Beyond the fading glory of the G7 and G20 — groups of states formed in the aftermath of World War II and now mired in stagnation and demographic decline — a new alliance has emerged on the geoeconomic map: the BRICS+ group.

This coalition — Brazil, Russia, India, China and South Africa — represents a rising union of states determined to expand their trading influence, secure resource flows and accumulate the economic surpluses that once enriched the great empires of Europe.

Coined in 2001 by Sachs economist Jim O’Neill as “BRIC,” the term began as a simple classification of markets and economies whose growth threatened to reshape the balance of global trade. But what began as an acronym quickly morphed into an ambitious union of states.

Since 2006 – and especially after the financial crisis of 2008/2009 – the four founding countries have been coming together to strengthen trade ties, coordinate investments and align political strategies. In 2009, the first official summit in Yekaterinburg was about more than diplomacy – it signaled the return of a multipolar world, where trade routes, resources and precious metals no longer flowed only to the old imperialist capitals, but to new centers of wealth creation.

In 2010, South Africa joined the group, transforming BRIC into BRICS and extending the group’s reach to the mineral-rich shores of Africa. By 2025, BRICS had evolved into BRICS+, a powerful trading confederation with eleven full members — Brazil, Russia, India, China, South Africa, Saudi Arabia, Egypt, the United Arab Emirates, Ethiopia, Indonesia, and Iran — controlling vast reserves of commodities and strategic goods, along with the markets and labor force to process and consume them.

Further expanding its reach, the bloc introduced a new category of “partner countries” on January 1, 2025, bringing Belarus, Bolivia, Cuba, Kazakhstan, Malaysia, Thailand, Uganda, Uzbekistan, and Nigeria into its sphere of influence.

Although not full members, these partners now participate in BRICS+ summits and ministerial meetings, and can endorse the bloc’s statements, thereby deepening their integration into its expanding sphere of economic and political influence.

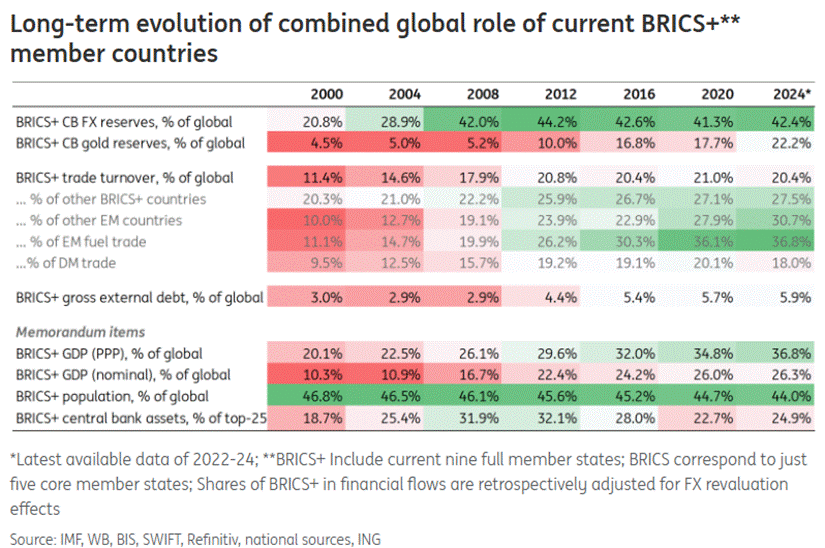

Together, these nations now control about 40% of global output in purchasing power parity terms, according to IMF data (April 2025) — surpassing the economic power of the old developed markets in key areas of trade and production. By the end of the year, their share is expected to rise to 41%, leaving behind the… meager 28% of the G7 group.

The flow of gold, commodities and trade is no longer directed to the aging imperialist ports of the West, but to a rising consortium of resource-rich, market-hardened economies intent on securing global wealth under their own flags.

In population terms, the BRICS represent over 40% of humanity — a figure that jumps to an estimated 55.6% when the partner states, known as BRICS+, are included. This vast pool of labor, consumers and “trade war soldiers” forms the backbone of the bloc’s expanding economic power, ensuring that markets grow not only through trade, but also thanks to the demographic power that has always supported the great trading empires.

