The Bureau of Labor Statistics (BLS) argued that a pick-up in rent inflation—the index rose unexpectedly sharply in January’s CPI—was due to a shift in the data series that could either mean that the change was a structural shift in values or indeed an error which could be fixed at a later stage.

Conclusion; No victory over inflation has been achieved, just a momentary retreat – and of course the politically calculated effort to obscure the significance of data that does not support the current “narrative” of the Federal Reserve and the Biden administration. So, we would have to say the most consistent narrative that fits the latest series of data is that while there is still some progress on the path to deflation, uncertainty is the dominant element.

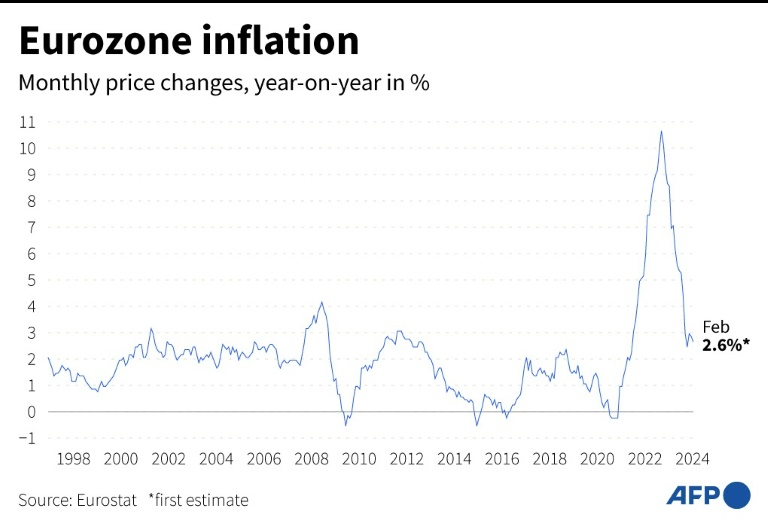

What is happening in the Eurozone?

European inflation data for February more or less underlined this element of uncertainty. The current trend of gradual deflation, according to recent data from Spain, Belgium, Germany and France, remains, but the new data does not ease concerns that core inflation is not on a downward path.

The negative impact of an early move by central banks still outweighs the cost of a somewhat delayed rate cut: credibility would take another hit if a resurgence of inflationary pressures led to a rapid reversal of monetary policy easing – and so we would hardly expect a rate cut within the year that would indicate a direct reversal of monetary policy.

Bowing central banks to the election cycle and prematurely cutting interest rates while keeping inflation high and a recession—not a far-fetched development—would cause not just protests but a social explosion. The European Parliament, which holds the ECB responsible for credit conditions in the Eurozone, expressed its dismay this week at high inflation and the credibility of monetary institutions.

The central European plan of the ECB

However, the ECB began to cultivate its narrative. The ECB intends to adopt a “floor” (on the interest rate) based on (the banking system’s) demand for funding. In such a policy framework, the central bank provides as much liquidity as banks demand, while using the lending rate to steer money markets by setting the lowest rate at which banks are willing to lend to each other in the interbank market.

The effectiveness of such a policy is based on the banks’ willingness to borrow from the ECB. This is related to the cost of borrowing the central bank’s reserves. Thus, the ECB can improve efficiency by narrowing the spread between the refinancing rate and the deposit rate.

Could the ECB announce an asynchronous refinancing rate cut next Thursday, March 7? Given the ample liquidity in the system, this should not materially affect money market rates. However, it would pose a huge communication challenge, particularly to a wider audience that does not distinguish between different policy rates.

Consumer spending and manufacturing

China’s manufacturing data released on Friday, March 2, 2024, indicated that manufacturing activity contracted again in February (the official PMI fell 0.1 points to 49.1 in February), but services activity rose somewhat (up 0, 7 in 51.4).

- Are government interventions in stock markets helping to create a rebound in consumer sentiment and spending? Amazing.

- The recovery in services was likely due to particularly high holiday spending rather than a sign of a broad recovery in the economy.

- If manufacturing remains weak while services activity picks up, the biggest risk is perhaps that the policy response will be one to stimulate production (and spare capacity) rather than consumption.