The difficult equation of how to keep the dollar as the global reserve currency and at the same time depreciate its value so that the US economy can regain competitiveness and reduce its trade deficits with the rest of the world is up to the Donald Trump administration – and all this against the backdrop of an economic war.

The solution that should be preferred is to “disarm” the holders of US debt – Asians alone, including China and Japan, hold over $3 trillion in US assets – by expanding the dollar’s monetary environment through stable coins.

In one move, two goals are achieved:

This increases the demand for US debt and

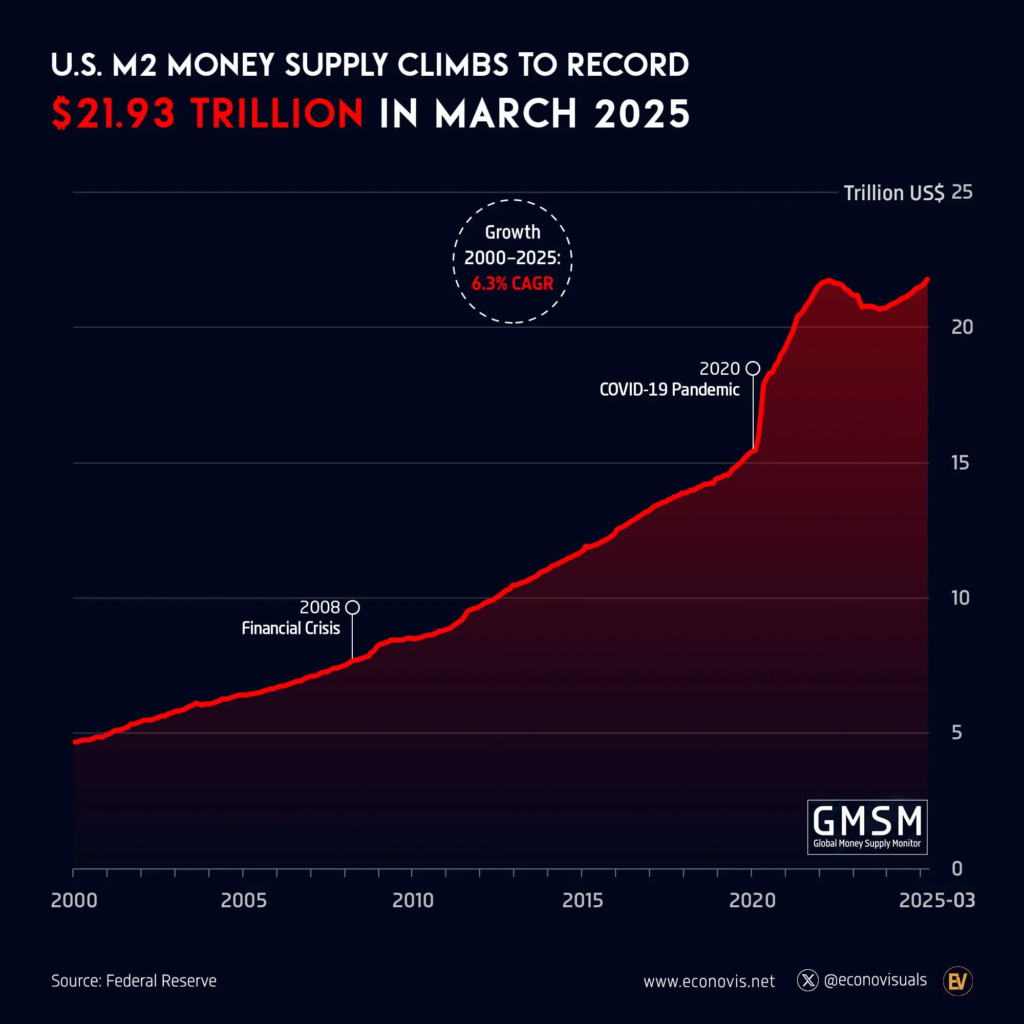

reduces the cost of servicing critical large maturities without increasing the supply (M2) of dollars that would put inflationary pressures on the economy (as the Fed has done so far) while at the same time keeping US debt holdings tied to the dollar system.

If they legalize cryptocurrencies, investors will turn to this activity. He was talking about stable coins – cryptocurrencies based on blockchain technology and usually linked to the dollar and, increasingly, for managing liquidity in global payments.

Congress is expected to set the rules for these cryptocurrency creations. The STABLE Act in the House of Representatives and the GENIUS Act in the Senate are bills that have a common goal: to put the issuance of stablecoins into a regulatory framework, specifying precisely how much capital, liquidity, and risk management are required.

They also aim to clarify which federal or state agencies can play the role of regulator of this market.

But there is another, less flashy side effect: How will the widespread acceptance of stablecoins among traditional institutions worldwide affect the United States’ nearly $28 trillion bond market?

The point is to turn US Treasury bonds into the backbone of the stablecoin reserve, because there aren’t many other assets that come close in terms of security standards and liquidity. There is a bid for a digital dollar, it needs to be backed by assets that are as risk-reduced as possible.

This is similar to the hundreds of money market funds, which are issued by giants such as BlackRock, Fidelity and Vanguard and contain over $6 trillion in assets, mostly in US bonds.

A money market fund (MMF) is an open-ended investment fund that holds short-term debt issued by governments, banks and large companies.

MMFs play an integral role in the global financial system as sources of short-term funding for organisations such as governments, pension funds, insurance companies, companies, local authorities and charities.

Money market funds have also taken on a secondary function as a cash reserve for ordinary “retail” investors chasing a better rate of return than they can get from a bank account or cash ISA.

The big difference is that, unlike a money market fund from, say, Fidelity, which might give you a 4% annual return, most stablecoin issuers have so far resisted offering any kind of yield or income to their holders.

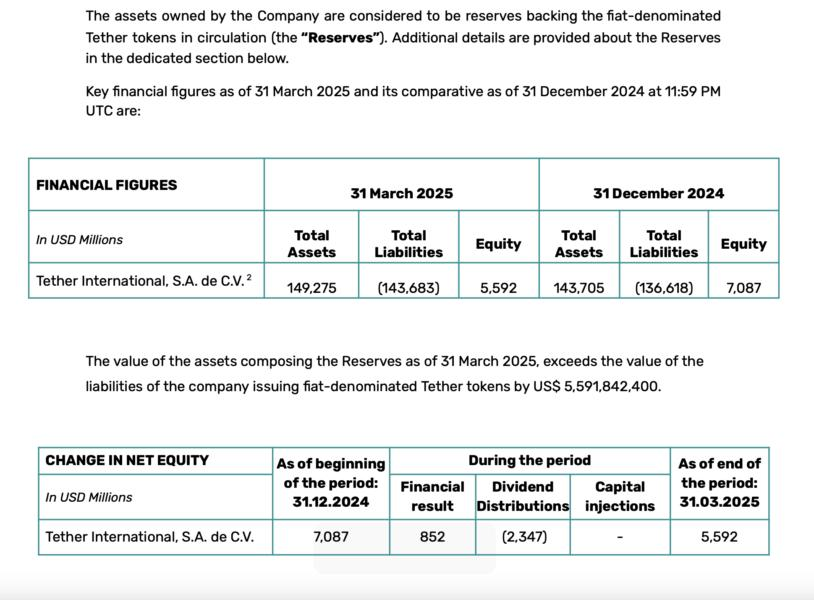

That’s one reason why Tether, the largest company in the space, has extremely high profit margins and reported operating profits of more than $1 billion in the first quarter of 2025.

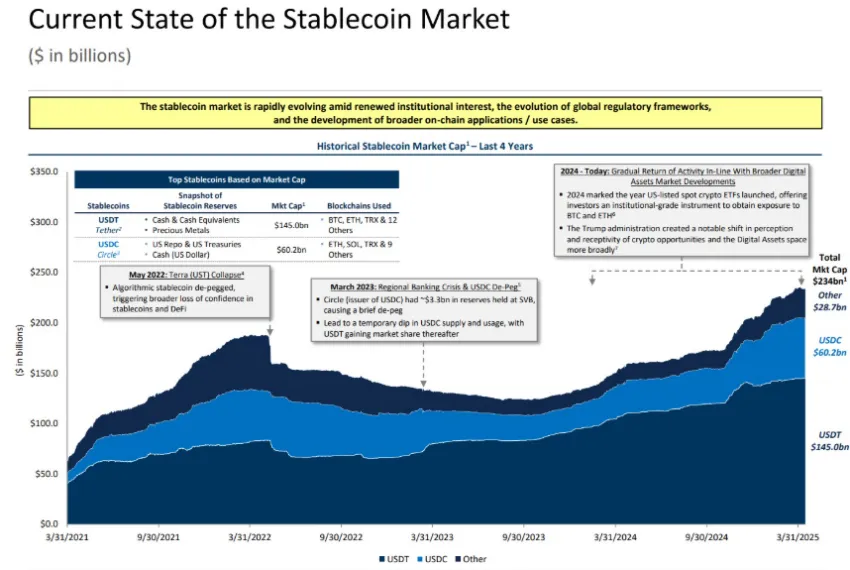

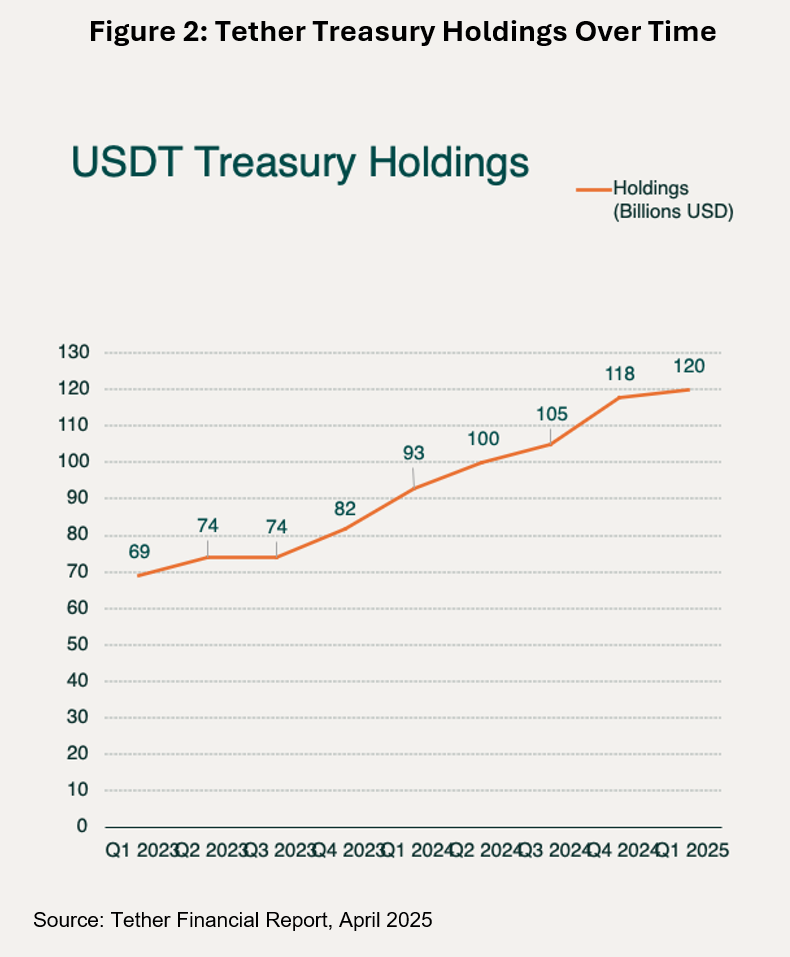

Right now, the dozens of stablecoin issuers out there — though most notably Tether, based in El Salvador, and Circle, based in New York — hold about $150 billion in U.S. debt, mostly short-term bonds.

This is a rounding error in the $28 trillion Treasury bond market and a fairly insignificant portion of the $6 trillion in outstanding Treasury bills.

Most U.S. Treasury bonds are still held by the government itself if you count Social Security and federal pension funds.

