Donald Trump is making a dramatic move that could change the face of global capital flows – access to the world’s largest market will not be free. To participate in the US financial system, which is the deepest and most liquid in the world, comes at a significant cost.

Following the swift passage of the Big, Beautiful Act by the US House of Representatives on May 22, a provision known as Section 899 has caught the attention of investors around the world, including a new set of “retaliatory” or punitive taxes on inbound foreign investment.

With the bill set to receive a public hearing in the Senate soon, there are growing concerns that some of the most sweeping changes to the tax treatment of foreign capital in the US in decades could lead to a sharp decline in foreign investment in US assets.

What is Article 899?

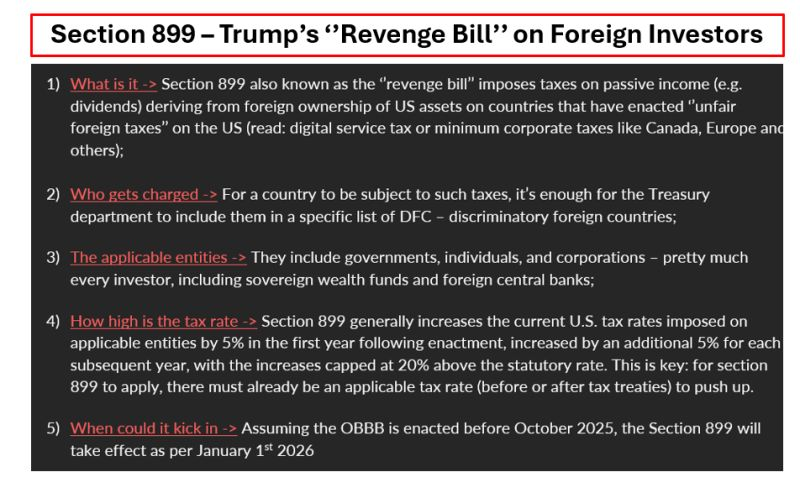

Titled “Enforcement of remedies against unfair foreign taxes,” Section 899 is a new provision that targets investments from countries that impose “discriminatory and extraterritorial taxes” on American businesses. The taxes named include digital services taxes, a tax on diverted profits, and undertaxed profits rules.

This provision is certainly a loaded weapon in Big Tech’s negotiations with Europe over their tax status in the single market. Governments, companies, private foundations, or individuals from these countries would be charged an additional 5 percent withholding tax rate each year on income generated in the United States, potentially increasing the rate to as much as 20 percent, until the “unfair taxation” is eliminated.

Echoing the spirit of the plan for a monetary “Mar-a-Lago Accord,” Section 899 reflects Washington’s growing readiness to leverage U.S. dominance in global capital markets to address what the Trump administration has cited as unfair treatment of American businesses abroad.

Which countries will be targeted?

The Section 899 measures could take effect as early as January 1 if the bill is passed by October 3. Several countries, including U.S. allies, already impose taxes that Washington has deemed “unfair” in a summary of the bill published by the House of Representatives Committee on Taxation.

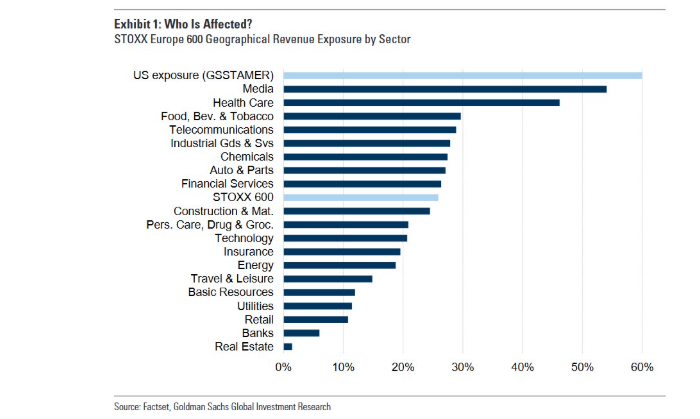

Taxes on Big Tech

For example, some European countries, including France, Italy and the UK, have imposed digital services taxes of around 2% to 5%.

These taxes target the digital services economy such as online advertising, online shopping and data monetisation, sectors dominated by US tech giants such as Google, Apple, Amazon, Meta and Microsoft.

Meanwhile, Australia and the UK have suspended their existing corporate profits taxes. And countries such as South Korea, Australia and Germany have implemented undertaxed profits rules.

The Undertaxed Profits Rule (UTPR) allows a country to raise taxes on a business if it is part of a larger company that pays less than the proposed global minimum tax of 15% in another jurisdiction.

This is part of the Global Tax Code of the Organization for Economic Cooperation and Development (OECD). However, the definition of an “unfair tax” remains unclear, as the bill gives the Minister of Finance broad discretion to determine what constitutes such a tax, leaving room for interpretation and possible expansion beyond current levels. So it remains to be seen which countries will ultimately be targeted.