The Decline of the West

Anyone who has read a little history knows that the US and the West have not always had the upper hand in the global economy.

The “crown” has passed through more hands than a cheap bottle of wine: Mesopotamia, Egypt, Persia, Greece, Rome, China, the Caliphates, Portugal, Spain, the Netherlands, Britain… all took their turn on stage before retreating. Now the BRICS+ — Brazil, Russia, India, China and South Africa — are preparing for their moment.

And if history teaches us anything, it’s that someone is always preparing to sit in the driver’s seat and someone else is out. When the great powers start to fear the future, the scenario rarely changes — stagnation, misery and decline.

Ming China once believed it had achieved eternal perfection: it banned sea travel, scorned foreign trade, and replaced science with Confucian formalism. At the same time, Europe was stumbling across the New World and inventing commercial empires.

Fast forward to today, America seems to be “testing” for a re-release of the Ming — unable to finance its own infrastructure, allergic to global trade, and comfortable with the idea that being “number one” in the last century guarantees the same in the present. History shows otherwise.

Americans spent decades riding a 2% “growth bubble” — enough to quadruple living standards in a generation, but so slow that every five years feels like watching paint dry, interrupted only by random disasters.

Lose your job, the value of your home, or a government contract, and years of “progress” disappear. No wonder change feels threatening. In the United States, new technology means layoffs — encyclopedia salesmen, automakers, telephone giants, stockbrokers — one innovation at a time.

In modern China, the opposite is true: technology has been a golden escalator, moving almost everyone up so quickly that losing a job often means simply finding a better one.

The result? Americans see change as a wrecking ball; the Chinese see it as a construction crane.

Geopolitical weapons tariffs and the economy

On August 7, Donald Trump waved his magic wand of tariffs again, proving that tariffs are no longer just economic tools — but geopolitical weapons aimed at the BRICS and anyone who dares to say “no thanks.”

Apparently, the favorite pastime of the Washington swamp remains spreading chaos under the guise of a Malthusian depopulation agenda, while simultaneously bombarding the planet with new tariffs. As of midnight on August 8, the earth braced itself for a global minimum tariff of 10% on imports. The tariff on Canada was raised from 25% to 35%, Switzerland was hit harder, at 39%, provoking diplomatic backlash.

Meanwhile, 40 countries were slapped with a 15% hit, more than a dozen economies saw even steeper increases, and China and Mexico were given a 90-day “suspension of execution.”

Comply or be kicked out

The rise of BRICS+ was almost “predestined” by the Biden administration’s decision to kick Russia out of the SWIFT system — a clear message that the US is acting as the global financial dictator: comply or be kicked out.

The threat of the same fate for China if it helped Russia only accelerated the birth of BRICS as a geopolitical counterargument. The plan to bankrupt Russia through sanctions backfired spectacularly.

China unloaded American debt, and the Global South got the message — American financial hegemony is not just being exercised, it is being weaponized.

Meanwhile, Europe, the US, and allies kicked several Russian banks out of SWIFT in early 2022 — except for Gazprombank, because Europe still needed Russian gas.

The effort to isolate Russia only fueled a new economic bloc determined to break the stranglehold of the dollar — and rewrite the rules of the world order.

As holding dollar assets suddenly became a geopolitical headache, it’s no wonder that the BRICS countries began dumping US bonds faster than you can say “unreliable trading partner.”

(Chart: Holdings of US Treasuries — Russia [blue line]• China [red]• India [yellow]• Brazil [green]• South Africa [purple])