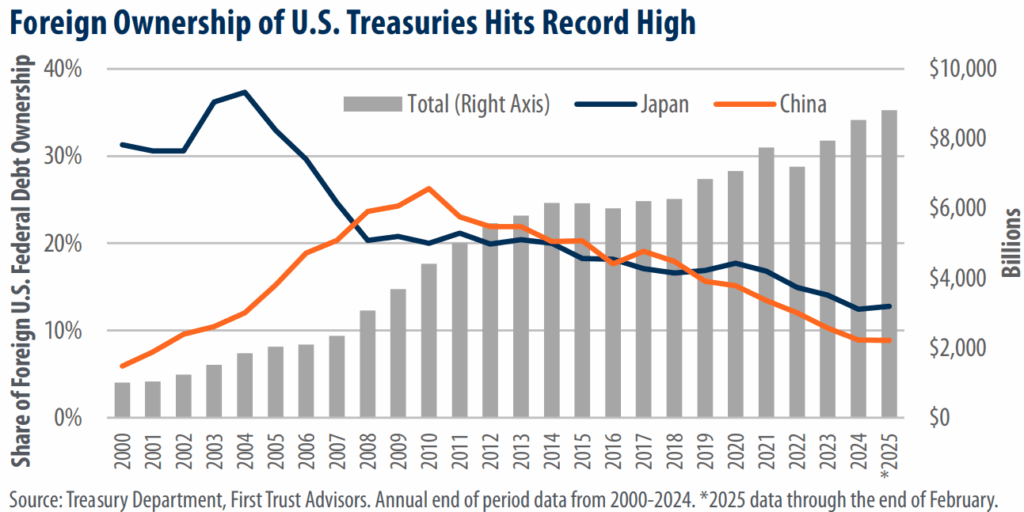

U.S. mutual funds, banks, and insurance companies are the next largest holders, with foreign investors accounting for about 30% (about $8.8 trillion), led by Japan and China.

However, Britain’s Standard Chartered Bank, an $874 billion institution that offers custody services for cryptocurrencies, predicts that the global stablecoin market could skyrocket from $240 billion to $2 trillion in just three years.

Both stablecoin regulations explicitly identify Treasury bonds with maturities of 93 days or less as one of the few acceptable reserve assets.

That could mean an additional $1 trillion in demand for Treasury bills in the short term, according to an April 30 presentation by the Treasury Borrowing Advisory Committee (TBAC), a group of senior bankers, asset managers and hedge fund representatives that advises Treasury officials every quarter.

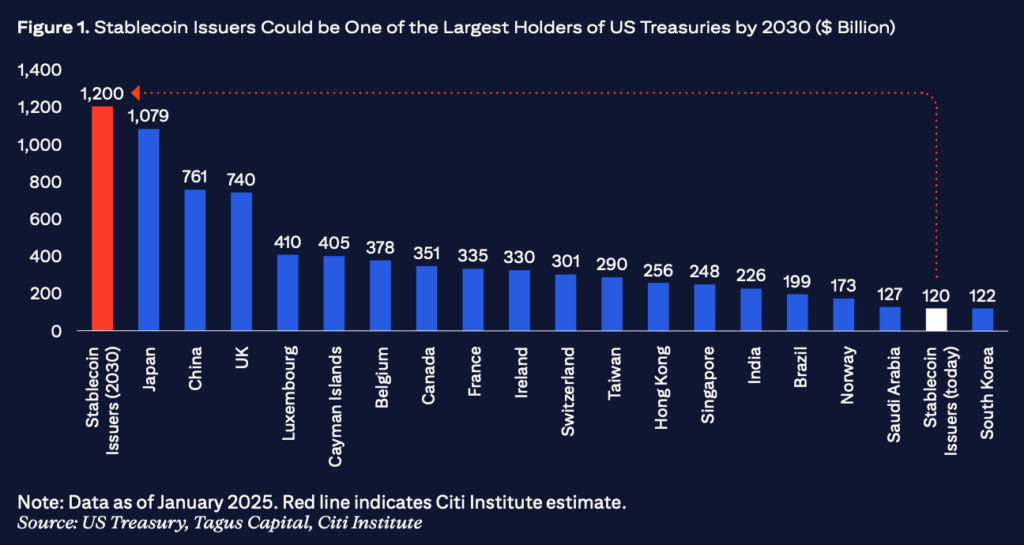

Citi’s research team goes a step further, suggesting that by 2030, issuers of stablecoins could surpass any single foreign country as holders of U.S. government debt. Despite its controversial history, Tether, with $120 billion already invested in US bonds, could become the largest holder if it complies with the new regulations.

Stablecoins Data

A major market turmoil could erupt as the U.S. national debt tops $36 trillion, growing by another trillion about every 176 days.

Meanwhile, creditors like China and Saudi Arabia are quietly reducing their holdings of U.S. assets. China’s holdings of U.S. debt fell to $761 billion earlier this year, the lowest since 2009, while Saudi Arabia’s share has fallen to a low of $126 billion, reflecting a global restructuring of reserves and growing skepticism about U.S. government debt.

If stablecoins are introduced around the world, as in places like Buenos Aires and Nairobi, who use them for everything from paying their rent to hedging against local currency volatility, they will emerge as a new, willing class of lenders in the US.

Trump Administration Changes

The Donald Trump administration has already made its stance on stablecoins clear.

Cryptocurrency and AI market tsar David Sacks has argued that they could help ensure the global dominance of the dollar, and President Trump has pushed Congress to introduce a bill for ratification before the August recess.

“Stablecoins have the potential to ensure the dominance of the U.S. dollar internationally, to increase the use of the dollar digitally as a global reserve currency, and in the process potentially create trillions of dollars in demand for U.S. Treasuries, which could lower long-term interest rates,” Sacks said during his first press conference in February.

Additionally, the Trump family business, World Liberty Financial, announced plans for its own stable coin.

The Fate of a Pending Regulation

On May 1, World Liberty announced that the token would be used by MGX, a company backed by the Abu Dhabi government, to invest $2 billion in Binance, the cryptocurrency exchange.

A few days later, nine Senate Democrats, including four who previously supported the “GENIUS” stablecoin bill, issued a statement saying they would oppose the legislation in its current form.

However, lawmakers had been pushing the idea of stablecoin issuers as ultimate purchasers of Treasury bonds even before Trump took office.

Senator Ritchie Torres of New York argued in an article last fall that greater adoption of stablecoins means more demand for Treasury bonds and, in turn, lower borrowing costs. Earlier, former House Speaker Paul Ryan presented stablecoins as a hedge against a future wave of foreign sell-offs: if traditional buyers retreat, dollar-backed token issuers could fill the gap.

The US could not have come up with a better innovation for the dollar than a stablecoin. It makes the dollar more widely available.

Its rise as a global reserve currency and the counterargument

If it falls into the wrong hands, there is due process by which the government can “freeze” and seize assets. It checks so many boxes: it creates buyers for the debt, it lowers interest rates.

But if the US Treasury bond market, for whatever reason, comes under pressure, if there are doubts about the US’s ability to repay its payments, then for stablecoin issuers, it is no longer a safe asset that can substitute for a claim on cash. And if a major stablecoin issuer collapses, it could be forced to dump Treasury bonds en masse, destabilizing the market.

Unlike foreign central banks, stablecoin issuers face a real risk of a run: panicked clients can withdraw funds immediately, triggering immediate selling pressure.

Of course, this risk also applies to Money Market Funds. In 2008, after the collapse of Lehman Brothers, the $65 billion Primary Reserve Fund, which held less than 2% of Lehman’s trading securities, faced a run and was forced to liquidate its assets.

For the first time, the bond market is backing the monetary value of a payments system, providing a backstop for an entirely new monetary claim. Should the government bail out stablecoin issuers so that they don’t default on the dollar claims they have issued?

Policymakers have not fully addressed these questions, and they should.

Creating significant new requirements for Treasury bills and Treasury-backed repos and reverse repos by stablecoin issuers could lead to dangerous shortages of available Treasury bills, especially in times of economic stress.

The September 2019 repo market crisis and the March 2020 sell-off are cautionary tales. For now, the demand for another trillion dollars of Treasury bills from stablecoin issuers may seem manageable. But the landscape is changing rapidly.

Large financial institutions like Bank of America and Fidelity, which manage trillions in assets, are considering issuing stablecoins. Visa and Bridge, which was acquired by Stripe, have just launched stablecoin-linked credit cards across Latin America, and Mastercard has unveiled a new platform that will allow users to pay for purchases with stablecoins and withdraw them directly to their bank accounts.

The assumption that stablecoin issuers will simply fill the gap is not something policymakers should be relying on. And there is another potential risk: banks and other stablecoin issuers will limit their reserves to Treasury bonds.

Bank-issued stablecoins could be subject to the fractional reserve rules that banks have long used to direct their FDIC-insured (the regulator) deposits into more profitable areas.