Record trading after the Iran crisis

In early April, just hours after US President Donald Trump’s televised speech in which he threatened Iran with devastating blows, the Chinese cross-border payment system CIPS (Cross-Border Interbank Payment System) recorded a historical trading record. On April 2, trading volume reached 1.22 trillion yuan (about $180 billion), almost double the daily average in February. This surge is directly linked to the increase in yuan-denominated energy transactions from oil-producing countries, in the context of the so-called “petroyuan”. The conflict in the Middle East and the uncertainty around the Strait of Hormuz accelerated a trend that had already been taking shape in recent years: more and more countries are looking for alternative payment systems and reserve currencies beyond the dollar.

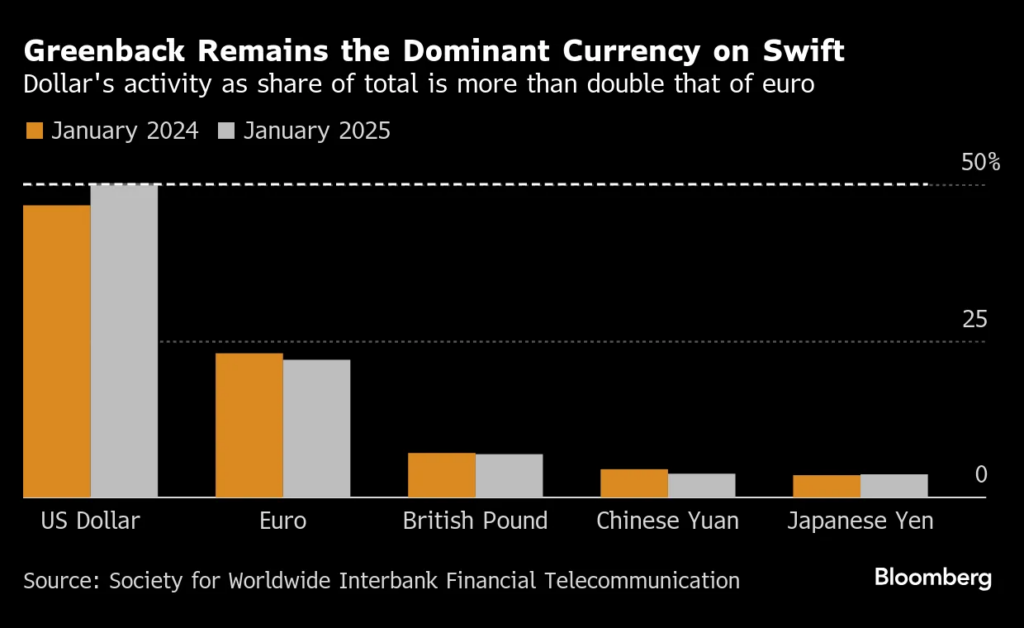

The dollar remains dominant

Despite the yuan’s momentum, the reality remains that the US currency still dominates. According to SWIFT data, the dollar is used in more than 45%-50% of global cross-border payments, while the euro follows with about 20%-22%. The yuan is still considerably lower, but the gap is steadily narrowing. China has already become the largest trading partner of more than 120 countries worldwide, which creates a natural demand for the use of the yuan in trade transactions. At the same time, the People’s Bank of China has concluded dozens of bilateral currency swap agreements with central banks around the world, facilitating the use of the yuan in international trade.

Europe’s Weakness

For the economic research and business advisory firm Trust Economics, the yuan’s rise depends not only on China’s strengthening but also on Europe’s relative decline. If Europe continues to move on a low-growth trajectory, the euro risks losing second place faster than many estimate. The European economy faces a series of structural challenges:- high energy costs after the break with Russia,

- weak industrial production,

- demographic aging,

- low productivity,

- limited growth compared to the United States and Asia.

The yuan as a trade currency

The real power of the Chinese currency is not yet in global reserves but in trade. The governor of the People’s Bank of China, Pan Gongsheng, stated as early as 2025 that the yuan had become the second most important currency for financing global trade and the third most important currency for international payments. In recent years:- Russia conducts a large part of its trade with China in yuan,

- Gulf countries are increasing energy transactions in Chinese currency,

- BRICS members are increasing the use of local currencies,

- many emerging economies are gradually reducing their dependence on the dollar.

The Energy Transition Advantage

China has another strategic advantage. It controls much of the global value chain in clean energy technologies:- about 80% of global solar panel production,

- about 80% of battery production,

- about 75% of electric vehicle production.

A Wonderful Multicurrency World

The real question is not whether the yuan will “beat” the euro or the dollar. The more likely scenario is a transition to a multicurrency system, in which different currencies dominate different geographies and sectors of the economy. The dollar may remain the world’s main reserve currency for decades to come. However, the yuan seems to be gaining an increasingly important role in energy trade, Asian trade, the BRICS countries, and the so-called Global South. If Europe’s economic stagnation continues and China maintains its position as the world’s largest trading power, the yuan’s overtaking of the euro could be the next big milestone in the reshaping of the global monetary system. The real challenge for Beijing, however, is not just to increase the use of the yuan in transactions. It is to create a financial system deep, reliable, and open enough that investors will trust it as an alternative to the dollar. That will ultimately determine whether the era of dedollarization will indeed lead to a new global monetary order.Please follow and like us: