Europe’s soaring public debt levels should prompt governments to rethink their role in delivering essential services to EU citizens, according to the International Monetary Fund (IMF), which sees an urgent need to impose shock measures on economies that would overturn the famous European model.

In a study published on Tuesday, November 4 (“Regional Economic Outlook for Europe, October 2025“), the IMF warned that Europe’s debt levels risk becoming “explosive” if reforms are not implemented in labor markets and businesses, and if budget deficits are not reduced by increasing tax revenues, limiting social spending and improving public sector efficiency.

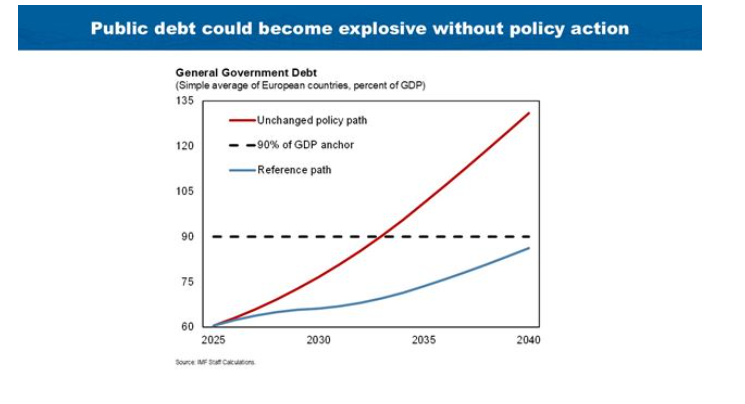

However, the Fund also warned that Europe’s debt levels — which are expected to double by 2040, reaching an average of 130% of GDP — are now so high that even with rapid reforms, “a reassessment of the role of the state in the economic sphere may be inevitable in some countries.”

“If reforms and medium-term fiscal adjustment are not sufficient, then more radical measures could include a reassessment of the scope of public services and other functions of the state, which could affect the social contract,” the IMF said.

The IMF study

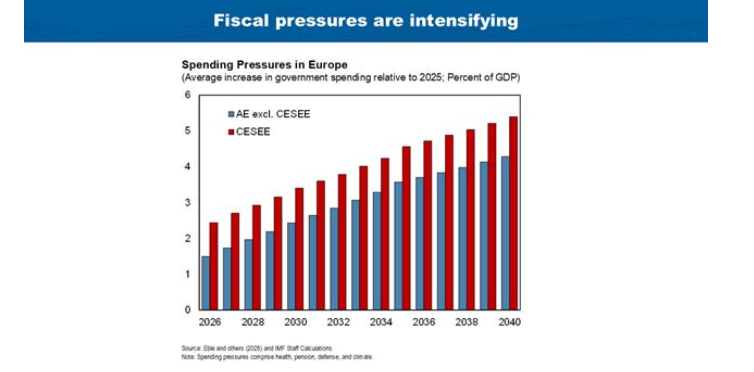

The surge in public debt comes at a time when EU governments are under increasing pressure to support ageing populations while also increasing strategic investments, particularly in green technology and defence.

Last year, former European Central Bank (ECB) president Mario Draghi said the EU would need to increase its annual investment by at least €800 billion a year — or around 4–5% of the bloc’s annual GDP — to keep pace with the United States and China.

He said up to half of that amount would need to come from the public sector. Twelve of the EU’s 27 member states now have debt-to-GDP ratios above the bloc’s 60% limit.

Several major economies — including Italy, France and Spain — have debt levels above 100% of GDP. Italy and France are also among nine EU countries under excessive deficit procedure by the European Commission, for breaching the 3% budget deficit limit. However, it notes that relatively low borrowing rates, higher tax revenues and deeper, more liquid capital markets now allow most European governments to maintain debt-to-GDP ratios of up to 90% without jeopardising fiscal sustainability.

What reforms are being proposed?

