In a speech in July, Harvard University professor Gregory Mankiw laid out with brutal honesty what needs to happen to end the unsustainable accumulation of debt in the United States.

The options are five:

deep cuts in government spending,

extraordinarily high economic growth,

significant tax increases,

bankruptcy, or

large-scale money printing, i.e. inflation.

Logic dictates that some combination of these will be inevitable.

These potential solutions are common throughout the developed world. Through a process of exclusion, deep spending cuts are unlikely, given aging populations and the political power of the elderly. Also, economic growth alone is not going to solve the problem, and a fanciful “AI explosion” will likely raise interest rates rather than lower them. Moreover, the amount of highly skilled immigrants that would be needed to support future fiscal needs is completely unrealistic.

So that leaves three unpleasant options: tax hikes, bankruptcy, and inflation.

The most likely of these is inflation — a risk that looms over those currently investing in long-term bonds.

In some countries, tax increases are feasible. The United States has a relatively low tax burden by international standards, as it has no value-added tax (VAT) — a mild consumption tax. However, the current Republican Party is unlikely to support any major tax increases unless forced by a severe economic crisis.

Such a crisis is considered almost inevitable, something both parties in Washington acknowledge behind closed doors. The only question is when. Crises have a tendency to make the unthinkable possible.

Before the financial crisis of 2007-09, it seemed impossible for Congress to pass “checks” to save the financial system. But the chaos in the markets forced it to pass the Troubled Asset Relief Program (TARP), a plan to buy “toxic” assets.

Unfortunately, the nature of the next crisis is such that it can only be prevented at reasonable cost in advance. If public debt reaches 150% or 200% of GDP, the cost of servicing it will increase so rapidly in the event of a massive sale of bonds that the necessary tax increases will be politically impossible.

Europe is in a better political but a worse fiscal position. Politically, because tax increases are not considered as prohibitive as in the United States; but fiscally, because this acceptance has already left European countries with very high taxes. In France, for example, government revenue is 52% of GDP.

A well-known economic result is that the damage caused by a tax increases as the square of the tax rate. Therefore, if high-tax economies try to cover their budget deficits through further increases in capital taxation, they risk significantly slowing growth.

Japan is an intermediate case. Its taxes are lower than in Europe and its fiscal balances are less strained, but its public debt is higher, making it more vulnerable to economic shocks. Thus, the world is faced with a difficult choice: either accept inflation as an inevitable price, or be forced to face a crisis that will make the unthinkable inevitable.

Across the developed world, bondholders are increasingly likely to face Gregory Mankiw’s final two choices — bankruptcy or inflation — and neither will be painless.

First, there is the possibility of default. In the postwar era, there was a strong taboo in rich countries against restructuring or defaulting on their sovereign debt. The only exceptions were Greece and Cyprus in the 2010s.

However, in recent years, politicians have broken many taboos, and the political scene has become so divisive that nothing can be considered impossible. But in countries that issue debt in their own currency—and which, unlike Greece, which was a member of the eurozone, have the ability to print money to repay their debt—creditors have historically paid the price through inflation.

That is precisely what happened in the first decades after World War II, when inflation played a key role in reducing the huge debts that the war had created.

Economists point out that only unexpected inflation actually reduces debt burdens. When price increases are predicted, bond investors take this into account, demanding higher yields from the outset.

In the postwar period, however, various restrictions prevented bondholders from protecting themselves in this way.

In the United States, the Federal Reserve had imposed a cap on long-term bond yields from 1942 to 1951. For decades, Regulation Q had prohibited banks from paying interest on deposits, ensuring that there would be demand for government bonds with artificially low yields.

Banks were often forced to hold large amounts of government debt, while capital controls made it difficult for investors to sell and switch to other markets.

Debt and Inflation

Today, however, capital flows freely around the world, making it difficult to imagine a 1950s-style debt solution.

Nevertheless, governments still have the tools to deflate their debt through inflation. Central banks have become accustomed to buying bonds with freshly printed money — called reserves — that pay interest.

The more bonds a central bank buys, the more direct control it has over the cost of servicing the government’s debt. A combination of bond purchases and keeping interest rates below inflation would result in a reduction in debt in real terms.

Independent central bankers, who see themselves as custodians of price and financial stability — not as fixers of fiscal crises — would never willingly sign off on such a plan. But they are coming under increasing political pressure.

Donald Trump has repeatedly called on the Fed to keep short-term interest rates low. If long-term yields remain high, the next step could be to pressure the Fed to rein them in, as it did in the 1940s.

The European Central Bank (ECB), under treaty rules, is prohibited from financing governments. In practice, however, it is already indirectly backing the European Union’s sovereign debt. During the Covid-19 pandemic, it has refocused its bond purchases on Italy, while inventing new mechanisms to keep interest rates low.

If the time came to choose between an inflationary explosion or a major economy leaving the euro due to a debt crisis, Mario Draghi’s old motto—“whatever it takes”—would certainly trump the inflation target.

That is, the central bank would create money to buy bonds in order to save the common currency.

In Britain, Reform UK, a right-wing patriotic party with a commanding lead in the polls, is promising to finance its big spending by abolishing interest on bank reserves — a policy that would make it profitable to create new money, that is, to “print” new sterling.

Perhaps the strongest argument against inflation is that, like spending cuts or tax increases, it is deeply unpopular. But unlike fiscal decisions, inflation can occur both intentionally and unintentionally.

When politicians misunderstand or conceal the consequences of their actions, inflation becomes a measure of their contradictions — and by the time it appears, it is already too late to stop it.

