The indications to date for the euro area economy raise reasonable concerns, increasingly removing the scenario for a recovery of its V-shaped economy and increasingly approaching the scenario of slow and uneven K-shaped growth.

At the same time, the governments of the euro area member countries are particularly concerned about the further recession that the new waves of the pandemic Covid-19 can cause with the upcoming general lockdowns in their societies and economies. That is why they are trying to impose local and individual lockdowns rather than generalised on the whole country.

by Thanos S. Chonthrogiannis-https://trusteconomics.eu ©The law of intellectual property is prohibited in any way unlawful use/appropriation of this article, with heavy civil and criminal penalties for the infringer.

Concerns about the euro area economy

Concern about the development of the recovery in the European economy is based on two main axes:

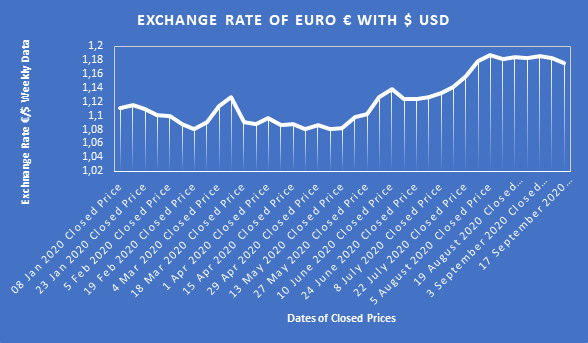

1. The €-euro is constantly valued against the US dollar

More specifically, the appreciation of the euro is in the order of 11% since the outbreak of the pandemic (March 2020 – until now 17 September, 2020) (please see below the Chart 1) and theforcedimpositionofthefirstgeneralised lockdowns on theeuroareaeconomyandsocieties.

This makes euro area products less competitive (more expensive) in the world’s markets, making any expected growth in its member countries even more difficult. In part, this continued appreciation of the Euro is based on the aggressively loose monetary policy implemented by the FED in order to support the recovery or containment of the recession from the pandemic in the American economy as well as the informal “financing” of the USA trade war against China and the artificial trade war between the US and the EU.

On the other hand, the scope for the ECB to “fight back” with even looser monetary policy is extremely limited to non-existent. The ECB’s current basic euro borrowing rate stands at 0.5% while the ECB has already drawn up a giant fiscal and quantitative stimulus package together with the EU Commission totaling €1,35trn to deal with the recession caused by pandemic response measures.

2. The emergence of Deflation (or negative inflation) in the Eurozone

The Eurozone for the first time in the last four years has entered a state of negative inflation. According to the data of the Eurostat HICP (2015=100)-monthly rate of change, https://appsso. eurostat.ec.europa.eu/nui/show.do?dataset=prc_hcip_mmor&lang=en, 27/09/2020) the hard core of inflation – not including energy, food, and tobacco products – fell to 0.4% in July and August, respectively. In addition, there is deflation in 12 of the 19-euro area member countries.

Under the Maastricht Treaty, the ECB’s main objective is with its monetary policy to keep euro area inflation below 2% per year in order to make the economy work better and to facilitate the management of public debt by the governments of the euro area member countries. For the two years 2021-2022 we forecast inflation of 1.1%-1.2% for the eurozone economy.

This is where the second factor comes in, negative inflation, which is further reinforced by the continued appreciation of the euro and at the same time makes the growth of the euro area economy problematic. The picture now created for the euro area economy is characterised by three main factors:

1. Appreciation of € versus $ USD

Consequence: It hampers exports and a rapid economic recovery.

2. Deflation from July 2020 onwards

Consequence: Long-term management of public debt for the governments of euro area member countries is exceedingly difficult.

3. Prolonged duration of negative interest rates for the euro Consequence: It creates a deep recession or very weak growth economy that will lead to Japan’s similar lost decades with exceptionally low interest rates (1990-present).

Our proposal to break the deadlock in the Eurozone

For the “unblocking” of the euro area economy by this “deadly tanks” (deflation, appreciation € vs. $ USD, negative interest rates) the Trust Economics believes that the key to the recovery of the economy is a new Financial Stability Pact (Table 1) in which all euro area member countries will have to agree that their central/federal governments have an annual total of public spending in their state budgets that will never exceed 15% of their GDP with 4% of their GDP per year directed to salaries and pensions of civil servants.

| Eurozone member-countries | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 |