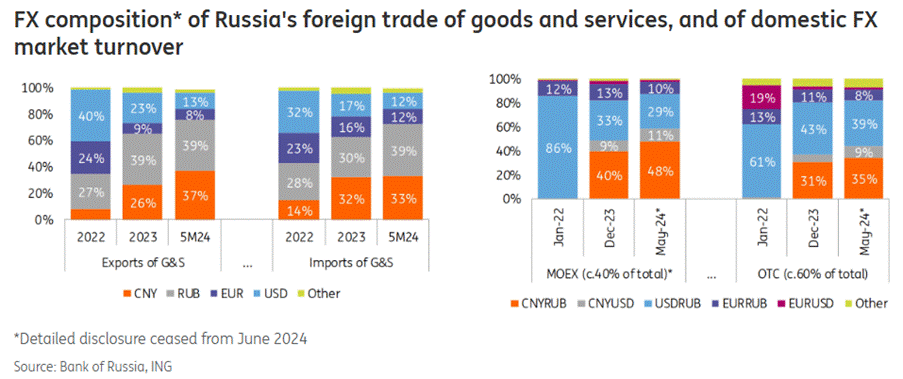

The dollar’s “rival” in BRICS+ foreign exchange reserves is essentially a “basket” of other developed-market currencies, which together account for 35% of the pie.

A key obstacle? BRICS+ countries hold just 6% of global external debt, compared to the US’s hefty 21%, making it difficult for their currencies to become truly global.

On the trade front, BRICS+ handle about 20%–21% of global trade — around $10 trillion annually — but growth has stalled since the financial crisis due to China’s slowdown and falling oil prices.

But the bloc’s members are expanding their ties with each other, with intra-BRICS trade rising from 22% in 2008 to 28% today, and emerging markets trading with them even more.

The real star is the fuel trade, which has doubled the BRICS+ share to 37%, making energy the main area for the dedollarization of global trade. With non-OECD oil demand now accounting for 55% of the global total, “who pays in what currency” matters.

While hard statistics are lacking, anecdotal reports suggest that renminbi, UAE dirham and rupee are widely used in energy deals. India now pays Russia in rubles and rupees. The Chinese yuan is the real heavyweight here — Russian foreign trade now prefers it over the dollar, thanks to the Bank of Russia hoarding yuan, which already makes up 22% of its foreign exchange reserves.

The m-Bridge trading system

When the BRICS talk about abandoning the dollar, the m-Bridge project often comes up — a sophisticated digital money “road” led by the Bank for International Settlements (BIS) and the central banks of China, Hong Kong, the United Arab Emirates, and Thailand.

It uses CBDCs (central bank digital currencies) to make large cross-border payments faster, cheaper, and seamless.

Bypassing the traditional banking network — which often routes payments through the dollar and the labyrinth of US banks’ SWIFT — m-Bridge is trying to reduce reliance on the dollar in global trade.

The technology works, but will it get all the banks and regulators to agree and cooperate? That’s the real challenge. After three years, they’ve only just released a basic version.

So yes, m-Bridge could one day challenge the dollar’s throne — the revolution is brewing, but it’s moving slowly.

First, the BRICS are not signing up to the globalized project that the West has been pushing since World War II.

Second, everyone has seen how the euro has become a headache that undermines national sovereignty, with debt defaults looming across Europe.

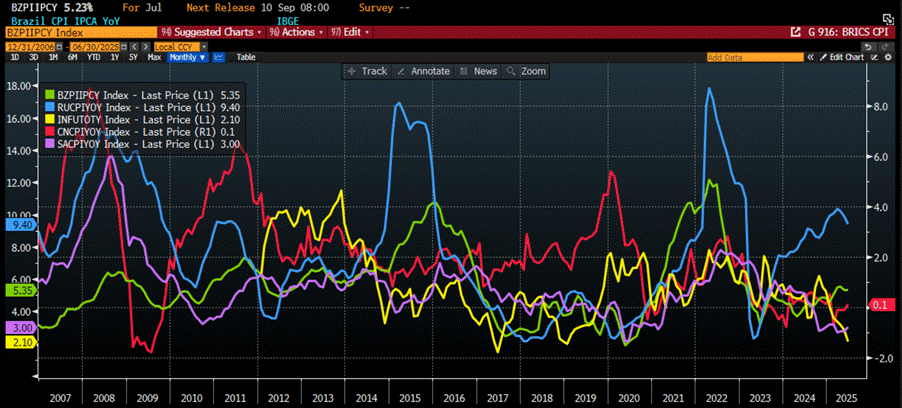

Third, they are not moving in sync — China has been stuck in deflation since the COVID health crisis, while Brazil and India are struggling with persistent inflation, and are trying to lower the exchange rate for their currencies against the dollar and manage debt.

So yes, a single BRICS currency will emerge soon.

Chart: CPI inflation change year-on-year in Russia (blue line), China (red line); India (yellow line); Brazil (green line); South Africa (purple line).

The Chinese Dragon’s Path

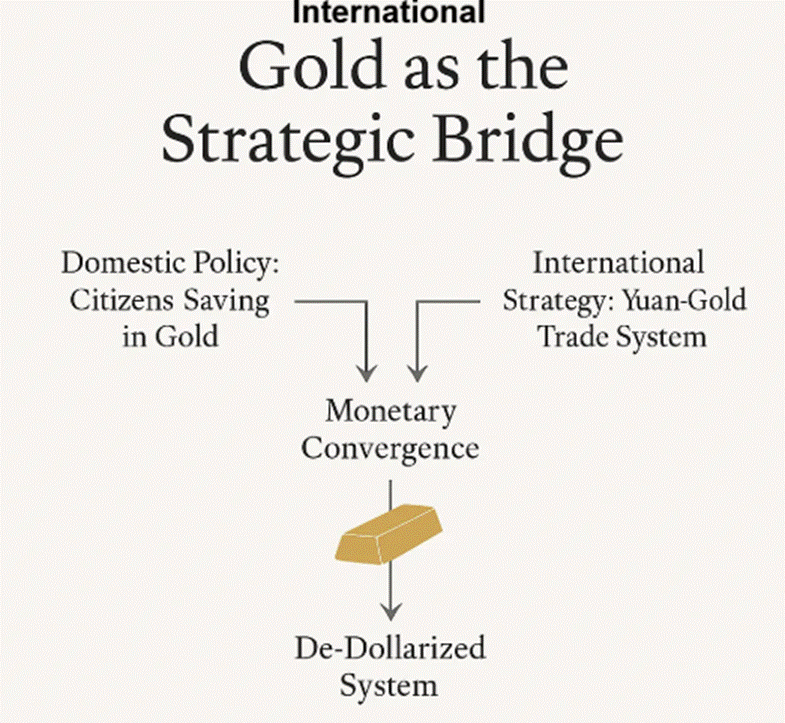

Instead of pushing for a BRICS currency or simply adopting the yuan as the new reserve currency, China’s leaders, who understand the headache of owning the world’s reserve currency, are quietly guiding the people and government away from the dollar.

Citizens are encouraged to buy gold, while the state builds a parallel system of trade and finance that completely bypasses the dollar.

The plan? Two separate paths that converge: a domestic savings base backed by gold meets an external trading engine backed by the yuan, creating a new, stable financial medium.

Unlike the United States, China is aligning its goals with the interests of its people. It is promoting the yuan for trade with countries participating in the Belt and Road Initiative, while promoting gold savings at home.

Internationally, gold acts as collateral for partners that accept the yuan.

The combination of gold and yuan forms a bridge between national ambitions and global trade.

The BRICS countries are being encouraged to move towards a yuan-based monetary system: sell raw materials, pay in yuan, and then buy finished goods from China — closing the loop.

If the plan succeeds, China will issue yuan-denominated bonds to foreigners, paying interest linked to the value of gold as a hedge against currency depreciation.

Bretton Woods II, the Beijing Consensus, and the Gold Standard

Let’s think about Bretton Woods II: the world on the gold-backed dollar standard.

Bretton Woods 3 is about the BRICS adopting the gold-backed yuan standard. It’s essentially a reboot of what the US did after World War II — building economies and influence, tying the world to a currency that was backed by gold.

But what is China’s modification?

No fixed price and decentralized storage of precious metal.

Smart moves to avoid the mistakes that led to Bretton Woods II.