Capital Control Dynamics

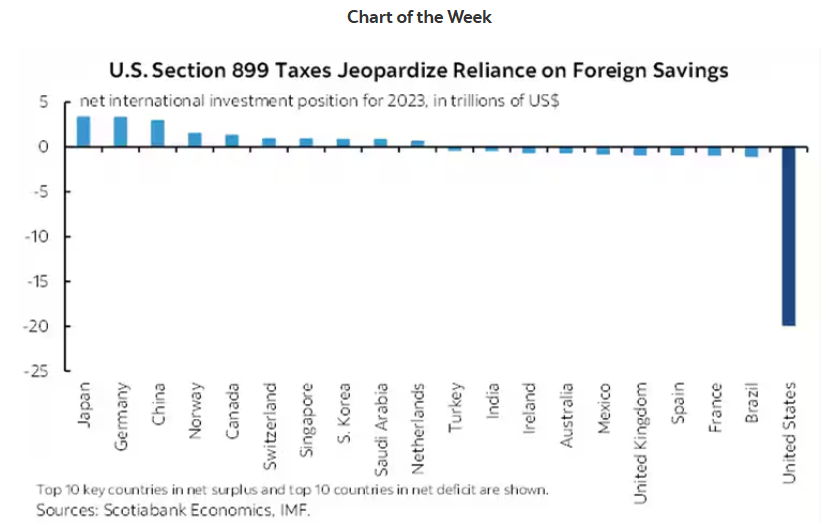

How will the provision affect U.S. assets? The provision reflects a capital control dynamic in the U.S. and could potentially cause a 5% drop in the U.S. dollar, as well as a roughly half-point increase in Treasury yields, and trigger a sell-off in the stock market.

If [Trump] goes ahead with his policy, we think that could create a big, scary moment, especially in the equity market and also, again, in the bond market. ING’s global head of markets, Chris Turner, also said on Monday (June 2) that the “retaliatory tax” would add to the narrative of a potential sell-off of U.S. assets.

If enacted, the provision could add to the long-term federal deficit, according to the independent Joint Committee on Taxation of Congress. Cross-border income flows associated with hedge funds, private equity, sovereign wealth funds and other large global investment vehicles would potentially be disrupted by Section 899 if enacted, with significant implications for the asset management industry.

It is being discounted as a bargaining chip

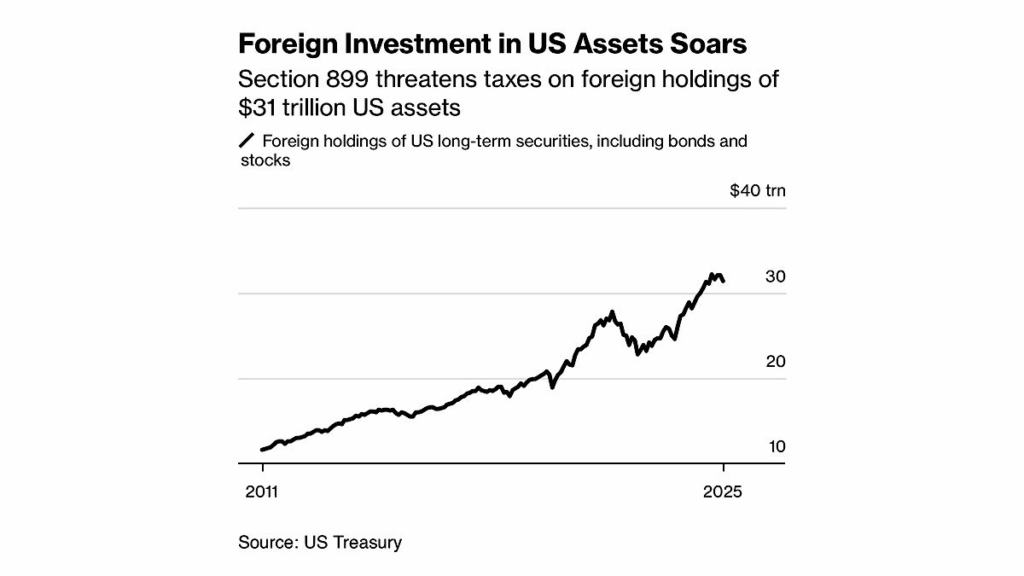

It should be noted that foreign investors hold a significant portion of the approximately $31 trillion in long-term US securities, including stocks and bonds.

I don’t think markets are discounting a full implementation of Section 899 today, so this could actually spook the markets quite a bit. The measure would be a form of “capital controls.” This is a significant reversal of the liberalization of capital flows that characterized the era of globalization—a milestone that was marked by China’s entry into the World Trade Organization in 2001.

The general view across Wall Street is that the provision would create yet another disincentive for foreign investors at a time when their once-unwavering confidence in Treasury bonds and other U.S. assets has already been shaken by Trump’s erratic trade policies and the country’s deteriorating fiscal accounts.

The risk of foreign capital outflows was reiterated by the independent Joint Committee on Taxation of Congress, which is tasked with producing official revenue projections for the legislation.

The provision would raise $116.3 billion over the next 10 years but would ultimately reduce annual U.S. tax revenue by $12.9 billion in 2033 and 2034.

Senate Republicans will consider its potential impact before approving the measure, Majority Leader John Thune said Monday, while a key Republican negotiator on tax cuts in the House of Representatives said he hoped it would be a deterrent that would never be used.

House Tax Committee spokesman JP Freire said the measure would not cover portfolios such as Treasury bonds, indicating uncertainty remains about its exact scope.

Further outflows would run counter to Trump’s policies to encourage long-term investment in the U.S., increasing the likelihood of a withdrawal, which may explain why markets have so far been reluctant to price in the risk, Subran said. The impact could “completely negate what he’s trying to do on his policy agenda,” he said.

The reshaping of globalization is happening before our eyes, with President Donald Trump’s economic policies playing a key role.