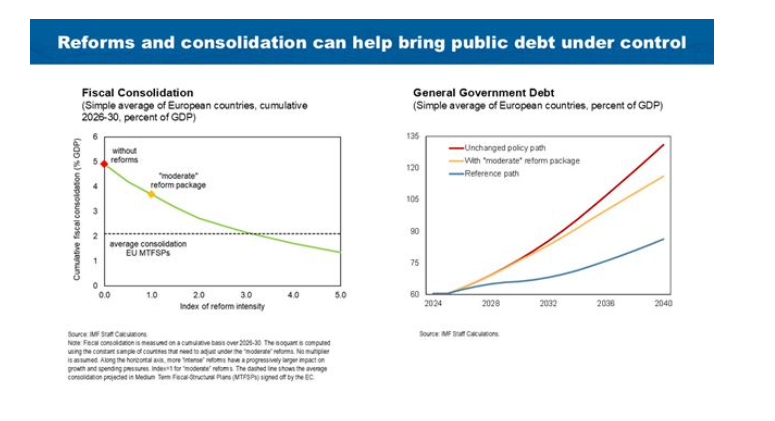

The Fund added that the need to reduce deficits and debt could be significantly mitigated through growth-enhancing reforms, such as:

deepening the single market for capital and energy,

simplifying the regulatory framework for businesses, and

issuing common European debt to finance critical “public goods” such as energy and defense infrastructure.

Even so, a “modest reform package” is unlikely to restore debt sustainability in many member states, the IMF said.

Public spending cuts of 1% of GDP over five years

Around a quarter of European countries would need to cut net public spending by more than one percentage point of GDP per year for five consecutive years — significantly more than the typical fiscal adjustment of recent decades.

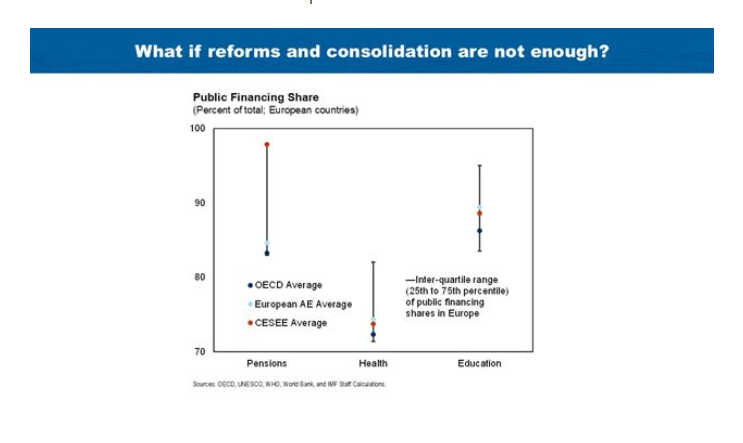

“In these countries, the debate over the scope and sustainability of the ‘European model’ seems inevitable,” the Fund said. Governments, the report said, could try to distinguish between “essential” and “premium” services in critical areas such as pensions, education and health — with only essential services remaining publicly funded and available free of charge.

Strong social reactions

The Fund, however, acknowledges that such measures are likely to encounter strong social reactions, as anti-government discontent is already growing in many European countries due to the deterioration of public services, deindustrialization and stagnant or declining wages.

Alfred Kammer, director of the IMF’s European Department, said that “some segments of the European population will experience the proposed reforms as painful, but we have to deal with that pain.” “When you do reform, you don’t want to just cause pain for years,” Kammer told reporters, adding that governments should be honest and seek compromises with citizens.

The Fund concluded that “gradual steps” are more likely to be realistic and win public support.

“Governments need to clearly explain the rationale for reforms, identify the spending pressures they face, and redefine public expectations,” the IMF said.

In a complete deadlock

One could not claim that Europe does not have a debt problem. The data provide some basis for this claim: although debt is high in historical terms, it remains below the 110% average of advanced economies.

Moreover, the eurozone’s debt-to-GDP ratio stands at 88%, around 20 percentage points higher than in 2000, but 10 points lower than in 2020. It estimates that if no action is taken, Europe’s public debt will reach 130% by 2040, exceeding the “warning threshold” of 90%, beyond which markets are likely to react strongly. Are there alternatives? The mathematical reality is that if governments do not actively repay their debt, the debt-to-GDP ratio will rise when growth slows or declines. The reforms proposed by Draghi — such as removing national barriers to the integration of European financial markets — could boost growth and reduce the need for drastic cuts to the welfare state.

None of this necessarily means that the International Monetary Fund is wrong. But it does suggest that there are many alternatives, less politically toxic, worth considering before governments abandon one of the key pillars of modern European society.