The Picture Behind the Stock Market Rise and the Strait of Hormuz

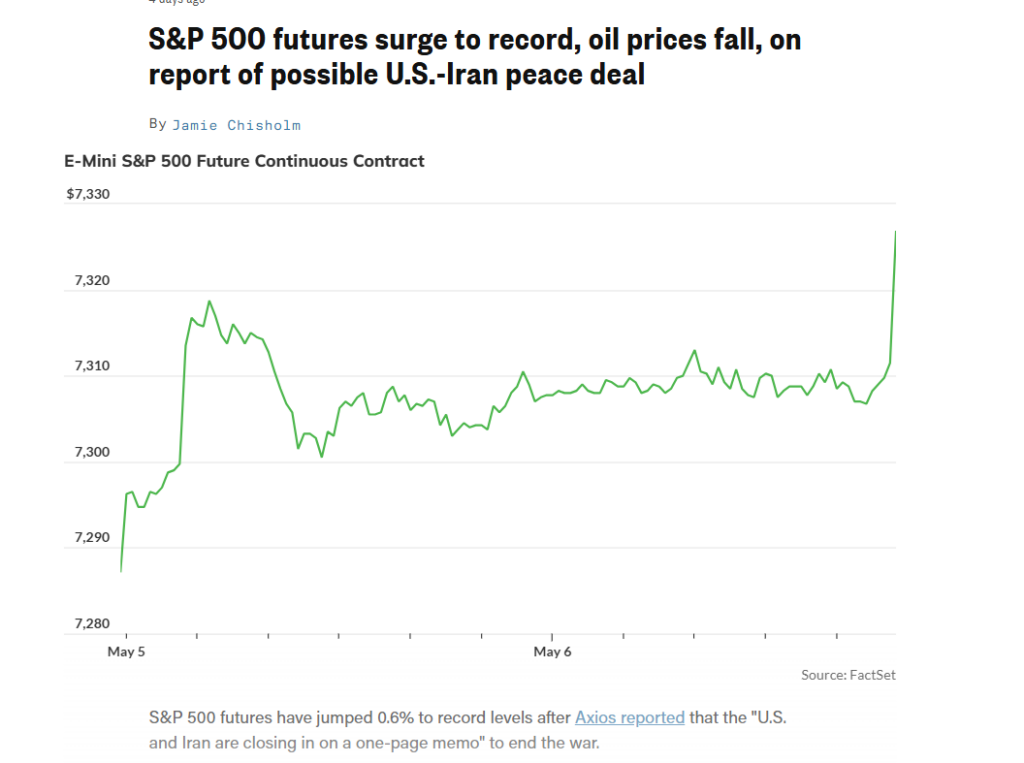

On February 28, the United States and Israel launched joint airstrikes against Iran. Iran closed the Strait of Hormuz, and over the next five weeks the S&P 500 fell nearly 9%. Hedge funds sold at the fastest pace in 13 years. Total leverage exceeded 300%, near an all-time high. Short exposure in macro ETFs reached levels not seen since the pandemic. The mood on Wall Street was not just pessimistic, it was reminiscent of October, Black Monday-Tuesday, 1929. Everyone in the market knew that a prolonged closure of the Straits of Hormuz without alternative pipelines would force the world to lose 15 million barrels of daily demand.

- On Wall Street — the world of stock indexes and ticker symbols — prices are at historic highs.

- On Main Street — the world of growth forecasts, consumer spending, and hiring — forecasts are being revised downward.

The Vicious Cycle as Political Cover

What makes President Trump’s political narrative resilient is that the market to which Trump refers has quietly transformed into something that most Americans no longer recognize as the institution they once trusted. The stock market of a generation ago functioned, at least in theory, as a collective judge of the health of the broader economy. Today, that market has largely been replaced by a system where more than $13 trillion moves automatically with fintech through passive index funds. In this new landscape, giant trading firms buy and sell based on programmed numerical limits rather than fundamental economic analysis. Perhaps most importantly, the AI and semiconductor giants that now dominate the indices operate in a growth cycle that is structurally disconnected from traditional indicators like energy prices, consumer confidence, or the cost of filling up a gas tank. When a company like Nvidia does well, the S&P 500 goes up—and that’s true whether gas is $2.50 or $4.50. This disconnect is precisely what makes the stock market so useful as a political tool right now. A president can stand on the podium and point to a number that reflects the health of the AI economy, the automatic liquidation of short positions, and the strength of Asian semiconductor stocks—and present it as proof that managing a war in the Middle East is paying off. He thinks he’s selling “mirrors” to the natives.

A Gallon of Gas vs. an Investment Portfolio – The Two Americas

This observation brings us back to President Trump’s press conference and the response that deserved far more attention than it received. The gas pump and the investment portfolio are now telling two very different stories to two very different groups of Americans. While a stock market at an all-time high is technically “good news,” the benefit is severely limited. It affects the roughly 58% of Americans who own stocks and disproportionately favors the wealthiest households, who hold the vast majority of that wealth. Gas at $4.50 a gallon is news to everyone, but it hits hardest those who spend most of their income on transportation and energy — those who are less likely to have an investment account that benefited from an $86 billion mechanical buying spree. Trump’s response on May 7 is his new argument, one he will repeat many more times to avoid discussing gas prices. He will try to shift attention from the number that pressures his voters at the pump to the number that flatters his political legacy, the stock ticker. Answering the reporter’s question honestly would require a level of transparency that the government has been unwilling to provide. It would mean admitting that gasoline prices remain high because the Strait of Hormuz remains effectively closed and because the Strategic Petroleum Reserve has been depleted to historic lows. More importantly, it would require acknowledging that the stock market’s all-time highs did not come from faith in a resolution to the Iran crisis. Instead, they were the result of a mechanical “short squeeze” — the aggressive liquidation of the most extreme bets that Wall Street had placed against the market since the pandemic. A “short squeeze” is a stock market phenomenon in which investors who had bet on a stock or market falling are suddenly forced to buy back their positions, causing prices to rise even further. That answer was never given. And it is precisely this gap — the gap between what was said and what actually happened — that is the most important economic story happening in Washington right now. And that’s why President Trump’s popularity will continue to collapse.Please follow and like us: