The US banking system is reeling as the commercial real estate market may turn out to be as toxic as the subprime mortgages that led to the 2008/2009 crisis. At the same time, approximately 1 trillion dollars are the loans that the official banking sector has granted to the shadow financial system – how much it especially increases the risk of a mountain of non-performing debts.

Federal Reserve officials ended the narrative of a “strong and resilient” banking system in their Jan. 31 announcement. That same day shares of New York Community Bank fell after the bank reported a loss of thirty-six cents per share when analysts had expected earnings of twenty-seven cents per share for the fourth quarter.

Internal or external auditors occasionally look at individual loans in a bank’s portfolio and make judgments as to whether those loans are worth what the bank has valued them at, or are undervalued due to revised appraisals and other issues, or are specific to an individual property or market in total.

Then the bankers reluctantly set aside the positive predictions and write losses on their books.

Damage Prediction +790%

In the case of real estate loans at New York Community Bank, credit controllers must have forced management to increase the bank’s provision for loan losses by 790%, to $552 million. This “opening” of the balance sheet led to the fourth quarter loss and caused the bank to cut its dividend. The bank recorded an increase of nearly $2 billion in the subprime category — debt with the potential for bankruptcy/default.

The bank also reported a net loss of $42 million – debt that is unlikely to be repaid – on a commercial real estate loan on which the borrower stopped paying interest. Apparently the Bank had higher levels of bad loans throughout the financial crisis and throughout the pandemic.

Powell’s silence

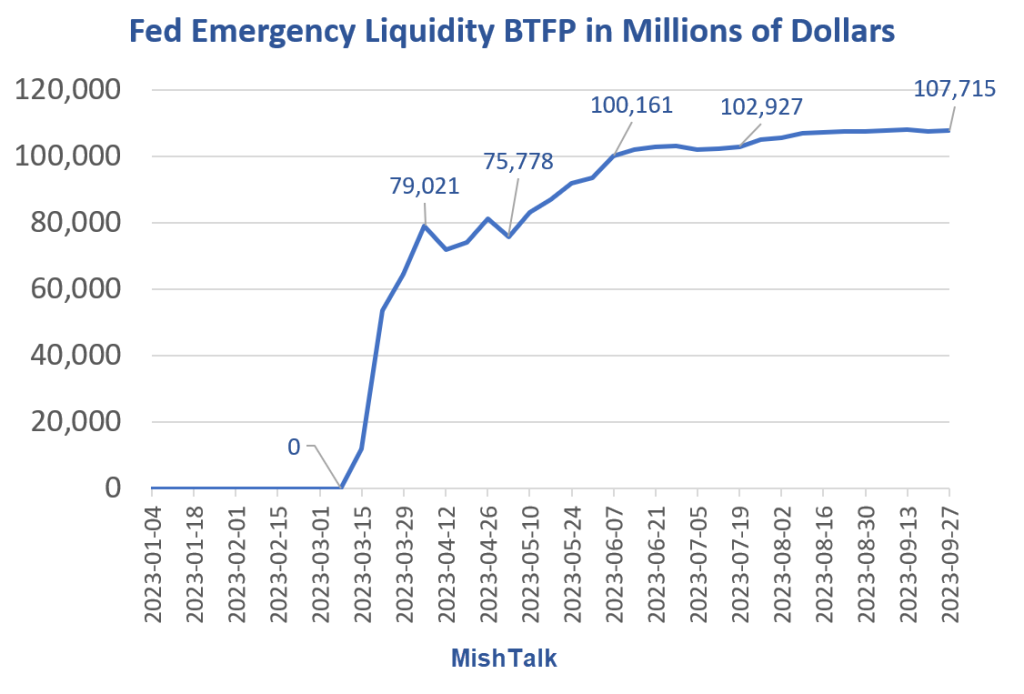

Fed chief Jay Powell made no mention of New York Community Bank in his remarks, and reporters did not ask him about the bank’s problems. There were no questions about the Bank Liquidity Program, which expires on March 11, despite its use by financial institutions rose to a record high.

The credit facilitation program and the banks

The program’s popularity is not due to new pressures on banks. However, some banks have recently found a way to use the program by speculating on the difference between what they pay to borrow the funds and what they can earn by parking the funds at the central bank as overnight deposits.

As of January 31, banks had borrowed more than $165 billion from the funds of the credit facility program. It is doubtful that there are no new pressures on the banks. New York Community Bank is not an anomaly but an indication of a real systemic risk.

Every sector of real estate, not just commercial real estate, has a problem with interest rates skyrocketing by 500 basis points. The office market is having an existential crisis right now. It’s a $3 trillion total asset class that’s probably worth $1.8 trillion (now). There are $1.2 trillion in damages spread out somewhere and no one knows exactly where all the damages are.

The percentage of loans that banks have so far reported as past due is a fraction compared to the defaults that will occur in 2024 and 2025. Banks remain exposed to these significant risks, and a possible rate cut next year will not solve banking problems.

The plan for the Credit Facility Program was hurriedly drawn up over a weekend in March of last year after the collapses of Silicon Valley Bank and Signature Bank (Signature’s assets were bought by New York Community Bank). To hide their embarrassment at banks using the safe-rate facility, they say they are closing the program because there is no pressure on the banking system. But there is significant pressure on the banking system.

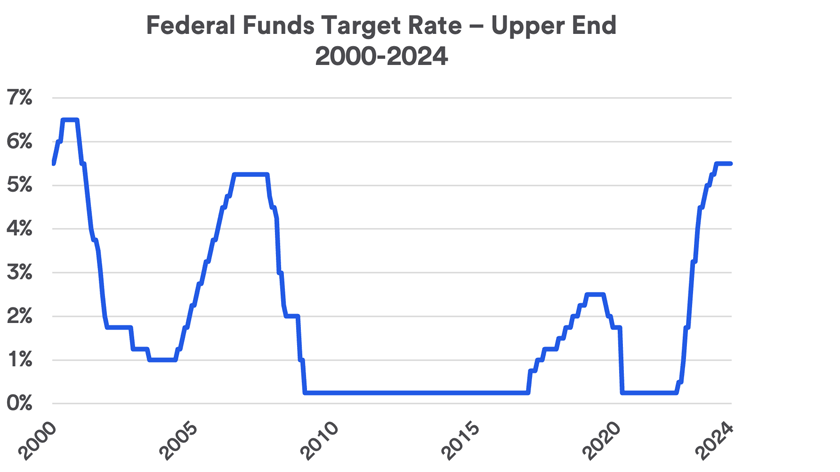

Coined credit expansion through the Fed is always unstable, as the more extensive the inflationary creation of new money, the more likely it will suffer contraction and subsequent deflation.