In the Strait of Hormuz, the traditional power of the dollar is collapsing in the face of Tehran’s resilience and the new geopolitical balances.

Meanwhile, eight indices reveal how the US’s most important economic weapon has lost its effectiveness, signaling the end of an era of undisputed hegemony.

In particular, as OPEC members have long understood, it is not a good idea to give users of your product an incentive to seek alternatives.

There is an old central banker’s maxim that seems to have broad application in today’s geopolitical situation. As quoted in David Kynaston’s history of the Bank of England, it says: “Wave the big stick if you like, but never use it; it may break in your hand. Better yet, try wiggling your finger.”

Among the many consequences of the confrontation in the Strait of Hormuz, it seems that we may remember this period as the moment when one of America’s most powerful geopolitical tools proved to be a weakened stick.

The threat of restricting access to the global dollar system now seems less daunting. We saw the first signs of this as early as 2022, when Russian banks were sanctioned and disconnected from SWIFT for international bank payments. Even then, it was understandable that this would likely be more of an inconvenience than an economic death sentence.

But the fact that Russia has continued to wage war and sell oil to finance itself must have disappointed supporters of sanctions. The ineffectiveness of the “weaponized” dollar in the Gulf is also telling. Iran is one of the most heavily sanctioned places in the world; it is one of the few cases where US Treasury sanctions cover an entire country rather than specific entities and individuals.

However, not only does this not seem to have stopped it from selling oil while at odds with the United States, it has also not stopped it from effectively imposing “ransoms” on international shipping seeking to pass through the Strait of Hormuz.

Some ships have paid Iran as much as $2 million to secure safe passage, according to Lloyd’s List Intelligence.

And following news of a ceasefire between the United States and Iran, an Iranian official suggested that his country would require shipping companies to pay cryptocurrency tolls for tankers, equivalent to $1 per barrel of oil transported.

Part of the problem is that being cut off from the dominant global payments system is only a threat because the dollar economy is so convenient and profitable.

This means that the “weapon” is most effective against open economies that are embedded in global supply chains.

But these are rarely the countries worth threatening. In contrast, states under sanctions tend to get by and find ways to work with willing partners.

Iran can sell at least some of its oil in exchange for renminbi, especially since most of its imports come from China.

There is also a network of banks and “shadow” financial companies that, according to the Atlantic Council, are willing to take on the risk of offshore enforcement of US sanctions and “launder” payments in dollars.

Such counterparties are less concerned about their access to New York’s dollar clearing system. But these workarounds may be almost unnecessary in a world where anonymous money can be sent over the internet.

The United States does not control the flow of payments made in Bitcoin or stablecoins (cryptocurrencies tied to real assets like the dollar) that are traded over decentralized networks.

While strict compliance with American anti-money laundering rules continues to cause problems for US allies, countries at odds with America have a separate and poorly regulated parallel “crypto-dollar” for use, as do criminals and other malicious actors.

As Gulf states have learned since OPEC’s founding, it’s not a good idea to give users of your product an incentive to seek alternatives. All of this was entirely predictable.

In fact, Henry Farrell, one of the political scientists who coined the term “weaponized interdependence,” predicted it.

Having been a source of global stability for so long, the dollar system has become a source of instability as it has become more “weaponized.”

As we have noted: “As the United States increases pressure, other countries will seek to escape the power of the dollar, likely provoking the United States to further intensify its response.”

This is not without consequences, as North Korea’s isolation from the mainstream global financial system has shown.

Targeted sanctions on individuals appear to be more effective than general sanctions on countries. “Malicious actors” who are excluded from the dollar banking system are still forced to turn to inferior alternatives, such as cryptocurrency payment technologies.

However, rather than being a geopolitical weapon for the United States, global finance is arguably a power multiplier for its adversaries.

As David Kynaston’s central bankers knew, it is far better to threaten serious consequences than to find yourself in a position where you actually have to use the “big stick.” It might break.