The Middle Class in a Vice and What Causes Inflation

For the Federal Reserve (Fed), the main challenge is the rise in prices of basic goods and services: food, housing, clothing and transportation. What everyday life and official data show

The Consumer Price Index (CPI) shows a cumulative increase of about 20% over the past five years.

In everyday life, consumers are experiencing increases of 30% or more, especially in critical goods, and the trend continues in 2025.

Economist Thanos Chonthrogiannis notes that:

The CPI is a problematic indicator because it attempts to find an “average price” of goods and services — something impossible.

Inflation is caused by the government, through artificial expansion of the money supply to finance deficit spending, not by individual spending.

The Great Pandemic Experiment

During COVID, a $6 trillion fiscal injection into the existing $15 trillion money supply increased the amount of money per citizen from $50,000 in 2020 to $75,000 in 2022.

The 50% increase in liquidity means that price increases were mathematically inevitable.

The Fed’s Tools to Fight Inflation

Increase in the federal funds rate (FFR): From 0.0-0.25% in March 2020 to 5.00–5.25% in February 2023.

Quantitative Tightening (QT): Initially, $1 trillion in bonds and MBS (Mortgage-Backed Securities) were allowed to mature without replacement, reducing liquidity.

Initial limits: $60 billion/month for Treasuries, $35 billion/month for MBS.

June 2024: $25 billion/month for bonds.

April 2025: $5 billion/month for bonds, MBS unchanged.

The big question is: Do these tools work?

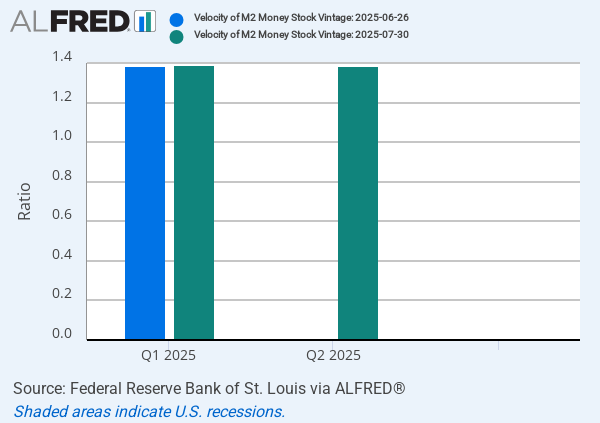

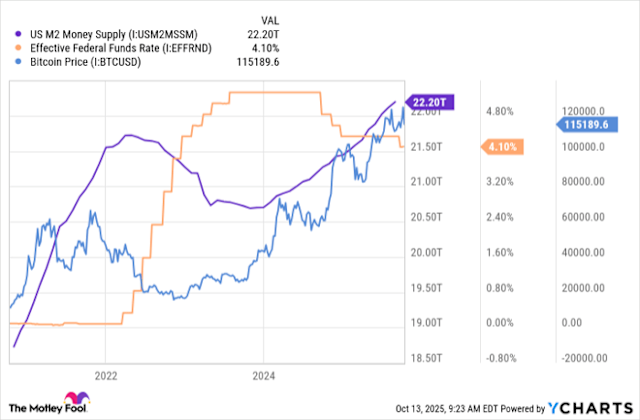

The state of money (M2) and inflation 2020–2025

The M2 liquidity measure, as tracked by the Federal Reserve Bank of St. Louis (FRED), includes:

Paper money and Fed coins in circulation,

All checking accounts at banks,

Savings deposits at banks, savings and credit unions,

Certificates of deposit (CDs) and mutual fund shares held by individuals.

Looking at the period from June 2020 to May 2025, three major stages are observed:

Massive money injection during the pandemic (2020–2022)

o The M2 line rises sharply (the “blue line”).

o The reason: $6 trillion new fiat dollars to support the economy and households.

o Consequence: strong consumer price inflation.

M2 Reduction via Quantitative Tightening (QT) 5/2022–10/2023

The Fed let $1 trillion in bonds and MBS expire without replacement, reducing liquidity.

Result: reduced inflationary pressure, but only temporarily.

Reversal and new all-time high after 10/2023 – 6/2025

M2 rose again to a new all-time high, exceeding $23 trillion.

Reason: continued printing of dollars to cover the federal deficit, which is estimated to exceed the budget by $1.9 trillion this year.

Why is inflation continuing?

The Fed recently cut the FFR by 0.25%, to stimulate an anemic economy.

The simultaneous easing of monetary policy and continued government spending means that the upward push in prices continues.

Who is most affected?

The government benefits: debts are paid off with “soft” dollars (inflated dollars).

The middle class bears the brunt, as price increases reduce its purchasing power.

The rich are minimally affected, because their incomes and assets are affected much less.

What would it take to reduce inflation?

Aggressive quantitative tightening and other methods of reducing the money supply.

Inevitably, such measures may cause a recession, but not a depression of the potential for economic output growth.

The goal: to bring interest rates, money supply, and inflation to reasonable levels without destroying the middle class

A taste of what’s to come

Nobody planned for the high inflation of the 1970s, which governments tried to deal with with irrational measures like price controls. The inflation explosion of the 2020s, which followed massive money creation and pandemic fiscal stimulus, was just a taste of what’s to come.

Without bold action by governments, more inflation is inevitable. And when it comes, it will prove politically toxic for rich democracies, and it will spell political change. Long-term bond investors will be in a difficult position — and they certainly won’t leave states unpunished.