The European Central Bank (ECB) recently published data on the borrowing rates of households, businesses and the overall long-term borrowing costs respectively for both the Euro area and each of its member countries (Source: ECB, https://data.europa.eu/euodp/en/data/publisher/ecb). What continues to trouble us from the graphs below is the fact that a Eurozone of different speeds appears and always based on its borrowing rates.

by Thanos S. Chonthrogiannis

©The law of intellectual property is prohibited in any way unlawful use/appropriation of this article, with heavy civil and criminal penalties for the infringer.

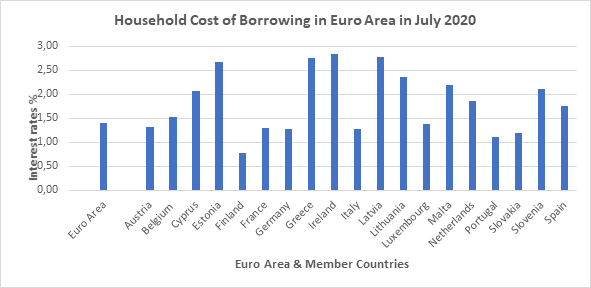

More specifically, in the first Chart entitled “Household Cost of Borrowing in Euro Area in July 2020” we observe that member countries such as Greece, Ireland, Lithuania, Latvia, Estonia, Cyprus and Slovenia have the highest borrowing costs for their households.

Chart 1

The member countries Greece, Cyprus, Ireland are shown not to have overcome the global financial crisis of 2008 and in addition for specific reasons each of them (i.e. high degree of non-performing loans, high operating costs of financial institutions, high protection of first residence from bankruptcy proceedings, etc.).

In euro area member countries such as Lithuania, Latvia, Estonia a key factor is the high borrowing costs of these member countries on international markets which affects the borrowing costs of the banks of these member countries as well as the high transport costs of goods and products from the other member countries.

In addition to these other factors are the high operating costs of banks, and the increased risk they present geopolitically due to their proximity to Russia.

Chart 2

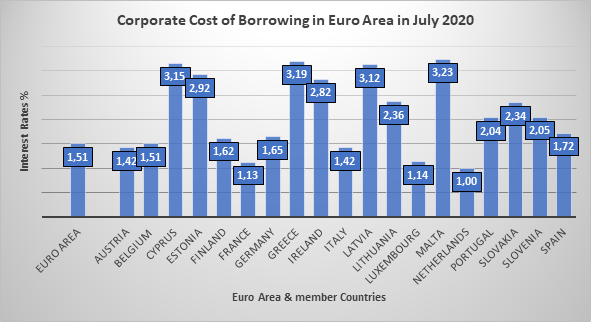

The same pattern for the same euro area member countries is observed both in business-related borrowing costs (Chart Two entitled “Corporate Cost of Borrowing in Euro Area in July 2020) and in the long-term borrowing costs of member countries (see below the third Chart entitled «Long-term Cost of Borrowing in Euro Area in July 2020»).

Chart 3

The Commission should put its weight on correcting these extreme economic disparities in the borrowing rates of the member countries concerned in relation to the average rate, in order to gradually bring about greater convergence of these economies with the stable central economic core of the euro area such as France, Germany, Belgium and the Netherlands.

For member countries such as Greece, Cyprus, Ireland, “bad banks” should be created that will either be created through the acquisition of one existing bank by the others by transferring its sound assets to the other banks-shareholders or by the creation from the outset of such a bad bank that in this case it will be fully financed by the other banks.

The cost of setting up this bank should in no way be borne by the public sector. Then all outstanding non-performing loans from the entire banking sector will have to be transferred to the bad bank. Then re-invoicing these loans at current prices and selling them for the banks-shareholders to collect part of their money.

In addition, there should be mass redundancies of bank employees and a reduction in bank sizes without reducing the quality of their services (through continuous technological upgrading). The change in bankruptcy proceedings should also enter the “frame” of the required changes and be such as to help the auction of houses.

At the same time, the state in these member countries will have to make sure to find decent accommodation-houses/apartments that will temporarily house families who are bankrupt, and their homes are auctioned.

Member countries such as Lithuania, Estonia, and Latvia, except the above policies, should intensify market liberalization policies and reduce the size of annual state expenditure (e.g. a logical target will be an annual government budget expenditure at 15% of GDP) to further reduce taxation.