The 8 Indicators You Can’t Ignore

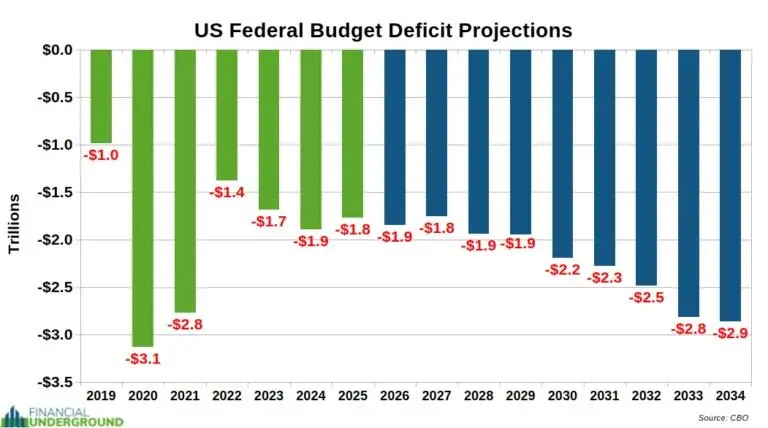

Indicator 1: US Deficits

The chart below shows the actual and projected federal budget deficits.

It is important to note that these projections are based on the ridiculous assumption that there will be no wars, recessions, or other events that will increase federal spending. This assumption has already been shattered with the Iran war: the Pentagon requested an additional $200 billion, for starters.

Even with this optimistic and unrealistic projection, the U.S. government is projected to run a total deficit of over $22 trillion over the next decade — deficits that will have to be financed by issuing more debt, much of which will likely be purchased by the Federal Reserve with “money” it creates out of thin air.

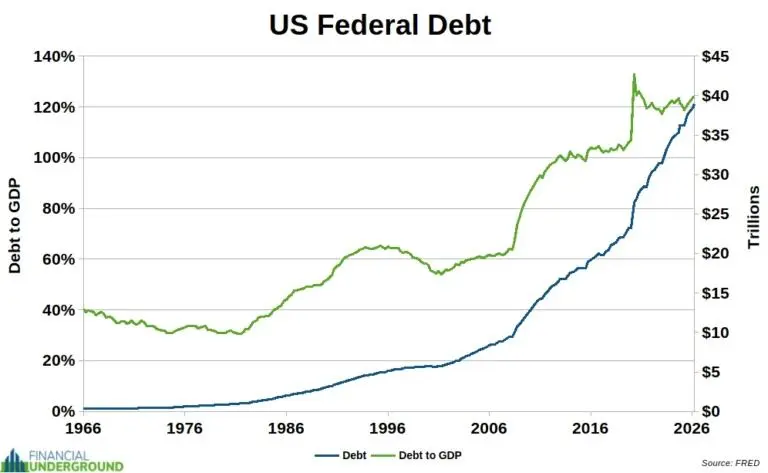

Indicator 2: Debt

Federal debt has surpassed $39 trillion, representing over 124% of GDP.

It’s important to remember that GDP is a flawed statistic. For example, it counts government spending as a positive. A more honest measure would count it as a major negative, as it exacerbates the debt cycle.

In the United States, government spending accounts for at least 37% of GDP. In other words, the debt-to-productive economy is much larger than the official figures indicate.

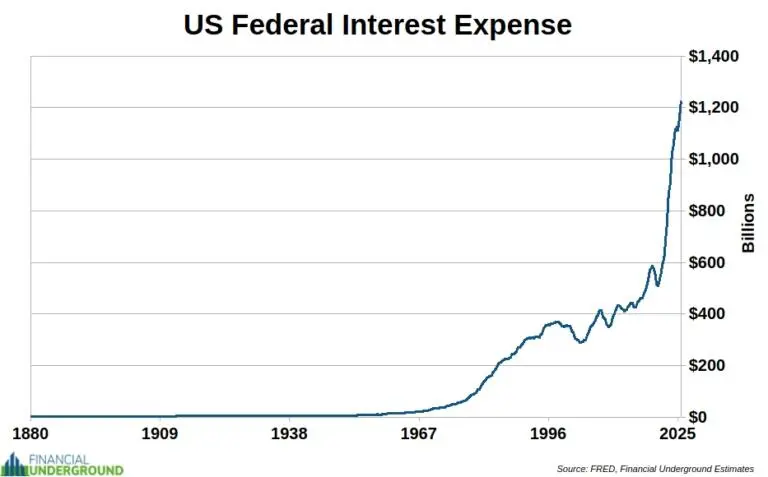

Indicator 3: Interest Expenses

The annual interest on the federal debt is over $1.2 trillion and rising.

This means that over 23% of the government’s tax revenue goes to servicing the interest on the existing debt alone. Interest costs are already the second largest expense of the U.S. government and are expected to surpass Social Security to become the largest federal expense within a few months.

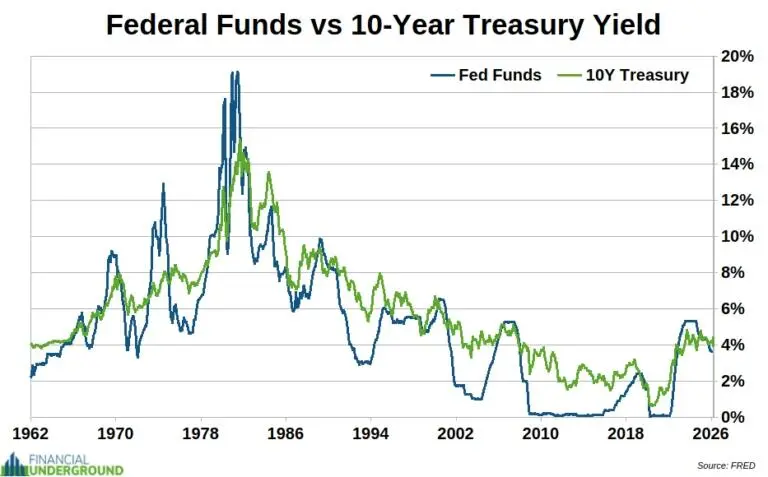

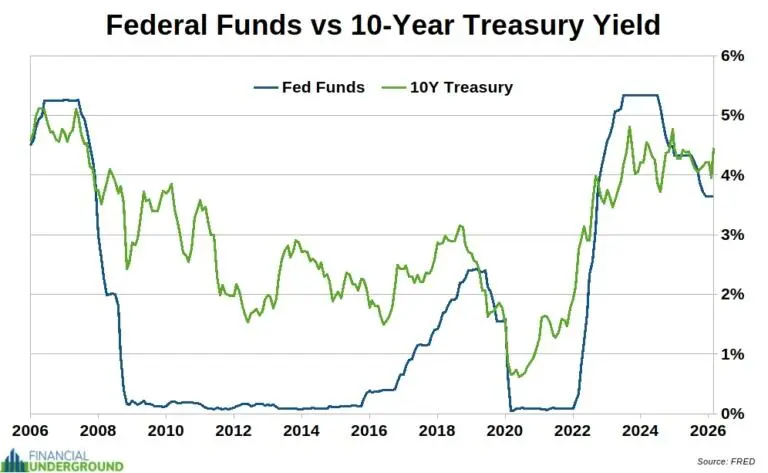

Indicator 4: Federal Funds Rate and 10-Year Treasury Yield

Whenever we discuss the Fed or central banks, it is essential to remember the basics. We must start with the most fundamental concept: central planning does not work. That is the first foundation.

Central planning of shoes does not work.

Central planning of wheat does not work.

And central planning of (counterfeit) money does not work.

Central banks in general—and the Fed in particular—are on a mission impossible. They don’t know what the interest rate should be. Nobody knows. Only a voluntary market of savers and borrowers, using honest money, can determine that.

A politburo can’t centrally program interest rates any more than it can program potatoes. They inevitably fail — and cause significant damage in the process.