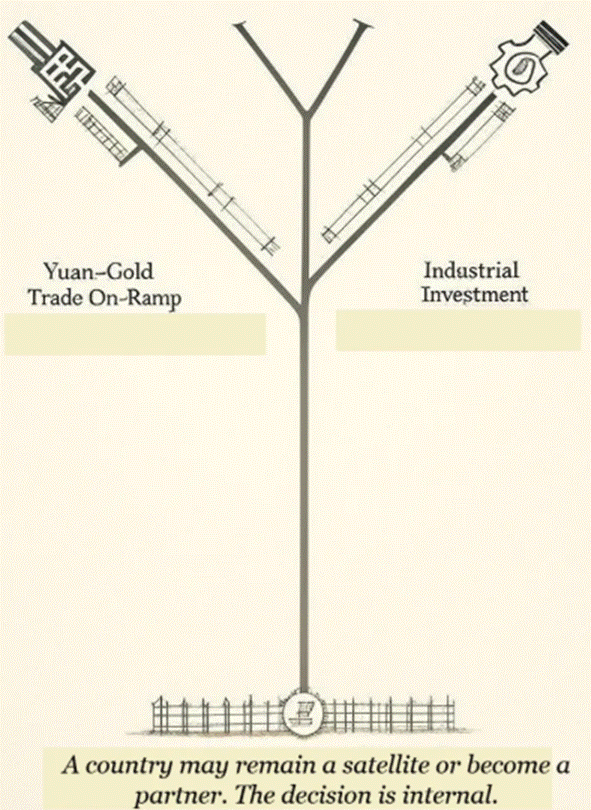

The BRICS countries will be able to peg their currencies to gold, the yuan, or whatever suits them.

The yuan acts as a medium of exchange, while gold acts as an absolute store of value.

The design of the system encourages countries to follow two paths: invest in your economy and watch your currency strengthen, or continue to export raw materials and become an economic satellite of China.

It will probably be voluntary — but let’s not kid ourselves, the pressure is real.

Build your industry, and China becomes your partner: infrastructure, goods, investment, the whole package.

Ignore it, and you remain dependent, just as the US rebuilt Germany and Japan after World War II — but now China is the one financing and caring.

China is playing the long game at home, too

It’s allowing citizens to buy gold, offering gold-linked savings accounts and promoting gold-backed investment products.

Next step? Gold-backed bonds.The goal: to build trust in the financial system — and reward that trust with substantial returns. As long as the U.S. is seen as a threat and the Chinese government makes no mistakes, trust will continue to grow. Internationally, China is opening its bond market to foreign holders of yuan, with returns tied to gold to hedge against currency risk.

The cycle is simple: sell resources for yuan, rely on gold as a safety net, invest in Chinese bonds, buy Chinese goods. Sound familiar?

It’s essentially the new Marshall Plan 2.0 after the end of World War II.

China is also smart about keeping highly profitable industries at home, selling finished goods abroad, and controlling the transfer of value in the supply chain — not just raw materials.

Gold is the glue: it reassures other countries, keeps people loyal at home, and steady the ship as the dollar declines.

Ultimately, the plan is to move from gold to the yuan once the yuan gains enough confidence — and perhaps abandon gold when the time is right. Remember, China invented abstract paper money and had markets before capitalism even existed — it’s not playing dumb.

This is not some secret plan — history repeats itself. Big changes in the financial system follow wars.

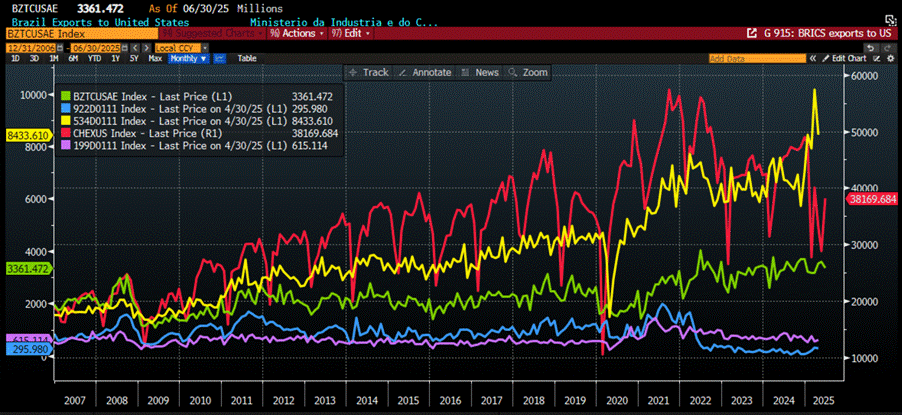

Today’s battleground? Trade deals, savings, and bonds. The plan is underway. The BRICS didn’t exactly wait for Donald Trump to throw additional tariffs like confetti before they started to reduce their love for US bonds. No, they started ignoring Uncle Sam’s trade as early as 2018, during the first act of Trump’s first term. They probably saw the “tariff magic” coming and decided to disappear early!

