The fiscal position of many advanced economies has deteriorated dramatically, it is now a well-established picture. The nightmare of the debt crisis has shifted from peripheral economies like Greece to the major players. Recently, the spotlight has turned to the United States, where the “One, Big, Beautiful Act” has credited the White House with large federal budget deficits and has heightened concerns that the country is now on a more dangerous fiscal path.

That is the story. But this is not yet another example of American exceptionalism. Fiscal weaknesses are intensifying across advanced economies.

In France, the situation seems particularly worrying, and the government has rushed to impose a memorandum of understanding on its own to avoid becoming Greece, although the United Kingdom and Italy are also causes for significant concern and are in the sights of the bond market punishers.

This means that the famous punishers are also lurking in the event that the numbers do not come out – as in the sudden ouster of Liz Truss in 2022 with only 45 days in office as prime minister of Britain – to punish governments that appear to be losing control of the fiscal wheel.

What is called in their terminology “political risk” will be the main menu of developments in the debt markets. Any government that does not convince through concrete actions that it wishes the country to return to a fiscally virtuous circle will be violently beheaded.

This means a domino of political crisis that will be triggered by markets that will price the risk of debt default in (rising) bond yields.

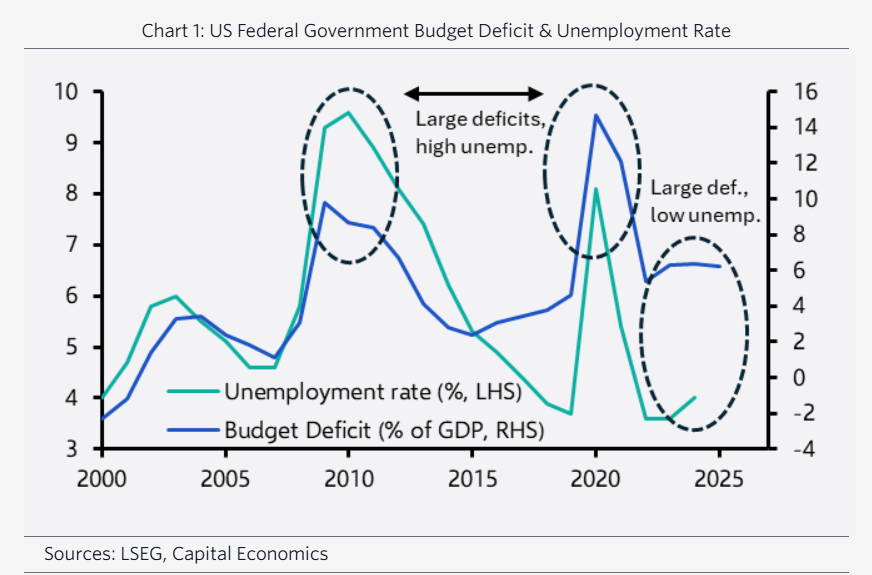

Back then, government borrowing was a cushion against the collapse of private-sector demand. As economies recovered, so did tax revenues, helping to restore fiscal balance.

In other words, deficits were cyclical. That is not the case today. These deficits are structural, and therefore require either tax increases or spending cuts to reduce them—and nothing else!

A different economic climate

Worse still, fiscal overruns occur in a very different economic climate. Back in the wake of the global financial crisis, ultra-loose monetary policies meant that government bond yields were negative in real terms.

Now, the real cost of borrowing is firmly in positive territory. The era of “free money” is over. As a result, the same deficits that once seemed tolerable – or even desirable – now constitute a growing fiscal burden as a share of GDP. That is the main point.

When governments run large deficits in good times, they accumulate problems. At some point, markets will react.

But there is no clear threshold at which a crisis begins. No magic debt-to-GDP ratio or budget deficit figure rings bells in the markets.

Japan, after all, has carried gross public debt above 200% of GDP for more than a decade, supported in large part by its deep pool of domestic savings.

Fiscal sustainability is less about hard metrics and more about the economic framework and confidence in the policy framework.

The Faces Behind Politics: Trust is the Key

And trust, it turns out, is as much about people as it is about politics. Events in recent months have underscored this point. The U.S. bond market was rocked in April as concerns about fiscal mismanagement and volatile policy signals, including President Trump’s “Liberation Day” (April 2) tariff announcement, sent long-term yields soaring. It took Treasury Secretary Scott Bessent’s intervention and a swift reversal of tariffs to calm things down.

Then, in early July, a visibly emotional Rachel Reeves in the House of Commons, combined with the failure of then-Prime Minister Keir Starmer to support her, fuelled speculation that the UK Chancellor was about to quit and triggered a sharp sell-off in gilts and sterling.

It was only after the UK government issued a more emphatic statement of support for the Chancellor that the gilt market steadied and yields fell.

What links these episodes is not fiscal policy but personalities

In both the US and the UK, investors were reacting not to new revenue or spending data, nor to the wording of a bill, but to who was in charge. They panicked when it seemed that trusted figures in the political establishment were losing control or influence. As a former hedge fund manager, Scott Bessent has credibility on Wall Street.

Reeves, who comes from the fiscally cautious wing of the Labour Party, has invested her political capital in strict fiscal rules. Subsequent rebounds in bond markets were not due to policy changes but to relief that trusted figures were, or were perceived to be, in control.

This is not a new dynamic. Bond markets have long responded strongly to the arrival or departure of key figures. The appointment of Mario Monti as prime minister in 2011 helped calm Italian bond markets at the height of the eurozone crisis.

The current market mood is a far cry from the panic of the eurozone debt crisis. But in a world where most advanced economies are running large structural deficits – even at full employment and with higher interest rates – recent moves in bond markets show that personalities can matter as much as policies, and sometimes more.

Investors should keep one eye on the fiscal numbers and the other firmly on who is in charge. If a crisis breaks out, it is as likely to come from a change of personnel as from a change of policy.

In Europe, the immediate risk is not France’s presidential election in 2027, but an early collapse of the government – potentially leading to an even weaker minority government that abandons efforts to reduce the deficit. That will send markets into a tailspin.

In the UK, the risk is that Reeves will be replaced by someone less committed to fiscal discipline. That will send markets into a tailspin.

And in the US, fiscal stability may depend on whether Secretary Scott Bessent continues to wield influence and enjoy the favor of President Trump. Fiscal sustainability, then, is increasingly a question of political sustainability. Markets are watching – not just the numbers, but also the faces and the trust they inspire.

President Donald Trump will either reverse the fiscal drift – for example by achieving his tax revenue targets and deregulating the economy – or his entire plan will collapse like a pack of cards in a spectacular and traumatic way for the rest of the world.