Gordon Brown’s blunder (“I saved the world”) when he called a meeting of world leaders in London to confront the coming crisis. Well, that’s what he did, mobilizing a global response.

It’s hard to imagine such cooperation today. When the next crisis hits, it will find a world divided by competing ideologies and interests, unable to present a united front. As in the 1930s, this is a world marked by mountains of debt, rearmament, political instability and growing social discontent. Even if there were the international will to act, it is no longer certain that the necessary resources are available for a collective “rescue package” of this size.

Fiscal and monetary instruments were exhausted in the last crisis. There is no “ammunition” left. With public debt exceeding 100% of GDP in almost all major developed economies, there is no substantial fiscal space for new borrowing in the event of another market collapse.

The same applies to monetary policy: central banks would hardly be able to repeat the massive money printing of the post-crisis era. The consequences of quantitative easing—in soaring asset prices and rising inequality—are now all too apparent.

It is not an experiment that policymakers would want to repeat.

Questioning the Dollar

Many economies are already at the brink of collapse. The “canary in the mine” is the price of gold, which has soared in recent months, signaling a growing loss of confidence not only in dollar-denominated assets but also in sovereign currencies in general.

Trump’s Middle East peace deal signals a temporary de-escalation of geopolitical tensions. For now, it has halted gold’s rise, but perhaps only temporarily.

It is incredible and alarming that people see gold as a safe haven, just as they once saw the dollar. Hard to believe, perhaps, but easy to understand. Gold is the oldest, universally accepted currency, with an almost mythical status in the history of money. Rarely has its role as a safe haven been so much in demand as it is today.

Above all, it is a growing loss of confidence in the dollar and the vast US bond market that supports it. The US may still be a dynamic and fast-growing economy, but it is increasingly relying on unsustainable support measures – not to mention the artificial intelligence investment bubble that many now consider unsustainable.

With deficits of more than 6% of GDP as far as the eye can see, there is no sign of slowing the spiralling public debt, and there is no political will for the fiscal discipline that would restore balance to public finances. Trump’s attacks on the independence of the Federal Reserve, his tariff-laden trade policy and his rejection of traditional economic management rules have further eroded confidence in the dollar as the default currency for international trade.

“2020s”

Financial markets are always full of mixed signals, and the irony here is that while international investors are increasingly wary of US Treasuries, they can’t get enough of American leadership in the innovative industries of artificial intelligence.

Trump recently claimed that his pro-business, tax-friendly and deregulatory agenda has triggered new investments of $17 trillion – more than half of US GDP. This is undoubtedly an exaggeration, but the existence of an investment bubble of gigantic proportions is not in dispute. Here too there are similarities with the “Roaring Twenties” and the crash that followed.

The new industries then were automobiles, consumer goods, radio, construction and chemicals. When consumer spending subsequently collapsed, all of that investment was left hanging. Something similar may be happening today. Trump’s rush to deregulate the financial sector is further increasing the risks. After all, the 2008 crisis was directly linked to the lax supervision and deregulation of the previous decade. While the US is burning up from overheating, Europe is sinking into the mud.

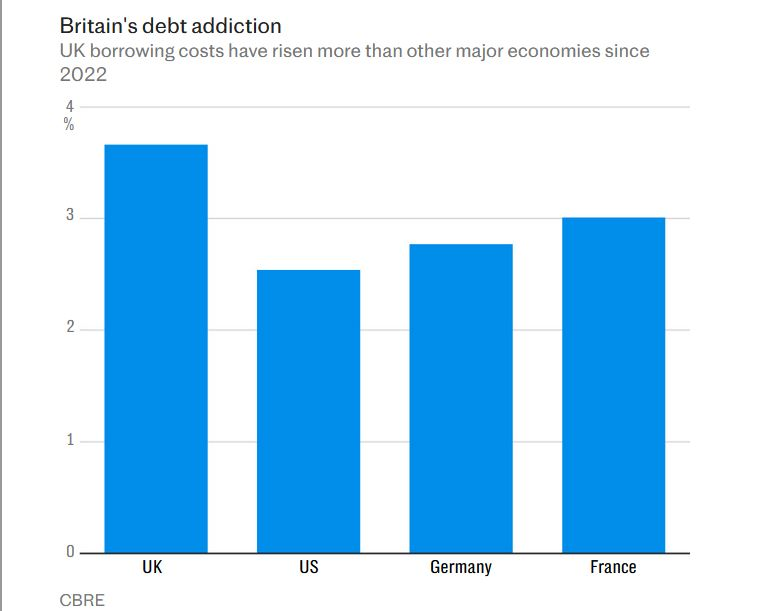

Britain’s fiscal position looks fragile and France’s almost hopeless. Politically paralyzed, neither seems capable of the austerity needed to restore stability. For now, our friends across the Channel are hiding behind the safety of the euro and the “German checkbook” that underpins it—but for how long?

Without a course correction, a generalized crisis is inevitable. Britain also appears incapable of making the necessary cuts, despite a comfortable parliamentary majority and four years to go until an election. This should allow for tough decisions, but the Labour government is proving incapable of making the spending cuts needed or taking the measures to boost productivity.

With interest rates at the highest in the G7, the pressures are already evident: debt service payments are skyrocketing, dramatically limiting the government’s ability to fund key priorities such as defence.

Black October

For financial markets, October is a particularly ominous month. Historically, it has been the autumn backdrop for some of the worst stock market crashes: the Panic of 1907, the Crash of 1929, Black Monday of 1987, and the global financial crisis of 2008—though technically that began with the collapse of Lehman Brothers.

But crashes can happen at any time of year. Accurate prediction is futile. Few people consistently do it, and even then, it’s usually a matter of luck, not insight. So for now, fear of “missing the moment” continues to drive the frenzied march toward the AI bubble.

That’s the great, inherent irony of markets: despite the lessons of history, they never know when to stop. Doomed to eternal cycles of boom and bust, they always push the limits of excess until the whole edifice collapses.

The Trigger

All the factors are now aligned for the “mother of all financial crashes” – but that doesn’t mean it will happen anytime soon. The markets need a catalyst, an event that will turn greed into panic and fear. We haven’t seen it yet. Rarely do bull markets simply die of “old age”. Alan Greenspan, the former chairman of the Fed, is a prime example.

He had warned as early as 1996 about the dangers of “irrational euphoria” in the stock market, but the dot.com bubble didn’t burst until 2000 – four years later. And when the markets finally collapsed, it was largely due to his own actions.

There was a mini-crisis in 1998 when the highly leveraged hedge fund Long Term Capital Management collapsed, threatening a domino effect. The Fed responded by bailing out, cutting interest rates, and flooding the system with liquidity—essentially adding fuel to the fire. Something similar could happen today.

Interest rates remain relatively high compared to the post-2008 era, leaving room for cuts if turmoil arises. Donald Trump will not want to see a market crash and recession in his lifetime. The Fed will be under pressure to act if the clouds begin to gather. That may keep markets “alive” for a while longer, but it will make the final bill even heavier when the inevitable crash finally arrives. Until then, “we keep dancing.”