Exports from Russia (blue line); China (red line), India (yellow line), Brazil (green line), South Africa (purple line) to the USA.

For all the Western “China experts” who have never set foot there and are writing from their cozy Texas offices: stop obsessing over China’s real estate crisis as if it were the apocalypse.

Unlike the US, Chinese companies rely on bank loans — not volatile stock markets — for growth.

Since 2019, Beijing has shifted financing from real estate to high-tech industries like EVs, AI, and mechanical equipment, creating global players like BYD, Huawei, and Zoomlion that are crushing Western competitors on price and quality.

Meanwhile, the “real estate crisis” that supposedly dooms China?

Beijing isn’t batting an eye — the Chinese have homes, the banks are state-controlled, and the government is preparing for an industrial Blitzkrieg. The Western world, by contrast, is still waiting for the Germans to cross the Maginot Line, to forget the… follies of the “green deal,” while China is advancing at a rapid pace.

The Russia-China-India Axis

Despite their lack of centralized power, the BRICS+ undoubtedly rely on the rise of the Russia-China-India triple axis — combining Russia’s vast, cheap natural resources, China’s advanced manufacturing know-how, and India’s growing, hungry consumer market.

Together, they form a mercantilist superpower that is reshaping the global economic game. In the first half of 2025, China’s exports tell a story: the Global South is now the hottest market, while the West is left out.

ASEAN leads with $322.5 billion in imports, Africa’s exports increased by $21.4 billion, India’s buying power increased by $14 billion, and Latin America kept pace with $7.3 billion more. Meanwhile, the US and Western Europe look… in decline

China is clearly hedging its bets, filtering out less demanding partners in the Global South to avoid the West’s tantrums.

Smart geopolitical move — less drama, more diverse shopping baskets. It seems the future of Chinese exports is not Wall Street, but Main Street… somewhere near the equator.

While reducing trade with the US and even Europe, the BRICS+ countries are getting closer to each other and increasing trade with each other. Take India’s love affair with Russian oil: imports have skyrocketed from 68,000 barrels per day before the use of the dollar as a weapon to over 2 million — why pay full price when you can get a discount?

Nearly 40% of India’s crude now comes from Russia, $10–20 cheaper per barrel than Middle Eastern oil.

Meanwhile, US-India trade is $118 billion, with a $45 billion deficit for the US — so yes, bring on the tariffs and job threats, but India is still smiling.

China is still consuming Russian oil, and other Asian exporters can’t fill the gap. Sanctions by the G7 and the EU may have shifted oil flows, but they have not affected global supply or demand, especially not in India.

A popular narrative among Western warmongers is that India imports Russian oil only to refine it and export petroleum products. The facts say otherwise: India’s petroleum product exports today are about the same as they were in 2019 — long before Russia launched its invasion of Ukraine.

Another myth is that only private Indian companies import Russian crude. No — both private and state-owned refineries have been loading Russian oil since the invasion of Ukraine.

Reliance Industries (RIL) accounts for about 1/3 of imports, IOC 16%, BPCL 12%, ONGC 8% and its subsidiary HPCL 5%, while Nayara and HMEL add 15% and 10% respectively.

Another example of BRICS mercantilism is the restructuring of the coffee supply chain between China and Brazil, following Donald Trump’s tariffs. After imposing 50% tariffs on Brazil’s major exports, China is rushing to support Brazil’s coffee industry, granting licenses to 183 new companies for five years.

President Lula calls on his BRICS friends — Xi Jinping, Modi, and Putin. Foreign Minister Wang Yi denounces the US tariffs as bullying, a violation of UN and World Trade rules, and has pledged cooperation with allies in the Global South.