Also, central banks have nothing to do with the free market; they are its opposite. In Karl Marx’s Communist Manifesto, central banking is the fifth column.

With that in mind, note the following: After the 2008 financial crisis, the Fed brought interest rates down to around 0% and kept them there for years. Then, in late 2015, a cycle of rate hikes began that lasted until the repo market turmoil in late 2019.

After the Covid outbreak in early 2020, the Fed brought rates back to 0%. Inflationary pressures reached 40-year highs in 2022, forcing the Fed into another round of rate hikes, one of the steepest in history.

In just 18 months, the Fed raised rates from around 0% to over 5%. Now, the Fed is back to easing and cutting rates without having beaten inflation. The Fed effectively controls short-term interest rates, such as the Federal Funds rate, which is the rate at which banks borrow from each other overnight.

Long-term interest rates, such as the 10-year Treasury yield, work differently. They are determined by a much larger market, influenced by many factors outside the Fed’s control.

The 10-year Treasury yield reflects the annual return an investor can expect if they buy a 10-year U.S. Treasury bond today and hold it until maturity. This yield is considered the most important financial benchmark in the global fiat system, as it determines valuations and market trends worldwide. Think of it as the “heartbeat” of the dollar system.

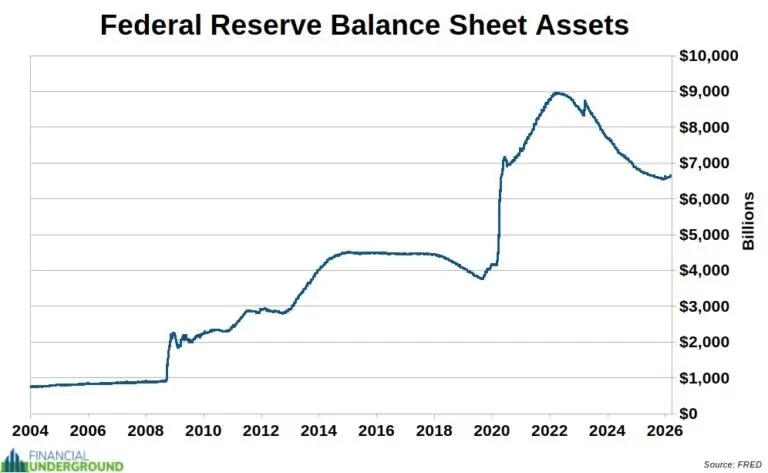

Indicator 5: Fed Balance Sheet

The Fed recently announced that it has stopped shrinking its balance sheet and will start expanding it again. The Fed says this is not quantitative easing, but “inventory management,” ignoring that it is not explicitly targeting long-term bonds. This is just a play on words.

The Fed’s bond buying with money created is money printing, no matter what the name. The Fed’s balance sheet is expanding again, starting a new printing cycle. The trend is obvious: every time the Fed expands its balance sheet, the currency depreciates. This is not a random or temporary policy error — it is a fundamental feature of the system.