| Euroarea 19 countries | 23,9 | 23,3 | 22,7 | 22,4 | 22,1 | 21,7 | 21,6 |

| Belgium | 31,8 | 38,9 | 27,6 | 27,4 | 26,6 | 26,6 | 26,8 |

| Germany | 13,3 | 12,7 | 12,5 | 12,5 | 12,7 | 12,6 | 12,6 |

| Estonia | 32,1 | 32,2 | 34,1 | 34,1 | 33,6 | 34,0 | 33,8 |

| Ireland | 38,5 | 35,9 | 27,9 | 26,5 | 24,9 | 24,1 | 23,4 |

| Greece | 52,1 | 38,8 | 41,2 | 37,7 | 36,8 | 35,8 | 33,9 |

| Spain | 22,8 | 21,9 | 20,7 | 19,8 | 18,8 | 19,1 | 18,7 |

| France | 23,3 | 23,2 | 23,1 | 23,4 | 23,4 | 22,6 | 22,5 |

| Italy | 30,8 | 30,9 | 30,8 | 30,8 | 30,4 | 29,8 | 29,4 |

| Cyprus | 34,2 | 39,9 | 31,8 | 28,5 | 28,3 | 35,8 | 30,7 |

| Latvia | 21,8 | 23,1 | 23,5 | 21,9 | 22,7 | 23,4 | 23,3 |

| Lithuania | 23,9 | 22,9 | 24,1 | 22,9 | 21,8 | 30,3 | 25,9 |

| Luxembourg | 31,6 | 30,6 | 30,3 | 29,7 | 30,3 | 30,4 | 30,7 |

| Malta | 41,7 | 40,9 | 39,5 | 36,5 | 35,9 | 36,6 | 37,6 |

| Netherlands | 26,4 | 26,3 | 26,8 | 26,4 | 25,4 | 25,4 | 25,8 |

| Austria | 34,8 | 35,5 | 34,2 | 33,1 | 32,2 | 31,5 | 30,9 |

| Portugal | 37,3 | 39,6 | 36,6 | 33,7 | 34,2 | 31,8 | 31,3 |

| Slovenia | 41,5 | 32,7 | 31,2 | 28,5 | 26,4 | 25,6 | 25,7 |

| Slovakia | 27,2 | 27,8 | 30,1 | 27,0 | 25,6 | 25,9 | 26,6 |

| Finland | 28,4 | 28,4 | 27,6 | 27,3 | 26,4 | 25,9 | 25,7 |

This treaty alone will cause a large wave of privatisation of public enterprises and organisations in most member countries, respectively.

This treaty alone will cause a large wave of privatisation of public enterprises and organisations in most member countries, respectively.

In this case, the funds to be released should be directed, through the application of equivalent budgetary measures, towards reducing, mainly, indirect and secondary direct taxation, in order to drastically increase the income available for consumption of citizens with a view to drastically increasing both their consumption and their savings.

| Eurozone member-countries | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 |

| Euroarea 19 countries | 8,9 | 8,3 | 7,7 | 7,4 | 7,1 | 6,7 | 6,6 |

| Belgium | 16,8 | 23,9 | 12,6 | 12,4 | 11,6 | 11,6 | 11,8 |

| Germany | -1,7 | -2,3 | -2,5 | -2,5 | -2,3 | -2,4 | -2,4 |

| Estonia | 17,1 | 17,2 | 19,1 | 19,1 | 18,6 | 19,0 | 18,8 |

| Ireland | 23,5 | 20,9 | 12,9 | 11,5 | 9,9 | 9,1 | 8,4 |

| Greece | 37,1 | 23,8 | 26,2 | 22,7 | 21,8 | 20,8 | 18,9 |

| Spain | 7,8 | 6,9 | 5,7 | 4,8 | 3,8 | 4,1 | 3,7 |

| France | 8,3 | 8,2 | 8,1 | 8,4 | 8,4 | 7,6 | 7,5 |

| Italy | 15,8 | 15,9 | 15,8 | 15,8 | 15,4 | 14,8 | 14,4 |

| Cyprus | 19,2 | 24,9 | 16,8 | 13,5 | 13,3 | 20,8 | 15,7 |

| Latvia | 6,8 | 8,1 | 8,5 | 6,9 | 7,7 | 8,4 | 8,3 |

| Lithuania | 8,9 | 7,9 | 9,1 | 7,9 | 6,8 | 15,3 | 10,9 |

| Luxembourg | 16,6 | 15,6 | 15,3 | 14,7 | 15,3 | 15,4 | 15,7 |

| Malta | 26,7 | 25,9 | 24,5 | 21,5 | 20,9 | 21,6 | 22,6 |

| Netherlands | 11,4 | 11,3 | 11,8 | 11,4 | 10,4 | 10,4 | 10,8 |

| Austria | 19,8 | 20,5 | 19,2 | 18,1 | 17,2 | 16,5 | 15,9 |

| Portugal | 22,3 | 24,6 | 21,6 | 18,7 | 19,2 | 16,8 | 16,3 |

| Slovenia | 26,5 | 17,7 | 16,2 | 13,5 | 11,4 | 10,6 | 10,7 |

| Slovakia | 12,2 | 12,8 | 15,1 | 12,0 | 10,6 | 10,9 | 11,6 |

| Finland | 13,4 | 13,4 | 12,6 | 12,3 | 11,4 | 10,9 | 10,7 |

Table 2 = (Data Table 1 – 15%)

The corresponding size of annual funds would be released if Eurozone had to implie the proposed Stability Fiscal Pact which would oblige the Central governments of eurozone member-countries to implement the fiscal rule 15% of GDP annual expenditures in their annual state Budgets

Data Period (2013-2019),

Notes Table 2: The minus (-) sign in case of Germany means that the Central (Federal) government of Germany would had to pop up its annual spending to achieve the annual limit of 15% of GDP.

This annual released of Funds would allow the EU Commission to impose a common Eurozone tax and implement a common fiscal and tax policy across the Eurozone.

The ECB President’s initiative to permanentise the European Recovery Fund, which from 2021 onwards will have to provide €750bn with aim to support the economies of euro area member countries, is wrong because it is as if the EU is making fun of capital markets by taking on debt that does not count and by increasing the public debt of the Eurozone/EU government.

In addition, it has not been clarified how the proceeds will be collected to repay the €750bn loan from capital markets.