As of July 1, 2025, gold is officially classified as a Tier 1, high-quality liquid asset (HQLA) under Basel III regulations – This means that U.S. banks can count physical gold at 100% of its market value as part of their core capital reserves.

For decades, many have rightly argued that gold is not just a shiny monetary relic of the past, but a serious, strategic asset for modern investors.

After years of developments in the financial system, it is safe to say that the world’s central banks – and now the U.S. banking system – are finally discovering this truth. As of July 1, 2025, gold is officially classified as a Tier 1, high-quality liquid asset (HQLA) under Basel III banking regulations. This means that U.S. banks can count physical gold, at 100% of its market value, towards their core capital reserves.

It will no longer be counted as 50% of a Tier 3 asset, as it was under the old rules. This is a seismic shift in how regulators treat gold, and it is a long overdue recognition of what many have been arguing for decades: Gold is money.

And it’s the kind of money someone wants to have in their possession when the world around them is collapsing.

What do central banks know (better than investors)?

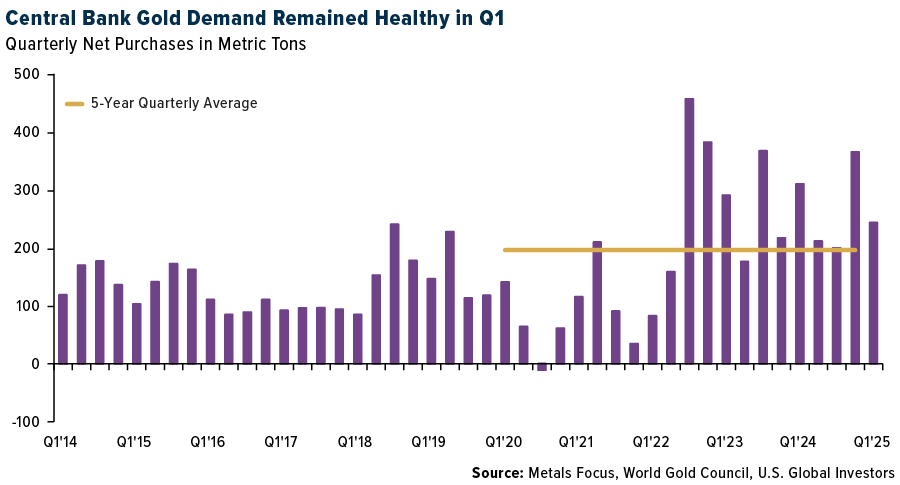

Central banks have been leading the massive gold buying spree for 15 years. In the first quarter of 2025, central banks added 244 metric tons of gold to their official reserves, according to the World Gold Council (WGC).

This performance is 24% above the five-year quarterly average. This is not an isolated incident. It is part of a long-term trend that began gradually after the 2008 financial crisis and accelerated after gold was reclassified under Basel III regulations in 2019.

According to the WGC, about 30% of central banks worldwide say they plan to increase their gold holdings in the next 12 months – the highest level ever recorded in its research.

Why do central banks buy gold? For the same reason you or I would buy it: to protect themselves from currency depreciation, geopolitical turmoil, and the rampant government debt that is choking developed economies. As the world’s fiat currencies are printed in ever greater quantities, the yellow metal remains one of the few truly finite, non-printable stores of value.

So if the world’s central banks are turning to gold, shouldn’t private investors do the same?

The Retail Resurgence

According to the latest Gallup polling data, nearly a quarter of U.S. adults now say gold is the best long-term investment — a sharp increase from last year and well above the 16% who say they prefer stocks.

Only real estate ranks higher in terms of performance. For the first time in more than a decade, Americans say they prioritize gold over stocks. Investors appear to be increasingly wary of the short-term stock market and are returning to this asset that has historically served as a safe haven in times of uncertainty.

Gold belongs in every diversified portfolio. In 2020, many predicted that gold could reach $4,000 an ounce on looser monetary policy and central bank balance sheet expansion. Today, the metal is trading at $3,340.

With President Donald Trump’s tariffs, ongoing global uncertainty, and rising demand for gold from central banks, it is predicted that gold could reach $6,000 an ounce in the medium to long term.

The paradoxical case of gold mining companies

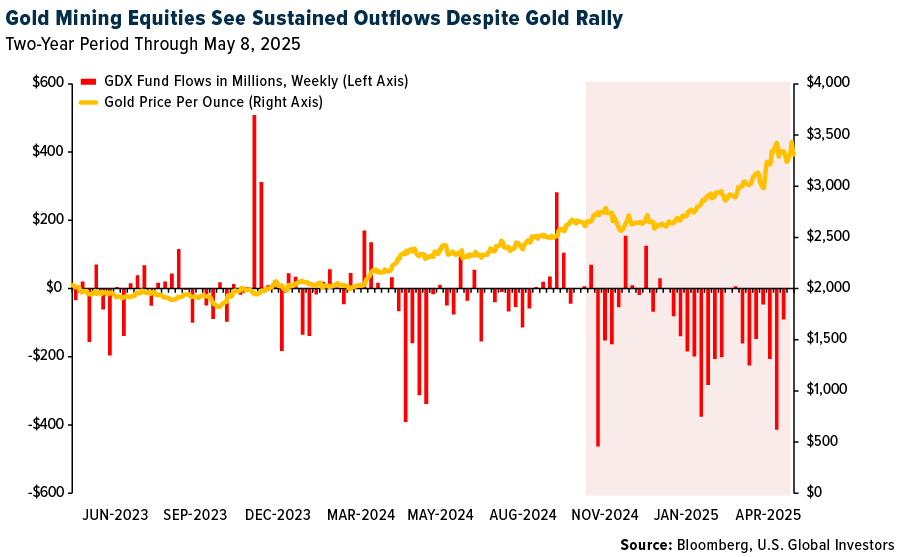

But here’s where things get interesting — and puzzling. While gold prices continue to hit new all-time highs, gold mining stocks have seen consistent outflows.

The VanEck Vectors Gold Miners ETF (GDX), which tracks many of the world’s largest publicly traded gold producers, has been losing money for months.

Even as gold prices have been rising, weekly capital flows have been negative, with investors pulling billions out of mining stocks. This disconnect is hard to ignore. It points to a deeper concern investors may have about the operational and financial health of mining companies.

Unlike physical gold, which simply tracks the spot price, mining companies are exposed to cost inflation, labor shortages, geopolitical risks and more.

These hurdles are not new, however, and should not overshadow the fundamental leverage that quality mining stocks offer in a bullish gold environment. Historically, gold stocks have tended to lag the metal itself until higher prices are deemed sustainable.

Institutional investors tend to wait for a clear trend reversal signal. This often means that retail investors can get ahead of the reversal. If gold prices remain high – or rise, as expected – we will see new investment flows into the mining space.

Meanwhile, we have seen investors increasingly favor physical gold-backed ETFs and streaming/royalty companies as lower-risk ways to gain exposure.

The term streaming/royalty refers to two types of companies that, while distinct, are often linked and derive their revenue from royalties or streaming agreements [an upfront payment or deposit to a mining company in exchange for the right to purchase a predetermined percentage of future physical production (e.g., ounces of gold, pounds of copper] at a certain, usually very low, predetermined price.

This is understandable. These investment vehicles offer the rise of gold with fewer headaches. But let’s not forget that mining companies are still extracting quantities of the metal from the ground. When profit margins improve, they can provide a significant upside boost.

The changes based on Basel III

Basel III is more than just a regulatory change. It confirms what many have long believed about gold’s status as a financial asset and a hedge against economic chaos.

If the world’s most powerful financial institutions are increasing their exposure to gold and regulators are reclassifying it as a top liquid asset, what’s stopping the average investor from joining the party?

As always, analysts recommend a 10% weighting in gold, with 5% in physical gold (bars, coins, jewelry) and 5% in high-quality gold mining stocks, mutual funds and/or ETFs.

The new era of gold has dawned…