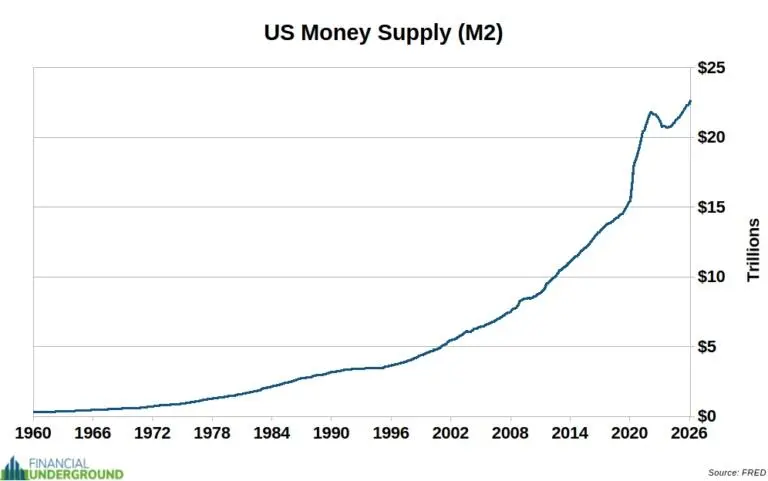

Indicator 6: Money Supply

Imagine working 9 to 5 for 50 years, only to have the Fed print 40% of the money supply and undo 20 years of hard work. No imagination required — it happened during the Covid hysteria, as governments around the world succumbed to a currency devaluation craze. The Fed has only two tools: currency devaluation and deception.

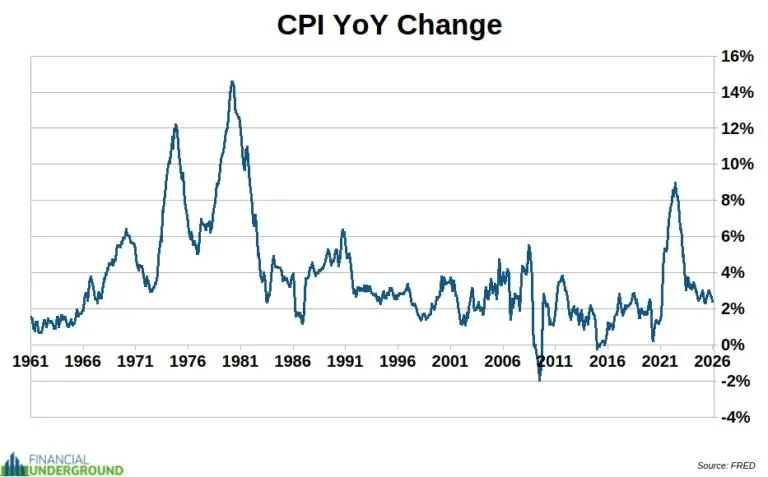

Index 7: Consumer Price Index (CPI)

The CPI is the most politically manipulated statistic in the entire government. And that’s saying a lot, because many statistics are manipulated, but the CPI is probably the most manipulated. The CPI attempts to measure average price changes for 340 million Americans, which is impossible because of the different baskets of goods purchased by each individual.

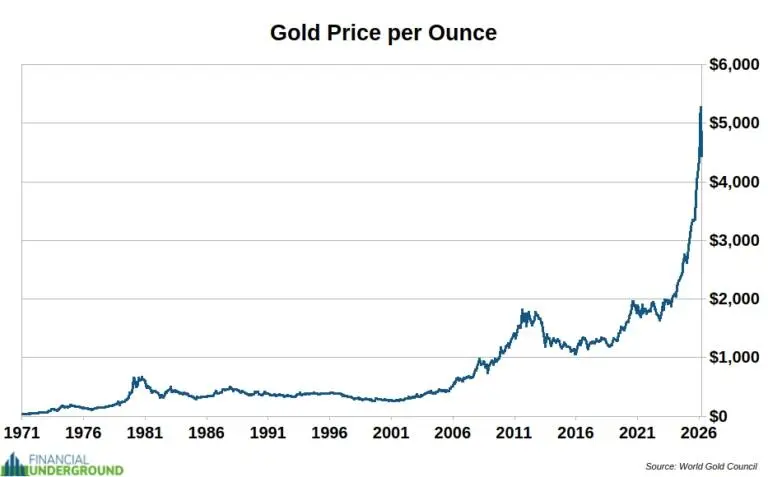

Indicator 8: Gold Price

Gold has been humanity’s most enduring currency for over 5,000 years, thanks to its unique characteristics: durable, consistent, convenient, rare, and the hardest of all natural commodities.

Gold is incorruptible, and its reserves have been accumulated for thousands of years. No one can arbitrarily increase its supply. This makes it an excellent store of value. All peoples value it.

Its value is not dependent on any government or rival party.

These eight indicators all point in the same direction: more debt, more money printing, and more erosion of the dollar’s purchasing power.