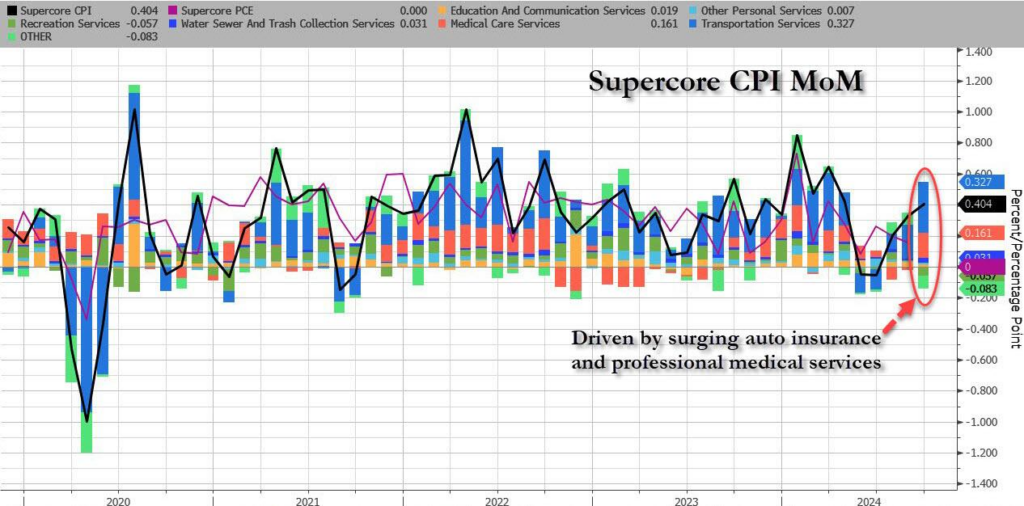

Inflation in the US fell to 2.4% against forecasts for a slowdown to 2.3%. On the other hand, “core” inflation recovered to 3.3%, against forecasts that it would remain unchanged. At the core, services inflation rebounded from 4.3% to 4.4% and accelerated strongly from 0.1% to 0.6% month-on-month (this is the part of the core that is supposed to be most closely linked to wage growth and is affected by the Fed’s efforts to bring the labor market into better balance). Meanwhile, in the minutes of the September 17-18 meeting published on Wednesday, some participants noted that “the rate of increase in prices of basic non-housing services had declined further”. Well, think again. On the bright side, housing inflation eased from 5.2% to 4.9% and fell on a monthly basis from 0.5% to 0.2%. However, core inflation remains persistent. In contrast, US jobless claims in the first week of October rose to 258,000 from 225,000 a week earlier. That’s a big jump, part of which appears to be related to the weather. Indeed, there were large percentage increases in southeastern states such as North Carolina, South Carolina, Florida, and Tennessee that were affected by Hurricane Helene. On the contrary, for the labor market, the picture of the Employment Report will prevail: strong job growth, a decrease in unemployment and a strengthening of average hourly earnings. So to summarize, September gave us a strong labor market, a rebound in core inflation…. and an interest rate cut of 50 bp. from the Fed. However, three Fed officials remain convinced that inflation is moving in the right direction, and the FOMC may continue to cut rates.

France

Meanwhile, French Prime Minister Michel Barnier presented the 2025 budget. Given the dire state of France’s public finances, it was closely watched.

Barnier warned that without intervention next year’s deficit could swell to 7% of GDP. So swift action is needed, so Barnier presented plans to cut the deficit by €60bn next year, around 2% of GDP.

The package includes a combination of broad spending cuts and tax increases on large corporations and wealthy individuals. Although the plans are quite detailed, Prime Minister Barnier stressed that the draft budget is a starting point for MPs.

However, this transparency raises the concern that some safe cost-saving or revenue-raising measures may be replaced by overly optimistic proposals.

Furthermore, this open stance clearly shows that Barnier lacks a parliamentary majority. His government relies on opposition support, which remains uncertain.

Chances are Barnier will face another vote of no confidence.

French budget deficits are estimated to reach 5.1% of GDP in 2024 and 4.2% in the next two years.