Return to the Land

In modern times, the US has tried to contain China to its island chains, but the dragon digs the land. With the Belt and Road Initiative, China is building railways, pouring concrete, and laying fiber optics, creating a web of influence that reaches from the heart of China to its distant shores.

After Russia’s invasion of Ukraine in 2022, the West went all-in on sanctions: no dollars, no euros, no SWIFT, no tank parts, no chips, no champagne at Davos. Russia responded: focus on land instead of sea, using its rivers — Volga, Don, Ob, Lena — connecting them with ports, roads, and railways to create a Eurasian trade artery that bypasses the Western seas.

When the river meets the mountain, they both find their way: China brings wealth and vision, Russia brings land and resources.

Together they weave roads, railways and rivers into a web that the seas cannot touch, forming a trade beyond shipping and sanctions. Simply put, the BRICS+ are doing what economic theory teaches: exploiting their comparative advantages and trading smartly.

The Gold Rush

Since 2022, they have been buying gold, now owning over 20% of the world’s gold. The second quarter of 2025 shows a 41% increase in gold purchases as they move away from the dollar and pursue financial freedom. Russia and China hold almost three-quarters of BRICS reserves.

With more than 10 new members in 2025, the BRICS are turning the global economic game into a multipolar one. Even India is getting in on the act, adding 19.2 tons last year — when money loses its value, the shiny metal is a safe bet.

Gold reserves in troy ounces in Russia (blue), China (red), India (yellow), Brazil (green), South Africa (purple).

The BRICS and their new members are piling up gold while moving away from U.S. Treasuries, and few in the West realize that they are also sitting on some of the largest gold deposits on the planet — top gold producers, too.

From a geopolitical perspective, China is making it clear: Russia will not lose, because then it may be their turn. The only defense against the steely Neocons is a united front — Russia, China, India and others against the West.

India and China once dominated global financial markets, while Europe lost its primacy after two world wars.

Lessons from the Bankruptcy of the French Empire

War is the quickest way to bankrupt an empire, and the history of France is a textbook example. Donald Trump seems poised to repeat this cycle.

Beginning in 1558, Henry II spent all his resources fighting the Habsburg and Valois dynasties before going bankrupt.

In 1648, the young Louis XIV borrowed uncontrollably during the Thirty Years’ War (1618–1648) and the Franco-Spanish Wars (1635 to 1659), suspending payments and manipulating the currency.

In 1661, a scandal erupted when the French Finance Minister Fouquet was arrested for embezzlement, while the debt continued to grow.

Finally, after the War of the Spanish Succession in 1715, France went bankrupt again, pretending that some debts did not exist.

History shows that war and debt are inseparable, and empires always pay the price.

As the world marches toward World War III, history gives a clear warning: war triggers

stagflation,

inflationary crashes,

and government intervention in the economy that pushes nations toward bankruptcy — a battle that has already been raging this decade as bondholders lose value.

Decades of wasteful spending and currency distortion have brought the West to the brink of collapse.

Donald Trump’s Big Beautiful Bill is just another episode in a series of increasing public spending and denying reality.

Bond markets — not stocks — are sounding the alarm: rising yields, synchronized selling, and shadowy buyers reveal a system that is losing trust. In the background, the US is already quietly bankrupting itself through inflation.

Yet many still worship supposedly “risk-free” U.S. Treasuries, ignoring that since 1971, the bonds have fueled a $300 trillion debt monster while all the gold in the world is worth only $22 trillion.

The real question: do you trust the paper promises of politicians or centuries of real value?

At the end of the day, empires tend to commit suicide in three acts:

Reckless fiscal mismanagement that fuels inflation to cover the debt.

When loans dry up, they impose political tyranny at home and blame an external “enemy” — this time, Putin.

The third door opens — bankruptcy, government collapse, and a new regime restructures old debts.

Classic economic tragedy, same script, different cast, and we’ve just entered phase 2.

In this context, the path to real prosperity remains paved with intangible assets, not fragile IOUs or digital tokens.

Physical gold and silver are the ultimate hedges against intense uncertainty. Beyond precious metals, commodities protect against the collapse of the global supply chain.

Let us never forget: